What Is Inflation in India and How Does It Destroy Your Savings ? (2026 Complete Guide)

Imagine you diligently put ₹1,00,000 in a savings account today. Your bank pays you 3% per year. In one year, you have ₹1,03,000 — and you feel good about your financial discipline.

But here’s what the bank didn’t tell you: the basket of goods you were planning to buy with that money now costs ₹1,04,500 — because inflation averaged 4.5% this year. In real terms, you are poorer than when you started.

This silent erosion is the story of inflation — and it is happening to millions of Indian families right now. In this comprehensive 2026 guide, we break down exactly what inflation is, how it is measured, how it is quietly destroying your savings, and — most importantly — what you can do to protect yourself.

⚠️ Why This Matters to You

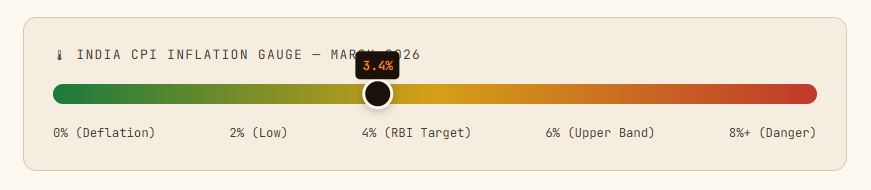

India’s CPI inflation rose to 3.4% in March 2026 and the FY 2025–26 annual average is estimated at 4.5%. If your money is sitting in a regular savings account earning 2.5–3%, you are losing purchasing power every single month.

1. What Is Inflation? A Plain-English Definition

Inflation is the rate at which the general level of prices for goods and services rises over time — and consequently, the purchasing power of money falls.

Think of it this way: if a plate of dal-chawal at your local dhaba cost ₹60 in 2020 and costs ₹85 today, that is inflation at work. The same meal. More money. Your ₹60 is worth less than it used to be.

At its core, inflation means your rupee buys fewer goods tomorrow than it does today. It’s not just about rising prices — it’s about the declining value of money itself.

“Inflation is taxation without legislation — it erodes the savings of the poor and the middle class while those with assets are shielded.”— Milton Friedman, Nobel Laureate in Economics

Inflation vs. Deflation vs. Stagflation

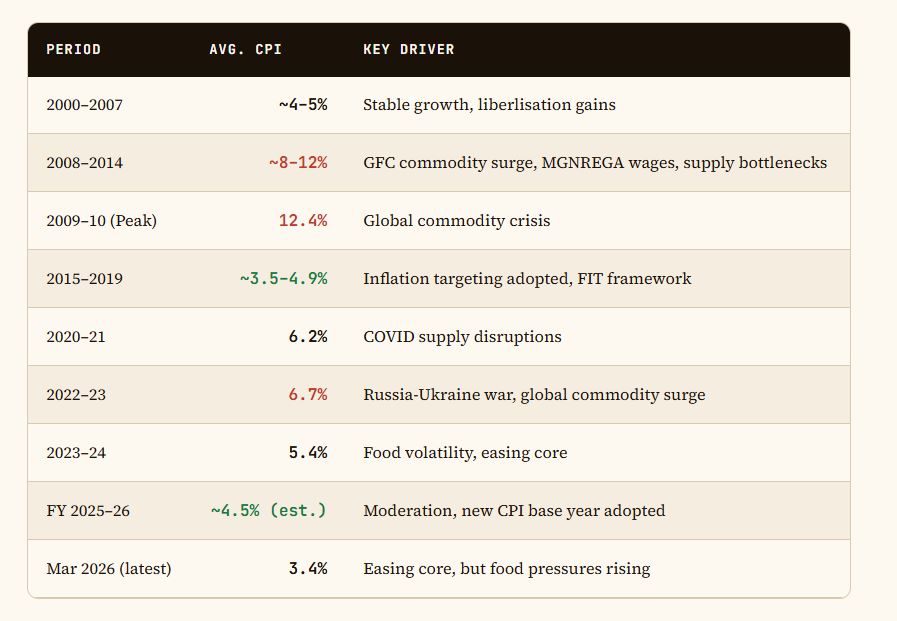

While inflation means prices are rising, deflation means prices are falling — which sounds good but is actually dangerous (people stop spending, economies contract). Stagflation — the worst of both worlds — means high inflation combined with stagnant economic growth and high unemployment. India experienced severe stagflation pressures during 2008–2014, when CPI inflation exceeded 8% for years.

