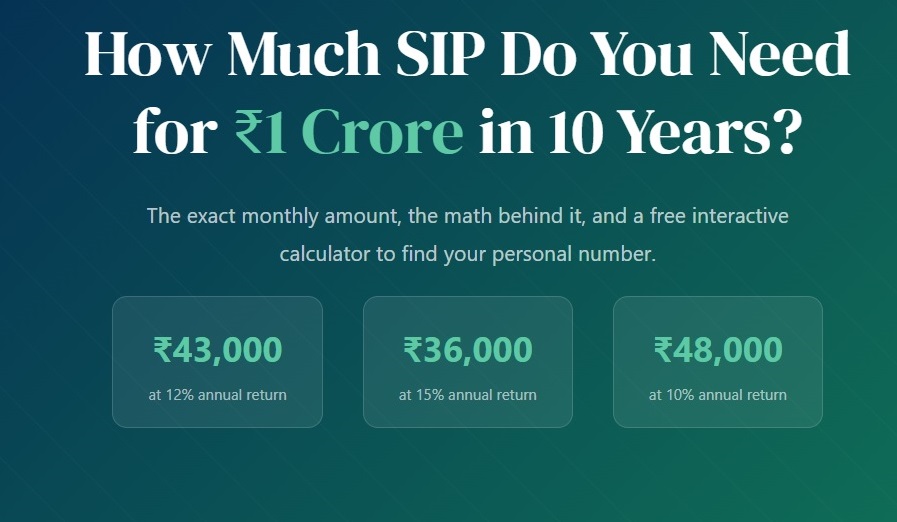

Every Indian investor dreams of the magic number — ₹1 Crore. But how close are you to it? If you have 10 years and a disciplined SIP, you might be closer than you think.

SIP (Systematic Investment Plan) is one of the most powerful wealth-building tools available to retail investors in India. The beauty of SIP is not just in the returns — it’s in the power of compounding and rupee-cost averaging. But the real question is: what’s the exact number you need to invest every month?

In this guide, we break down the math, give you a complete comparison table across different return scenarios, and offer a free interactive SIP calculator so you can plug in your own numbers.

The SIP Formula Explained

The standard SIP future value formula is:

FV = P × [ ((1 + r)ⁿ − 1) / r ] × (1 + r)

Where: P = Monthly SIP | r = Monthly return rate (Annual ÷ 12) | n = Number of months (Years × 12)

To find how much SIP you need for a target amount, you reverse-engineer this formula. You plug in ₹1,00,00,000 as the Future Value and solve for P (monthly SIP amount).

What Does “Rate of Return” Mean in Practice?

The assumed rate of return depends on the type of mutual fund you choose:

- Debt Funds: 6–8% annually — low risk, lower returns

- Balanced/Hybrid Funds: 9–11% annually — moderate risk

- Large-Cap Equity Funds: 10–13% annually — moderate-high risk

- Mid-Cap/Small-Cap Funds: 13–18% annually — high risk, high reward

- Flexi-Cap / Multi-Cap Funds: 12–15% annually — diversified, popular choice

Mutual fund returns are market-linked and not guaranteed. Past performance is not indicative of future results. The figures used here are illustrative projections only. Please consult a SEBI-registered financial advisor before investing.

SIP Amount by Return Rate — Complete Table

Here’s a comprehensive table showing exactly how much monthly SIP you need at various expected annual return rates to accumulate ₹1 Crore in 10 years:

| Expected Annual Return | Monthly SIP Needed | Total Amount Invested | Wealth Gain (Returns) | Fund Category |

|---|---|---|---|---|

| 6% | ₹61,016 | ₹73,21,920 | ₹26,78,080 | Debt / Liquid |

| 8% | ₹54,642 | ₹65,57,040 | ₹34,42,960 | Debt / Conservative Hybrid |

| 10% | ₹48,819 | ₹58,58,280 | ₹41,41,720 | Large-Cap / Balanced |

| 12% ⭐ Most Common | ₹43,474 | ₹52,16,880 | ₹47,83,120 | Flexi-Cap / Large-Mid Cap |

| 14% | ₹38,556 | ₹46,26,720 | ₹53,73,280 | Mid-Cap / Multi-Cap |

| 15% | ₹36,213 | ₹43,45,560 | ₹56,54,440 | Mid-Cap / Small-Cap |

| 18% | ₹30,047 | ₹36,05,640 | ₹63,94,360 | Small-Cap / Sectoral |

Notice how at 12% — a commonly used benchmark for equity mutual funds — you need approximately ₹43,474 per month. At 15% return (aggressive funds), you need about ₹36,213. This difference of ~₹7,000/month compounds massively over time.

