Term Insurance vs ULIP: Why Mixing Insurance With Investment Costs You Lakhs

Let me tell you about Ramesh.

He’s 32, married, has a 2-year-old, and earns ₹12 lakh a year. His LIC agent — a family friend of 15 years — sat across the dinner table and said: “Bhai, ek hi policy mein insurance bhi, investment bhi. ₹25,000 premium. Best deal hai.”

Ramesh signed up. Because it felt responsible. It felt like he was doing two things with one rupee.

He wasn’t.

He was slowly, politely, bleeding ₹30–40 lakhs of potential wealth over 20 years — and he had no idea.

This is the story of millions of Indians. And this blog is going to break that cycle for you.

What Is a ULIP? (And Why It Sounds Better Than It Is)

ULIP stands for Unit Linked Insurance Plan. It’s a hybrid financial product that bundles life insurance coverage with market-linked investment — all in one premium.

Your premium is split into:

- A portion for life cover

- A portion for fund investment (equity, debt, or hybrid)

- A (surprisingly large) portion for charges

On paper, it sounds like the best of both worlds. In reality, it’s a compromise that delivers neither well.

ULIP was the darling of insurance agents in the early 2000s. After IRDAI regulations in 2010, many of the worst practices were cleaned up — but the fundamental design flaw remains.

What Is Term Insurance? (Pure, Simple, Powerful)

Term Insurance is the most straightforward life insurance product available.

You pay a fixed annual premium. If you die within the policy term, your family gets a large lump-sum payout (the Sum Assured). If you survive the term, you get nothing back.

That last part makes most Indians uncomfortable. It shouldn’t.

The “nothing back” is the whole point.

Because that’s what keeps premiums devastatingly affordable — and frees up your remaining money to actually grow through proper investments.

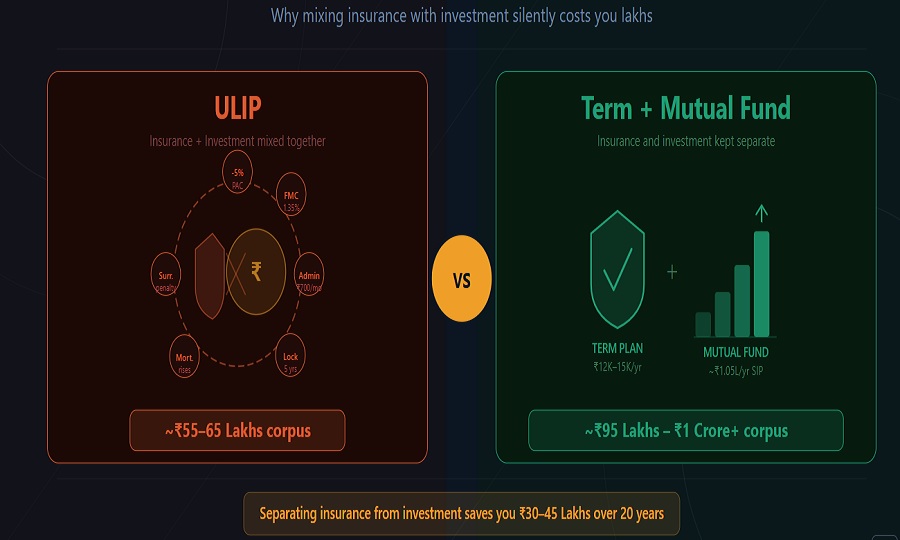

Term Insurance vs ULIP: The Real Numbers India Doesn’t Talk About

Let’s do the math that your insurance agent never showed you.

The Setup

| Parameter | Details |

|---|---|

| Age | 30 years |

| Sum Assured | ₹1 Crore |

| Investment Horizon | 20 Years |

| Annual Budget | ₹1,20,000 |

Option A: ULIP — ₹1,20,000/year premium for ₹1 Crore cover

Approximate charges deducted (Year 1–5):

- Premium Allocation Charge: 3–5%

- Policy Administration Charge: ₹500–₹700/month (₹6,000–₹8,400/year)

- Fund Management Charge: 1.35% per annum

- Mortality Charge: Increases every year with age

In the first year alone, you might lose 15–25% of your premium to charges before a single rupee gets invested.

Assuming 12% gross returns:

- Effective returns after all charges: ~8–9%

- Corpus after 20 years: Approx ₹55–65 lakhs

Option B: Term + Mutual Fund (The Smarter Alternative)

| Component | Amount |

|---|---|

| Term Insurance Premium (₹1 Cr cover) | ₹12,000–₹15,000/year |

| Remaining for Investment | ₹1,05,000–₹1,08,000/year |

Invested in a diversified equity mutual fund (index fund or large-cap) via SIP:

- Assumed returns: 12% CAGR (same assumption as ULIP)

- Corpus after 20 years: ₹95–1.05 Crore

Difference: ₹30 to ₹45 LAKHS more wealth — just by separating insurance from investment.