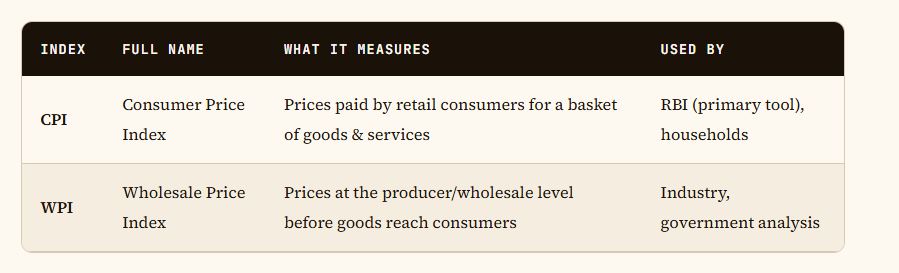

2. How Is Inflation Measured in India?

India uses two primary indices to measure inflation:

Since 2014, the RBI uses CPI as its primary inflation benchmark, because it better reflects the actual cost of living for Indian households. The CPI is computed monthly by the National Statistical Office (NSO) under the Ministry of Statistics & Programme Implementation (MOSPI).

What’s in the CPI Basket? (2026 Updated Weights)

3. India’s Inflation Situation in 2026

India’s retail inflation, as measured by CPI, rose to 3.4% in March 2026 from 3.21% in February — marking the highest reading in over a year. Despite this uptick, the rate remains below the RBI’s medium-term target of 4%, offering some relief.

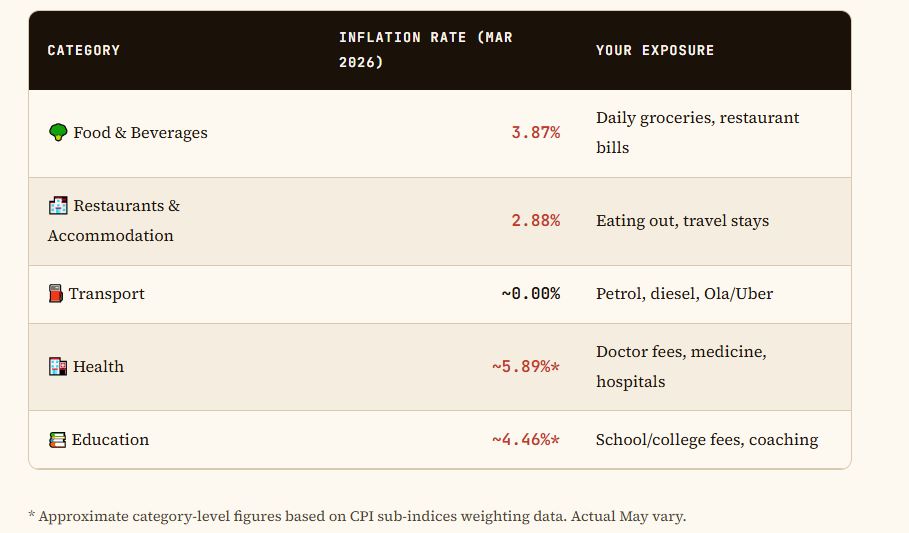

Food inflation reached 3.87% in March, driven by higher prices of vegetables, edible oils, and processed foods. Fuel and energy costs also contributed, driven by global energy price volatility and geopolitical tensions in West Asia disrupting supply chains.

✅ A Milestone Decision

In April 2026, India reaffirmed its flexible inflation targeting (FIT) framework, setting a 4% retail inflation goal with a tolerance band of 2–6% for the five years from April 2026 to March 2031 — signalling monetary policy stability and predictability for investors and businesses.

4. Types of Inflation You Must Know

Not all inflation is alike. Understanding the type helps you anticipate which sectors of your life will be hit hardest:

🔥 Demand-Pull Inflation

This happens when demand for goods exceeds supply. India saw this during post-COVID recovery when pent-up demand surged but supply chains hadn’t recovered. Result: prices skyrocketed.

💰 Cost-Push Inflation

When the cost of production rises (fuel, raw materials, labour), businesses pass those costs to consumers. Russia-Ukraine war-triggered fuel spikes in 2022–23 are a textbook example — India’s fuel inflation drove CPI to 6.7% in FY 2022–23.

🌱 Built-In Inflation (Wage-Price Spiral)

Workers demand higher wages to compensate for rising prices → businesses raise prices to cover wages → repeat. MGNREGA-driven rural wage growth in 2010–2014 contributed to this spiral in India.

🌾 Food & Fuel Inflation (India’s Special Problem)

India is uniquely exposed to food inflation due to monsoon dependency, poor rural infrastructure, and a large agricultural sector. A single bad monsoon in one state can push vegetable prices up nationally — making India’s inflation more volatile than that of most large economies.

5. How Inflation Destroys Your Savings — With Real ₹ Numbers

This is the most important section of this article. Abstract percentages don’t feel real — rupee calculations do.

