Health Insurance Claim Rejected?Here Is Why It Happens and How to Fight It

The Harsh Reality of Health Insurance Claims in India

You paid your premium faithfully every year, needed hospitalisation, filed your claim. And then came that dreaded letter — or worse, a WhatsApp message from your TPA — saying your health insurance claim has been rejected.

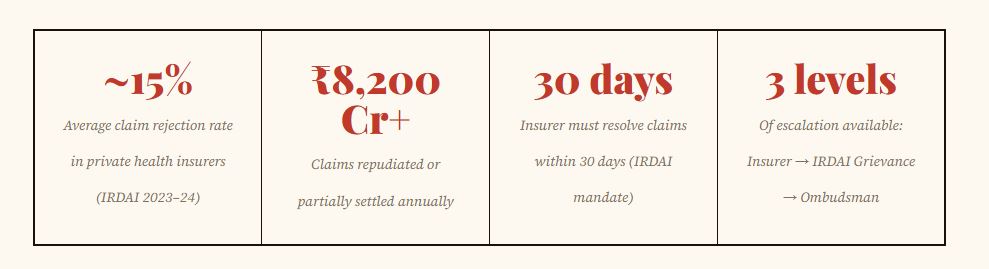

In India, health insurance claim rejections are far more common than insurers like to admit. According to data published by the Insurance Regulatory and Development Authority of India (IRDAI), thousands of health insurance claims are repudiated or partially settled every single year. With India’s out-of-pocket healthcare expenditure still among the highest in the world, a denied claim can push families into immediate financial distress.

The good news? A rejected claim is not the final word. Indian policyholders have legally protected rights — and if you know the system, you can fight back and win.

Top 10 Reasons Your Health Insurance Claim Gets Rejected in India

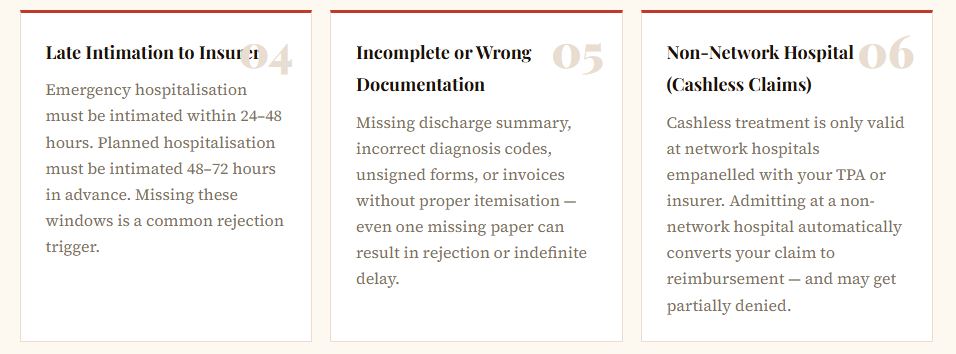

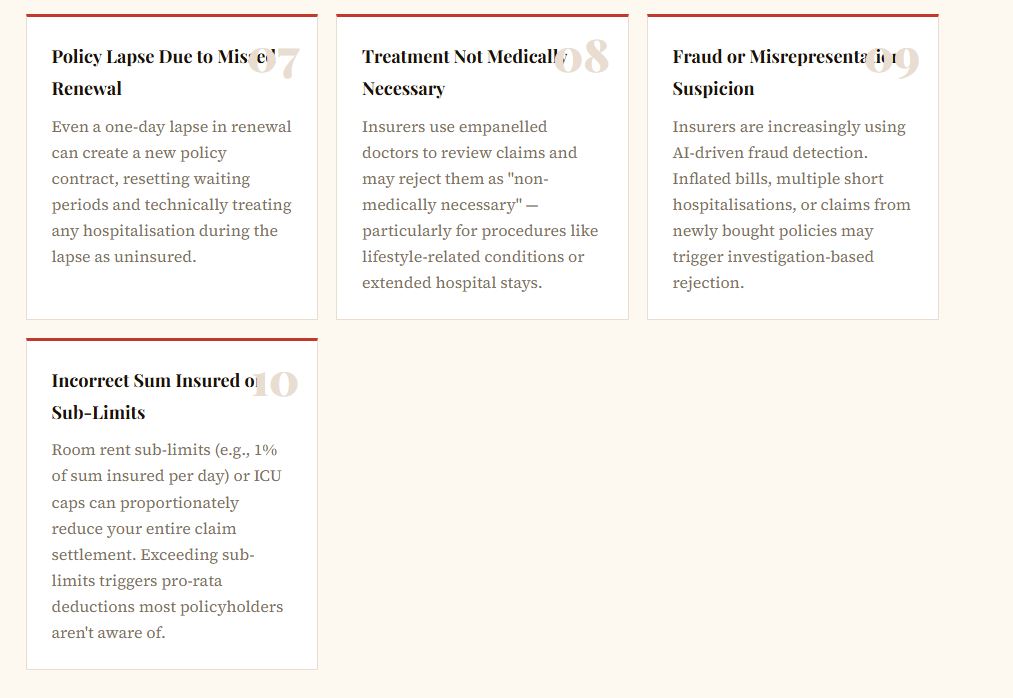

Knowing why claims get rejected is the first step to avoiding denial — and to challenging it if it happens. Here are the ten most common reasons, with context specific to Indian policyholders.

