Why is the Indian Rupee Falling? Causes & Economic Impact (2026)

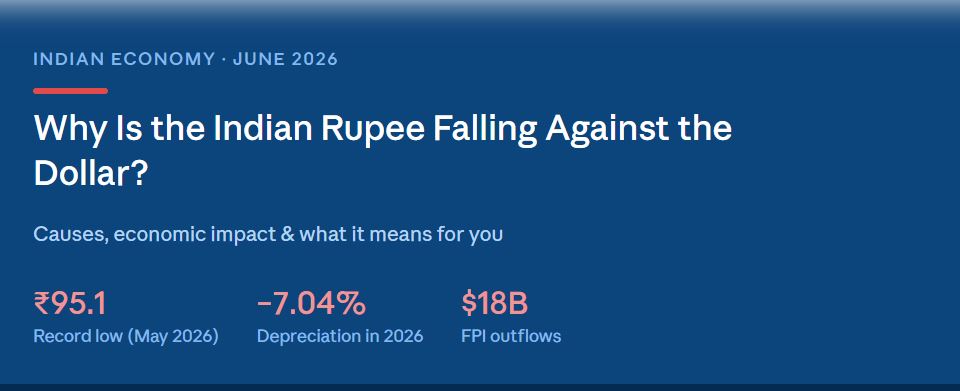

From ₹85.53 in early 2025 to over ₹95 in May 2026, the Indian rupee has shed more than 10% of its value against the US dollar in little over a year — one of the steepest slides since 2013. This isn’t just a number on a forex ticker. It’s showing up in your fuel bill, your grocery basket, your overseas tuition fees, and your investment portfolio.

This guide breaks down exactly why the rupee is falling, what it means for India’s economy, and who gains and loses in this environment.

What does rupee depreciation mean?

Currency depreciation occurs when a currency’s value declines relative to another currency in the open market. When the rupee depreciates against the dollar, it simply means you need more rupees to buy one US dollar. Two years ago, $1 cost ₹83. Today it costs ₹95.

Like stock prices, the rupee’s value is driven by demand and supply. If demand for the dollar rises — through higher imports, capital outflows, or global risk aversion — the rupee weakens. If foreign investment pours in or exports boom, the rupee strengthens.

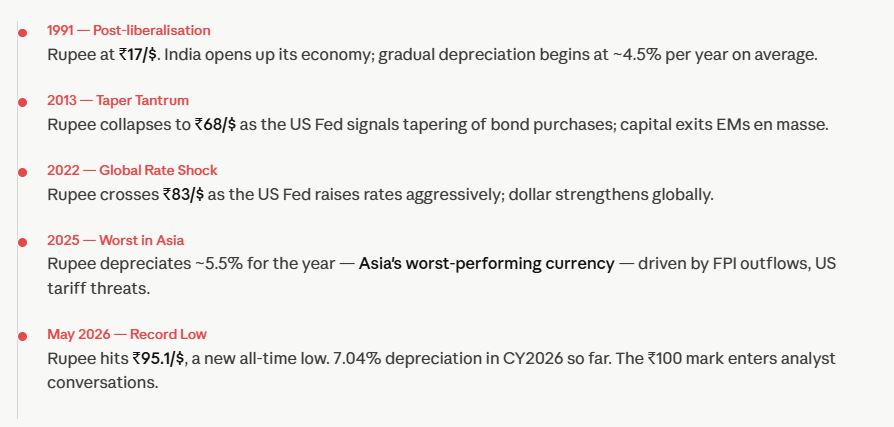

Historical context: ₹17 to ₹95 in 35 years

“India’s current account deficit faces more severe pressure than those of Indonesia and the Philippines. US tariffs damage Indian exports, while a weaker rupee amplifies a higher war-related oil import bill and discourages investor equity inflows.”— UBS Report, as cited in The Hindu (2026)

Key causes of the 2025–2026 depreciation

1. Soaring crude oil imports

India imports ~70% of its crude oil in USD. With Brent crude trading near $111–121 per barrel amid the West Asia conflict, India is buying dollars relentlessly to pay for oil. Analysts estimate this alone creates a $40–50 billion dollar inflow shortfall this fiscal year — the single largest structural cause of the current slide.