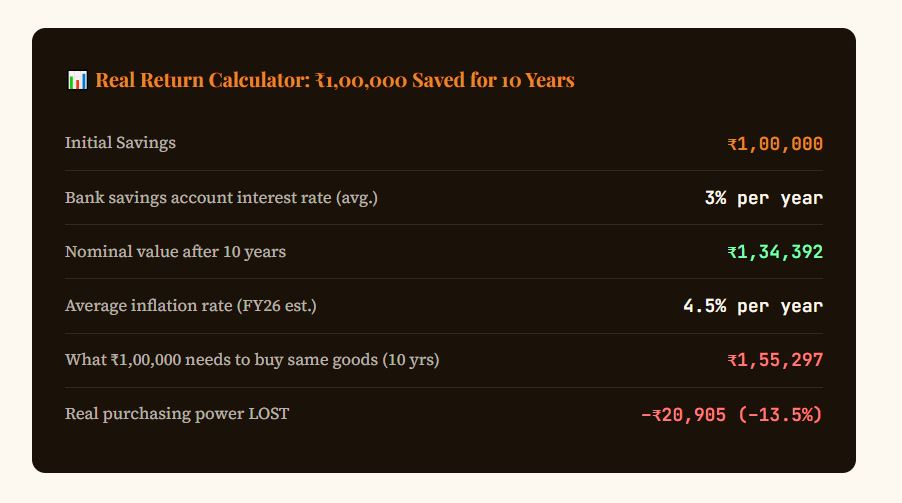

The Savings Account Trap

Despite earning ₹34,392 in interest over 10 years, you actually lost ₹20,905 in real purchasing power. You thought you were saving — but inflation was quietly stealing from you every day.

The “Real Interest Rate” Concept

Economists use a simple formula to reveal the truth about your savings:

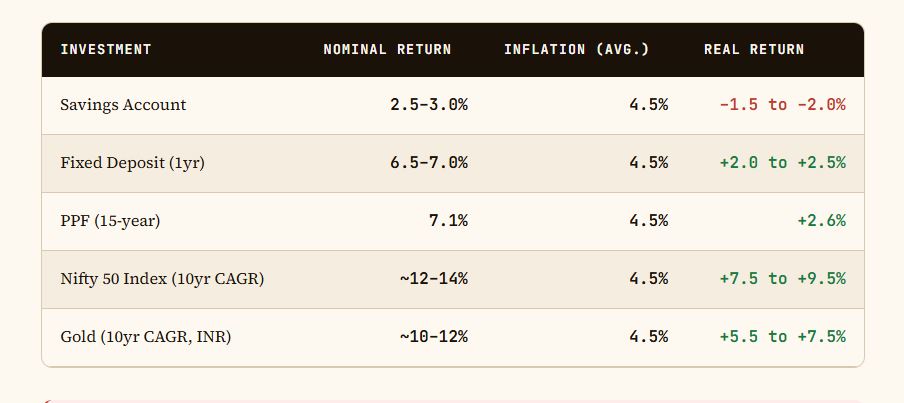

Real Return = Nominal Interest Rate − Inflation Rate

If your Fixed Deposit earns 6.5% and inflation is 4.5%, your real return is only +2%. If inflation climbs to 7%, your real return becomes –0.5% — you are losing money in real terms even while “earning interest.”

6. Which Categories Are Hitting Your Wallet Hardest?

Inflation doesn’t hit all categories equally. In 2026, some sectors are running far hotter than the headline number suggests:

Notice that health and education — two of the most important spending categories for Indian families — consistently run above the headline CPI. The real inflation experienced by a middle-class Indian family with children in school and elderly parents to care for is significantly higher than the 3.4% headline number.

7. India’s Inflation History: A 25-Year Journey

The adoption of the Flexible Inflation Targeting (FIT) framework in 2016 was a turning point. Average CPI since FIT: approximately 4.8%, versus 8.5% in the preceding five years. The framework — renewed for another five-year cycle in April 2026 — has brought measurable discipline to India’s monetary policy.

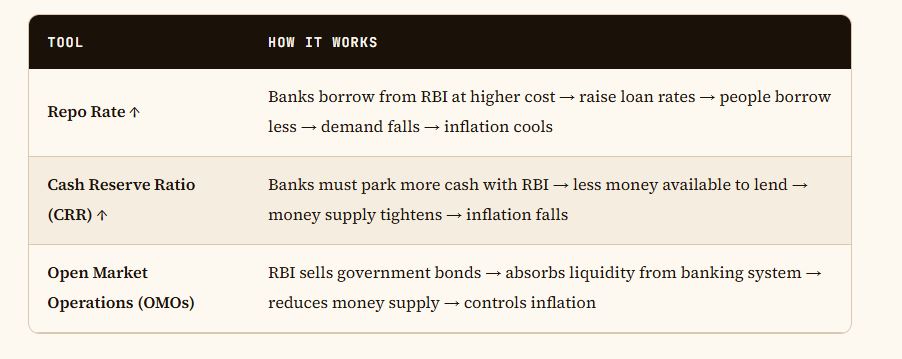

8. The RBI’s Role: What Is It Doing About Inflation?

The Reserve Bank of India is the primary institution responsible for managing inflation through monetary policy. Its six-member Monetary Policy Committee (MPC) meets six times a year to set the repo rate — the rate at which banks borrow from the RBI.