⚠ Critical India-Specific Issue

India has a unique “room rent sub-limit” problem. If your policy limits room rent to ₹3,000/day and you opted for a ₹6,000/day room, insurers proportionately reduce all other charges — including surgery, medicines, and doctor fees. This catches thousands of policyholders by surprise every year.

Why Cashless Claims Specifically Get Denied

Cashless hospitalisation is the most convenient benefit of health insurance — but it is also the most frequently denied at the pre-authorisation stage. Here’s what goes wrong:

“A cashless pre-auth denial is not a final claim rejection. Always pay and file for reimbursement — you preserve your legal right to appeal. Accepting a cashless denial without follow-up is the biggest mistake Indian policyholders make.”— Insurance Ombudsman Advisory, IRDAI

How to Fight a Rejected Health Insurance Claim: Step-by-Step

When your claim is rejected, you will receive a formal repudiation letter from your insurer (or TPA). This letter is your starting point. Here is exactly what to do next:

1. Read the Repudiation Letter Carefully

Understand the exact clause cited for rejection. Is it a policy exclusion? A procedural lapse (late intimation)? A documentation issue? The reason determines your appeal strategy. Insurers are required by IRDAI to specify the exact policy clause for rejection — if they haven’t, that itself is grounds for appeal.

2. Gather Your Complete Policy Document

Pull out your policy wording — not just the schedule card. Read the exact exclusion or clause cited. Many rejections are based on a misapplication of policy terms. In India, ambiguous policy language must be interpreted in favour of the policyholder (contra proferentem rule).

3. Get a Treating Doctor’s Letter

If your claim was rejected for “medical necessity” or wrong diagnosis code, ask your treating doctor to write a detailed letter explaining why the treatment was medically necessary. A specialist’s supporting letter significantly strengthens your appeal, especially for conditions like kidney stones, hernia, or back surgery.

4. File a Formal Written Appeal with the Insurer

Write a formal appeal letter to the insurer’s grievance officer within 15–30 days of receiving the rejection. Reference the specific policy clause, attach supporting documents, and state clearly why the rejection is incorrect. Send it via registered post AND email for a paper trail.

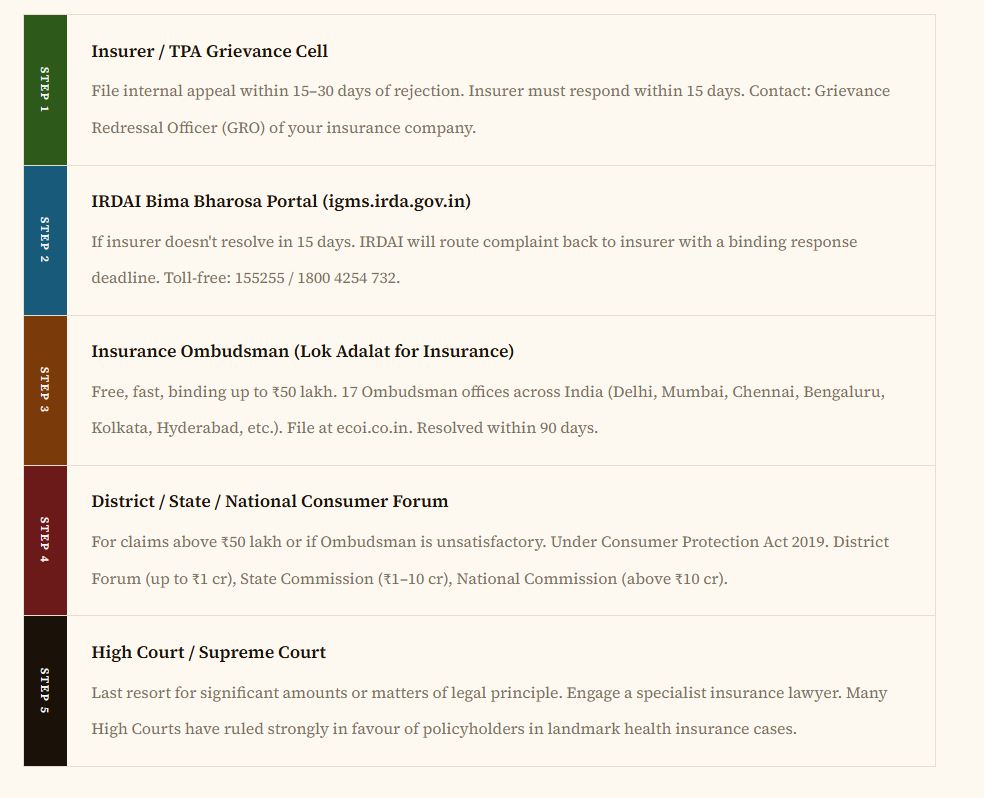

5. Escalate to IRDAI Bima Bharosa / IGMS Portal

If the insurer does not respond within 15 days or upholds the rejection unsatisfactorily, register a complaint on IRDAI’s Bima Bharosa portal (formerly IGMS) at igms.irda.gov.in. The insurer is now legally obligated to respond within a defined timeline.

