Income Tax Saving Options for Employees in India (FY 2026-27)

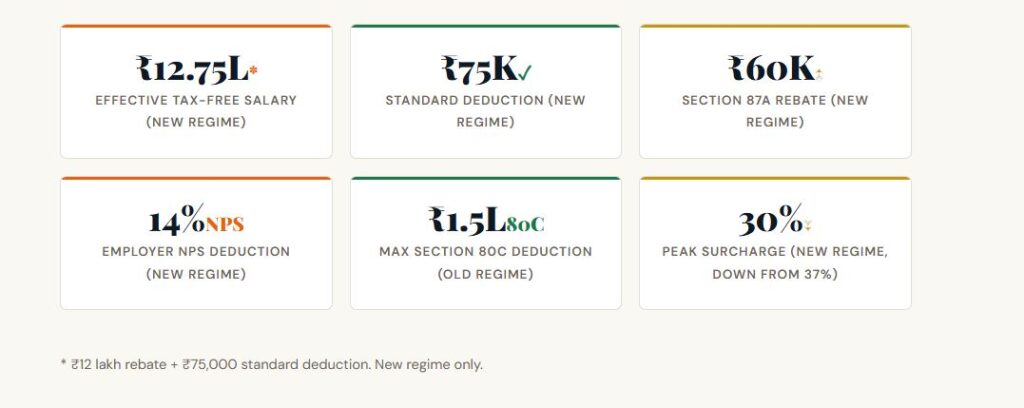

The Union Budget 2026 kept income tax rules for salaried individuals unchanged for FY 2026–27. This means all the powerful reforms from Budget 2025 — including the ₹12 lakh rebate, ₹75,000 standard deduction under the new regime, and a 14% NPS employer contribution deduction — are fully in play. Here is your definitive, jargon-free guide to keeping more of your salary in your pocket.

01. Key Numbers for FY 2026–27

Before diving into strategies, let’s anchor on the numbers that matter most for salaried taxpayers this year.

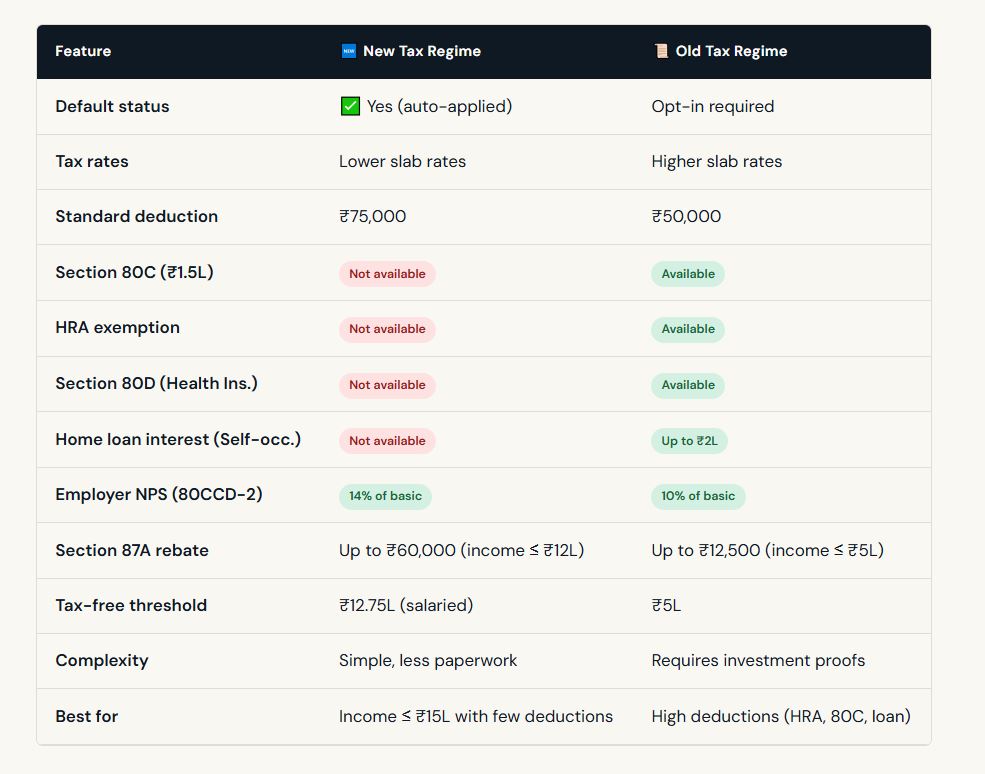

02. Old Regime vs. New Regime — Which Is Better?

This is the most important decision you’ll make. The new tax regime is now the default — you must actively opt out to use the old one. Here’s an honest head-to-head comparison:

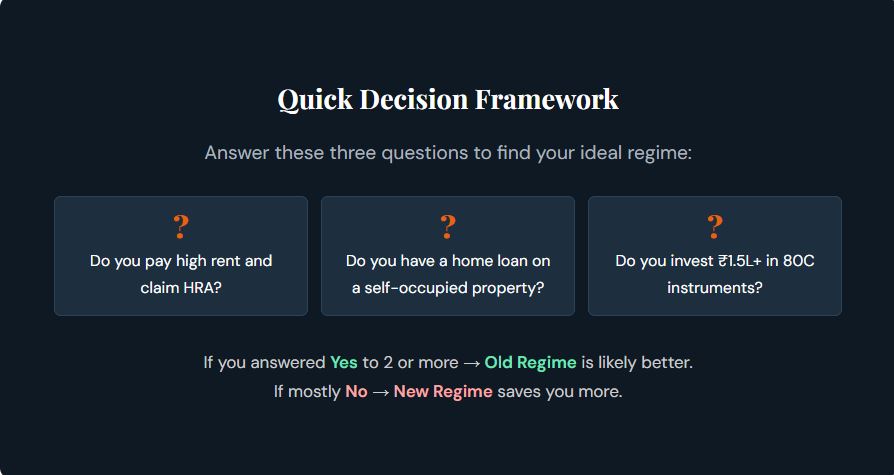

Rule of Thumb: If your total deductions (80C + HRA + 80D + home loan interest) exceed ₹3.5–4 lakh, the old regime is likely better. For everyone else — especially those earning under ₹15 lakh with minimal investments — the new regime typically wins.

03. Tax Slab Rates for FY 2026–27

The slabs below are effective for FY 2026–27 (Assessment Year 2027–28). Add 4% Health & Education Cess to the final tax amount.

04. Old Regime: Every Deduction Explained

If you’ve opted for the old regime, here is every weapon in your arsenal:-

Section 80C — The Big One (Up to ₹1,50,000)

The most popular deduction in the Indian tax code. Invest in any of the following and reduce your taxable income by up to ₹1.5 lakh:

- ELSS Mutual Funds — Highest return potential, shortest 3-year lock-inNo sub-limit

- PPF (Public Provident Fund) — Government-backed, 7.1% interest, 15-year tenure, fully tax-free returns₹1.5L/year max

- Employee Provident Fund (EPF) — Auto-deducted from salary; employer’s share is extraCounts within ₹1.5L

- National Savings Certificate (NSC) — Post office scheme, 7.7% p.a., 5-year lock-inNo sub-limit

- 5-Year Tax Saver FD — Bank fixed deposits with 5-year lock-inUp to ₹1.5L

- Life Insurance Premium — Term plan or endowment policiesNo sub-limit

- Sukanya Samriddhi Yojana (SSY) — For girl child, 8.2% interest, fully exempt₹1.5L/year max

- Home Loan Principal Repayment — EMI principal component qualifiesWithin ₹1.5L cap

- Children’s Tuition Fees — For up to 2 children, full-time education in IndiaWithin ₹1.5L cap

Old + New Regime Common-

Section 80CCD — National Pension System (NPS)

NPS offers deductions across three sub-sections — and one of them works in the new regime too:

- 80CCD(1) — Your own NPS contribution (part of 80C umbrella) Up to ₹1.5L (old regime)

- 80CCD(1B) — Additional NPS contribution over and above 80C Extra ₹50,000 (old regime)

- 80CCD(2) — Employer’s NPS contribution – Available in new regime 14% of basic (new) / 10% (old)

🏆Pro Tip: 80CCD(1B) gives you ₹50,000 in extra deduction on top of the ₹1.5L 80C limit — a total of ₹2L in NPS-related savings in the old regime. Ask your employer to route more as NPS contribution to leverage 80CCD(2) even in the new regime.

Old Regime Only

HRA — House Rent Allowance Exemption

If you live in a rented house and receive HRA from your employer, you can claim an exemption. The exempt amount is the lowest of:

- Actual HRA received from employer

- 50% of basic salary (metro cities) or 40% (non-metro)

- Actual rent paid minus 10% of basic salary

⚠️Rent paid above ₹1 lakh/year requires the landlord’s PAN. If you pay rent to a parent and claim HRA, the parent must show it as rental income in their own ITR.

Section 80D — Health Insurance Premium

- Premium for self, spouse & childrenUp to ₹25,000

- Premium for parents (below 60)Up to ₹25,000 extra

- Premium for senior citizen parents (60+)Up to ₹50,000 extra

- Maximum possible deduction (if parents are 60+)₹75,000 total

Section 24(b) — Home Loan Interest

Interest paid on a home loan qualifies for deduction under Section 24(b):

- Self-occupied property — interest deductionUp to ₹2,00,000/year

- Let-out property — no upper limit, available in both regimesEntire interest

Other Deductions Worth Knowing

- Section 80E — Interest on education loan (no upper limit, 8 years)Entire interest

- Section 80G — Donations to eligible charitable institutions50%–100% of donation

- Section 80TTA — Interest on savings bank accountUp to ₹10,000

- Section 80TTB (Senior Citizens only) — Interest on depositsUp to ₹50,000

- LTA (Leave Travel Allowance) — Travel within India for self & family (2 journeys/4 years)Actual travel cost