Key RBI Tools to Control Inflation

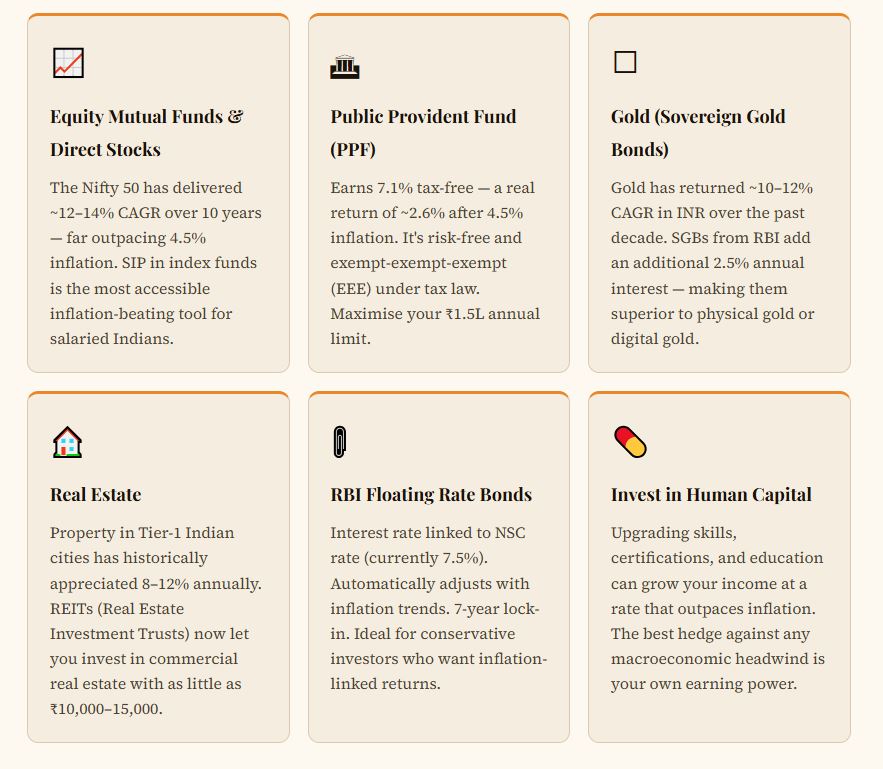

9. How to Protect Your Savings From Inflation (2026 Strategies)

The good news: inflation is manageable if you take deliberate action. Here are the most effective, India-specific strategies to preserve and grow your real wealth in 2026:

The Golden Rule: Earn > Inflation > Taxes

A simple framework for every financial decision: ask yourself whether the after-tax real return (return minus inflation minus tax) is positive. If it’s negative, your wealth is shrinking.

💡 Quick Win for 2026

If you have idle money in a savings account earning 2.5–3%, consider moving it to a liquid mutual fund or short-term debt fund. These currently yield 6.5–7.2% with near-identical liquidity — giving you an instant real-return improvement of 3–4 percentage points.

Conclusion: Inflation Is a Stealth Tax You Cannot Ignore

Inflation in India in 2026 is at a relatively benign 3.4% — but the story is more nuanced than the headline number suggests. Food inflation is higher, health and education costs rise faster, and the average Indian household faces a true inflation burden that can exceed 5–6%.

Most critically, the traditional Indian habit of saving in bank accounts is no longer enough. With savings rates at 2.5–3% and inflation averaging 4–5%, every rupee left idle in a savings account is a rupee slowly losing its value.

The solution is not to stop saving — it’s to save smarter. Invest in assets that generate real returns above inflation: equity mutual funds for the long term, PPF and Sovereign Gold Bonds for the conservative investor, and real estate or REITs for those with higher capital.

“Compound interest works for you with investing; inflation makes compound interest work against you with savings. Choose wisely.”

Key Takeaways

- India’s CPI inflation is 3.4% in March 2026; the FY26 annual average is ~4.5%

- Food inflation (3.87%) and health/education inflation consistently exceed the headline number

- A savings account earning 3% with 4.5% inflation means a real loss of –1.5% per year

- The RBI targets 4% inflation with a 2–6% band, renewed until March 2031

- Equity mutual funds, PPF, gold (SGBs), and real estate are the top inflation-beating instruments for Indian investors

- The “real return” = nominal rate − inflation. Always calculate this before choosing an investment

- WPI tracks wholesale prices; CPI tracks consumer prices — both matter, but RBI uses CPI