At 12% return, out of your ₹1 Crore target, only ₹52 lakhs is your own money. The remaining ₹48 lakhs is pure interest/return. This is the magic of compounding!

Interactive SIP Calculator

Use the calculator below to find the exact SIP needed for any target amount, timeframe, and expected return rate. Adjust the sliders and see results update instantly.

🧮 SIP Goal Calculator

Find your monthly SIP amount for any wealth goal

Best Mutual Funds to Consider for 10-Year SIP

While fund selection requires personal due diligence, here are categories of funds commonly used for 10-year SIP goals (not investment advice — please research and verify):

Historical returns do NOT guarantee future performance. Small-cap and mid-cap funds carry higher volatility. Always diversify and match your fund selection to your risk tolerance and time horizon. Consult a SEBI-registered investment advisor.

5 Pro Tips to Reach ₹1 Crore Faster

Use Step-Up SIP (Increase by 10% every year)

Instead of a flat SIP, increase your contribution by 10% each year. A ₹30,000/month SIP with 10% annual step-up can reach ₹1 Crore in 10 years at just 12% — vs ₹43,474 flat. This mirrors your salary growth and dramatically reduces the starting burden.

Start Early — Every Year Matters

Starting your SIP at 25 vs 30 doesn’t just give you 5 more years — it can halve your required monthly investment. Time in the market is your greatest free asset.

Diversify Across Fund Categories

Split your SIP across large-cap (stability), flexi-cap (balanced growth), and mid/small-cap (alpha generation). A 50:30:20 split is a popular starting point for moderate-risk investors.

Never Stop During Market Crashes

Market crashes are the best time for SIP investors. You buy more units at lower prices — which drives massive returns when markets recover. Pausing your SIP during downturns is the most common and costly mistake.

Review and Rebalance Annually

Review your portfolio every 12 months. If a fund consistently underperforms its benchmark over 3+ years, consider switching. But don’t churn frequently — transaction costs and tax implications add up.

Step-Up SIP vs Flat SIP — Comparison

| SIP Strategy | Starting Monthly SIP | Assumed Return | Goal Achieved? | Total Invested |

|---|---|---|---|---|

| Flat SIP | ₹43,474 | 12% | ✅ ₹1 Crore | ₹52.17 Lakhs |

| Step-Up SIP (10%/yr) | ₹29,500 | 12% | ✅ ₹1 Crore | ₹56.32 Lakhs |

| Step-Up SIP (15%/yr) | ₹24,000 | 12% | ✅ ₹1 Crore | ₹57.90 Lakhs |

Step-Up SIP at 10% annual increment lowers your starting SIP from ₹43,474 to just ₹29,500 — a saving of nearly ₹14,000/month in year one!

Common SIP Mistakes to Avoid

- Stopping SIP during market corrections — This kills your rupee-cost averaging benefit

- Chasing last year’s top performer — Past performance ≠ future returns

- Investing without an emergency fund — SIPs shouldn’t be redeemed in emergencies; keep 6 months of expenses liquid

- Ignoring expense ratio — A 1% difference in expense ratio compounds significantly over 10 years

- Not linking SIP to a goal — Goal-less investing leads to early redemption; always know your “why”

- Overlooking tax implications — LTCG above ₹1 lakh/year from equity funds is taxed at 10%; factor this into planning

Frequently Asked Questions

Ready to Start Your ₹1 Crore Journey?

Use our free tools, read more SIP guides, and join thousands of smart investors at NerdyFinance.

Explore More Guides on NerdyFinance →