This isn’t magic. This is math. And this is why every serious financial advisor in India recommends separating your insurance from your investments.

The Hidden ULIP Charges Nobody Explains at Signing

Here’s the fine print that agents gloss over during that dinner table pitch:

1. Premium Allocation Charge (PAC)

Deducted before your money is invested. Can be as high as 5–8% in Year 1. So ₹1,20,000 premium means only ₹1,11,600–₹1,14,000 gets to work for you from Day 1.

2. Policy Administration Charge

A flat monthly fee just for having the policy. Sounds small. Compounds painfully over 20 years.

3. Fund Management Charge (FMC)

Charged as a % of your fund value. IRDAI caps it at 1.35%. Compare this to an index mutual fund’s expense ratio of 0.1–0.3%. That’s a 10x difference in annual drag.

4. Mortality Charge

This is the actual cost of your life cover. The problem? It’s deducted from your investment fund and increases every year as you age. By age 50+, this can become a significant drain on your corpus.

5. Surrender Charges

Try exiting a ULIP in the first 5 years and you’re penalized heavily. Your money is locked up — exactly when a market downturn might tempt you to exit badly.

6. Switching Charges

ULIP allows fund switches (equity to debt, etc.). Beyond free limits, each switch costs money.

Why Indian Families Fall for ULIPs (It’s Not Stupidity — It’s Psychology)

Let’s be honest. Smart, educated people buy ULIPs every day. Here’s why:

1. “Kuch toh milega” mentality Indians are culturally averse to “wasting” premiums. If a term plan pays nothing on survival, it feels like a loss — even if it isn’t. ULIPs exploit this emotional bias brilliantly.

2. The one-stop-shop illusion Managing one policy feels simpler than managing two products. The convenience is real. The financial cost of that convenience is also real — and enormous.

3. Social proof via agents Insurance agents earn significantly higher commissions on ULIPs than on term plans. A ₹1,20,000 ULIP premium earns an agent far more than a ₹15,000 term premium. The incentive structure is misaligned with your financial interest.

4. Tax saving confusion Both products qualify under Section 80C. But so do ELSS mutual funds — which give you far better returns with a shorter lock-in period (3 years vs 5 years for ULIP).

Term Insurance vs ULIP: Full Comparison at a Glance

| Parameter | Term Insurance | ULIP |

|---|---|---|

| Purpose | Pure life cover | Insurance + Investment |

| Premium | Very low (₹10K–₹20K/yr for ₹1Cr cover) | High (₹50K–₹2L/yr) |

| Death Benefit | Guaranteed Sum Assured | Higher of Fund Value or Sum Assured |

| Maturity Benefit | None | Fund value (variable) |

| Charges | Minimal | High (multiple charge heads) |

| Investment Returns | N/A | Market-linked (not guaranteed) |

| Flexibility | Simple | Complex |

| Lock-in | None (can stop anytime) | 5 years mandatory |

| Transparency | High | Low (hidden charges) |

| Tax Benefit | 80C + 10(10D) | 80C + 10(10D) |

| Best For | Everyone who needs life cover | Rarely the best choice |

When (If Ever) Does a ULIP Make Sense?

To be fair: there are rare scenarios where ULIPs might be considered:

- HNIs wanting a single tax-efficient wrapper for insurance + investment with estate planning benefits

- People who are extremely undisciplined investors and will not invest separately even with the best intentions

- Post-2020 ULIPs from newer insurers with very low charges (< 1% total annual charge) can be mildly competitive

But for the average Indian earning ₹5–30 lakh per year? The term + mutual fund combination wins. Every time.

The Right Way to Think About Life Insurance

Life insurance has one job: financially protect your family if you die too soon.

That’s it. It’s not a savings tool. It’s not an investment vehicle. It’s not a tax-saving instrument (though it helps there too). It’s financial protection for the people you love.

Once you accept this, the choice becomes obvious:

Buy the cheapest possible product that gives you the maximum cover.

That product is a pure term plan.

Then take the money you save on premiums and invest it separately — in index funds, PPF, NPS, or wherever fits your risk profile.

This is called the “Buy Term, Invest the Rest” strategy. It’s been the gold standard of financial planning globally for decades. It’s catching on in India, but not fast enough.