6. Approach the Insurance Ombudsman

If the insurer still refuses, file a complaint with the Insurance Ombudsman for your region. The Ombudsman process is free, fast (resolution within 3 months), and binding on the insurer up to ₹50 lakh. You do not need a lawyer.

7. File in Consumer Court (If Needed)

For claims above ₹50 lakh, or if the Ombudsman does not rule in your favour, you can approach the District Consumer Forum under the Consumer Protection Act 2019. Courts have repeatedly ruled in favour of policyholders in cases of unfair claim rejection.

Pro Tip — Time Limits Matter

In India, you typically have 1 year from the date of rejection to approach the Ombudsman, and 2 years to file in Consumer Court. Do not delay — missing these windows forfeits your right to appeal.

Escalation Ladder: From Insurer to Ombudsman

India’s insurance grievance system has a clear hierarchy. Here is the complete escalation path with timelines:

Documents You Must Gather Before Filing an Appeal

A strong appeal is built on documentation. Collect every single one of these before submitting:

- Original claim repudiation / rejection letter from insurer or TPA

- Complete policy document including all endorsements and renewal schedules

- Hospital discharge summary (signed by treating doctor)

- All original hospital bills, receipts, and pharmacy invoices

- Treating doctor’s letter supporting medical necessity (fresh, detailed)

- Diagnostic test reports (pathology, radiology, ECG, MRI, etc.)

- Pre-authorisation request form and TPA’s denial letter (for cashless)

- Claim form submitted (original copy or acknowledgement)

- All communication (emails, letters, WhatsApp screenshots) with insurer/TPA

- Proof of timely premium payment and policy continuity

- Proposal form submitted at time of buying policy (to counter PED allegations)

- Any previous approvals for similar treatments under the same policy

Indian Context Note:- In India, many hospitals provide discharge summaries with vague or abbreviated ICD-10 diagnosis codes that TPAs can misinterpret. Always ask your treating doctor for a detailed narrative discharge summary in addition to the standard form — this can be decisive in appeal proceedings.

Prevention: How to Claim-Proof Your Health Insurance Policy

The best fight is one you never have to fight. Here is how to significantly reduce your risk of claim rejection in India:

At the Time of Buying the Policy

Declare every health condition you know of — even minor ones like acid reflux, mild hypertension, or vitamin D deficiency. Non-disclosure is the number one reason claims are denied years after purchase. The short-term benefit of a lower premium is never worth the long-term risk of full claim rejection.

Choose the Right Sum Insured and Room Rent

Avoid policies with room rent sub-limits (e.g., 1% of SI) if you live in a metro. Opt for policies that offer “any room category” or at least a high daily cap. A policy with ₹10 lakh SI but a ₹3,000/day room cap can result in 40–60% deduction on your entire bill in a private hospital.

Know Your Network Hospitals

Before any planned hospitalisation, confirm that your chosen hospital is on your insurer’s network list — and not just “empanelled” but currently active on the panel. Hospital-insurer empanelments change regularly, and many policyholders discover the hospital was delisted only after admission.

Intimate on Time — Always

Save your insurer’s and TPA’s helpline number in your phone right now. The moment a family member is hospitalised, call to intimate — even if documents are not ready. Verbal intimation followed by written documentation is acceptable and starts the clock on your coverage.

Never Do This– Never sign a blank or incomplete claim form, never allow the hospital billing department to fill out your claim forms without your review, and never accept a “partial settlement” without understanding what the insurer is deducting and why. Once you accept a partial settlement in writing without protest, it weakens your right to recover the balance.

Do a “Claim Readiness Audit” Every Year at Renewal

At each renewal, update your insurer on any new diagnoses, medications, or surgeries from the past year. Ask your insurer to issue a written confirmation of coverage for any pre-existing conditions. This paper trail protects you against future disputes.

Final Word: Your Claim is Worth Fighting For

Health insurance claim rejection is distressing — but it is not the end of the road. India’s insurance regulatory framework, while imperfect, gives policyholders real tools to push back: internal appeals, IRDAI intervention, the Ombudsman mechanism, and the Consumer Forum.

The most important things to remember: act fast, document everything, know your policy, and do not accept a rejection without understanding exactly why it happened and whether it is legally correct.

The system is complex, but thousands of policyholders win their appeals every year. With the right approach, you can be one of them.