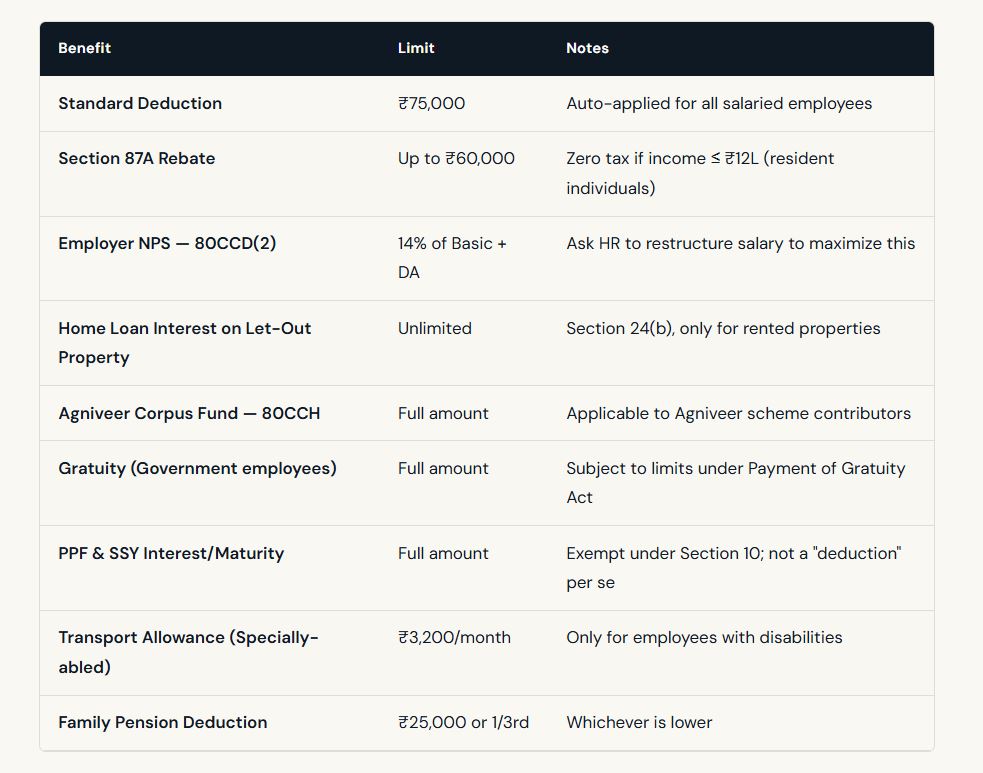

05. New Regime: What You Can Still Claim

The new regime isn’t a total blank slate. These deductions and exemptions survive:-

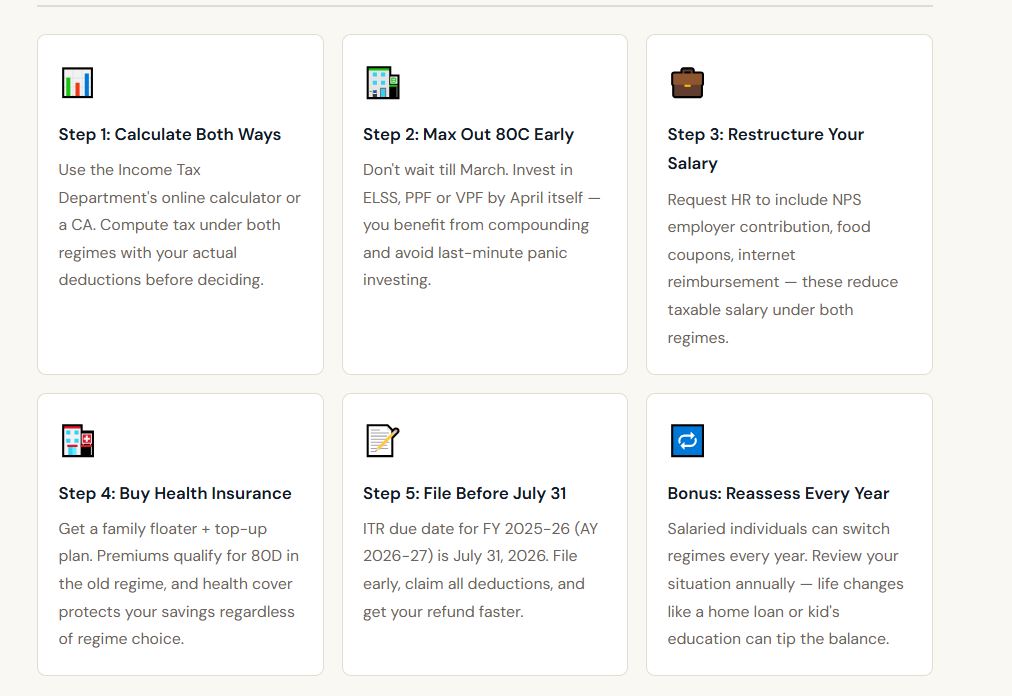

06. Your 5-Step Tax-Saving Action Plan

Disclaimer: This article is for informational and educational purposes only. Tax laws are subject to change. Visit income tax india. Always consult a qualified Chartered Accountant or tax advisor before making financial decisions.