How to Choose the Right Term Plan in India

Not all term plans are equal. Here’s what to look for:

1. Claim Settlement Ratio (CSR)

Look for insurers with CSR above 98%. Check IRDAI’s annual report for updated figures. Names like LIC, HDFC Life, ICICI Prudential Life, and Max Life consistently rank high.

2. Solvency Ratio

Ensure the insurer has a solvency ratio above the IRDAI-mandated 1.5. Higher is safer.

3. Sum Assured

Rule of thumb: 15–20x your annual income. If you earn ₹10 lakh/year, aim for ₹1.5–2 Crore coverage.

4. Policy Term

Cover yourself until at least age 60–65 — when your assets and EPF/PPF can support your family independently.

5. Riders (Add-ons)

Consider:

- Critical Illness Rider — lump sum on diagnosis of major illness

- Accidental Death Benefit Rider — extra cover for accidental deaths

- Waiver of Premium Rider — premiums waived if you become disabled

6. Online vs Offline

Online term plans are 30–40% cheaper than offline ones because there’s no agent commission. If you’re reading this blog, you can absolutely buy online.

The ₹1 Crore Cover Reality Check

Many Indians think ₹1 Crore is a lot of money. In 2025, it isn’t.

- ₹1 Crore invested at 6% (conservative) generates ₹6 lakh/year

- Average Indian household expense: ₹8–12 lakh/year in Tier 1 cities

- Inflation will erode purchasing power further

For a family in Mumbai or Bengaluru, ₹1 Crore barely covers 8–10 years of expenses at current prices.

Reassess your cover. And get term insurance while you’re young — premiums only go up with age.

Action Plan: What to Do Right Now

If you have an existing ULIP:

- Check your current fund value and charges paid so far

- If past the 5-year lock-in — evaluate if surrender makes sense (factor in tax implications)

- If within lock-in — stop paying further premiums and activate the “paid-up” option if available

- Buy a term plan immediately — don’t leave your family unprotected while you restructure

If you’re starting fresh:

- Buy a term plan first — get covered before you do anything else

- Start an SIP in an index fund or diversified equity fund with the premium difference

- Set up a separate tax-saving investment (ELSS, PPF, NPS) for 80C benefits

- Review coverage every 5 years as your income and liabilities grow

Frequently Asked Questions

Q: Is ULIP better than term plan for tax saving? Both qualify for Section 80C deduction up to ₹1.5 lakh. Maturity proceeds are tax-free under 10(10D) if annual premium is ≤ ₹2.5 lakh (for ULIPs issued after Feb 2021). However, ELSS mutual funds also offer 80C benefits with better returns and only a 3-year lock-in — making them a stronger tax-saving option than ULIPs.

Q: Can I get money back with term insurance? Yes — some insurers offer “Return of Premium” (ROP) term plans where premiums are refunded if you survive the term. However, ROP plans cost significantly more (2–3x regular term premium) and the “refund” isn’t actually inflation-adjusted. Regular term + SIP almost always beats ROP term mathematically.

Q: My agent says ULIP gives guaranteed returns. Is that true? No. ULIP returns are market-linked and NOT guaranteed. Any agent claiming guaranteed returns on a ULIP is either mistaken or misleading you — report such mis-selling to IRDAI.

Q: What if I already have a ULIP and don’t know what to do? Don’t panic. If you’re within the 5-year lock-in, make the premium paid-up. After 5 years, evaluate surrender with a SEBI-registered financial advisor. Meanwhile, immediately buy a separate term plan to ensure your family is covered.

Q: Is LIC ULIP better than private ULIP? LIC ULIPs benefit from the trust and sovereign backing of LIC. However, the fundamental structure — high charges, mixed product, low flexibility — applies across all ULIPs. The term + investment separation strategy beats any ULIP, including LIC’s.

Final Verdict: Stop Mixing. Start Separating.

The financial services industry profits when you conflate insurance with investment. You profit when you separate them.

Insurance = Term Plan (cheap, simple, maximum cover) Investment = Mutual Funds / NPS / PPF (transparent, low-cost, market-linked)

This isn’t radical. This isn’t complicated. It’s just honest math that agents with commission incentives won’t do for you.

Ramesh, from our story at the top? He eventually found a fee-only financial advisor, surrendered his ULIP in year 6, bought a ₹1.5 Crore term plan for ₹18,000/year, and started a ₹10,000/month SIP.

Today, 8 years later, his mutual fund corpus has already crossed ₹18 lakh — with 12 more years of compounding to go.

The difference between a good financial decision and a bad one isn’t intelligence. It’s information.

Now you have it. Use it.