2. Massive FPI (foreign portfolio investor) outflows

Foreign portfolio investors have pulled over $17–18 billion from Indian equities in 2026, chasing better returns in Asian and European markets. Every FPI exit converts rupees into dollars before leaving India — directly increasing dollar demand and weakening the rupee.

3. US tariff shock on Indian exports

The Trump administration imposed tariffs of 26%–50% on Indian goods including gems, jewellery, electronics, and auto parts. This curtailed the dollar inflows that normally support the rupee. The depreciation accelerated sharply after the April 2025 tariff announcement and has not fully recovered since.

4. Widening current account deficit (CAD)

India’s imports are significantly exceeding its exports. The current account deficit for this fiscal year is estimated at $40–50 billion — wider than recent years. During Oct–Dec 2025, the CAD widened from $11.3 billion to $13.2 billion (1.3% of GDP). A structurally wide CAD is one of the most reliable predictors of sustained rupee weakness.

5. Narrowing US–India interest rate differential

The RBI cut its repo rate to 5.25% in December 2025 to stimulate growth, narrowing the interest rate advantage that had been attracting global capital to India. A reduced yield differential lowers foreign dollar inflows and adds sustained background pressure on the rupee.

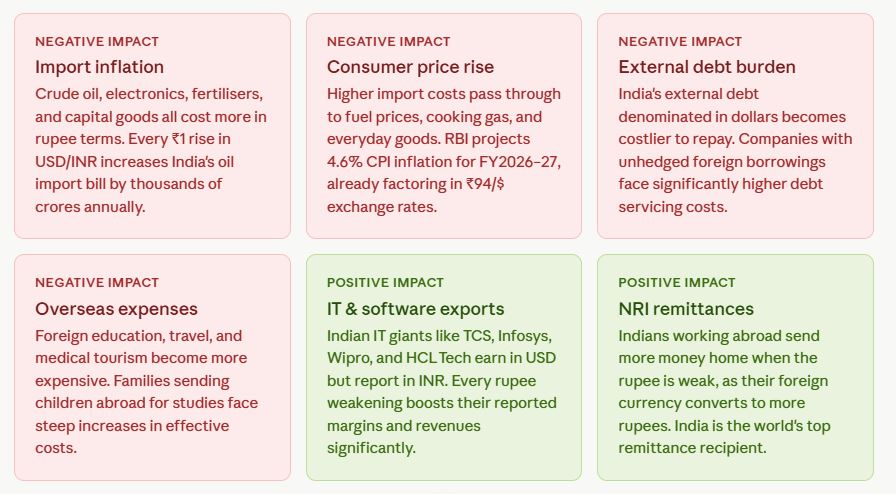

Impact on the Indian economy

The effects of a depreciating rupee ripple across every sector of the economy. Here’s both the downside and — surprisingly — the upside:

Sector-wise winners and losers

What analysts are forecasting

Despite crossing ₹95, most mainstream financial institutions do not project the rupee hitting ₹100 in 2026. A recovery hinges largely on a US–India trade deal and a stabilisation of crude oil prices.

The path to ₹100 is described as a “bearish multi-year scenario for 2028–2030” that would require oil above $130 per barrel and major tariff escalation simultaneously — not a base-case forecast for 2026.

What the RBI is doing

The Reserve Bank of India has been actively managing the rupee’s fall rather than defending a fixed level. The RBI intervenes by selling dollars from its foreign exchange reserves to prevent disorderly or excessive depreciation, while also buying dollars when flows ease to rebuild reserves. India’s forex reserves have remained broadly in the $640–700 billion band since mid-2024, providing a credible buffer.

The RBI’s stance is to temper volatility, not freeze the exchange rate — allowing a gradual depreciation while preventing sharp daily swings that would rattle business confidence and foreign investment.