ELSS Mutual Funds: Your Complete Guide to Tax-Saving Investments in India

If you’re like most Indians scrambling to save tax as March 31st approaches, you’ve probably heard your colleagues, friends, or that uncle at family gatherings mention “ELSS Mutual Funds.” But what exactly is it? More importantly, should you be investing in it?

Let me break it down for you in plain language, just like I’m explaining it to a friend over chai.

What is ELSS? (The Basics First)

ELSS stands for Equity Linked Savings Scheme. Think of it as a mutual fund that invests primarily in equity (stocks) while also giving you tax benefits under Section 80C of the Income Tax Act.

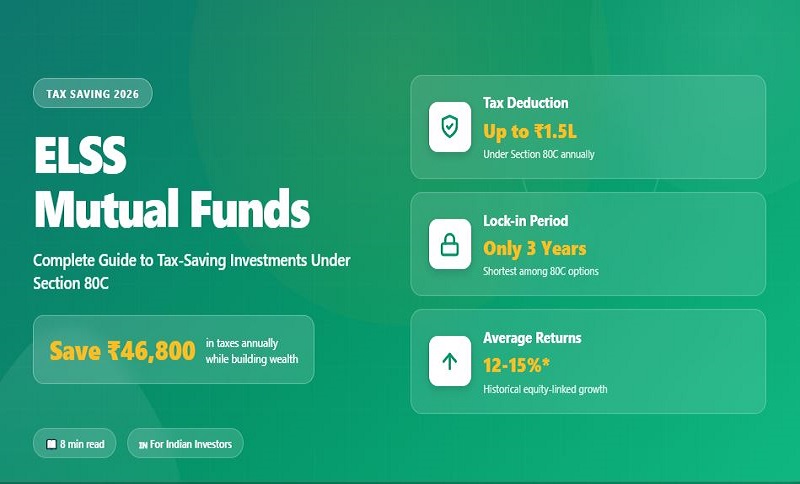

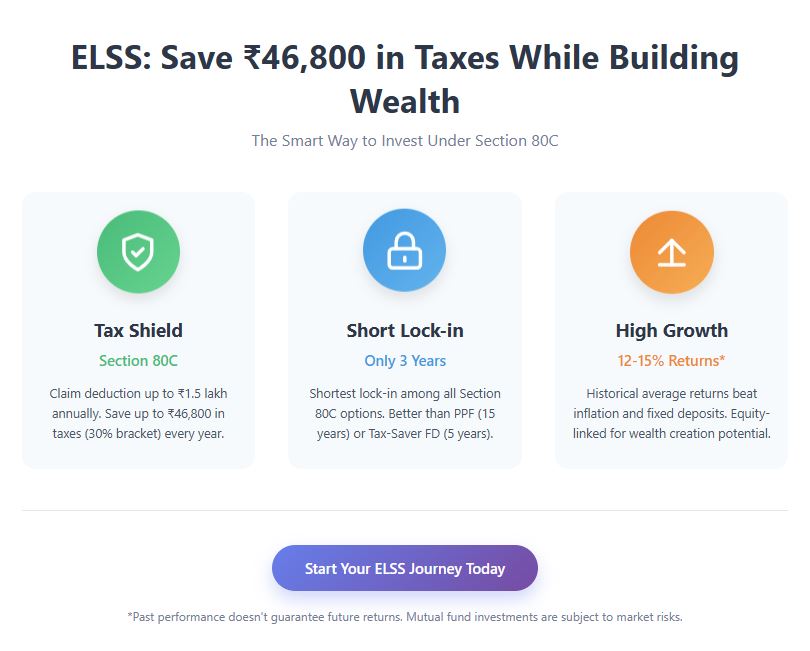

Here’s what makes ELSS special: you can claim a deduction of up to ₹1.5 lakh from your taxable income every year. That means if you’re in the 30% tax bracket, you could save up to ₹46,800 in taxes annually (including cess). Not bad, right?

Why ELSS Stands Out Among Tax-Saving Options

You have several options under Section 80C—PPF, NSC, tax-saver fixed deposits, life insurance premiums, and ELSS. So why choose ELSS Mutual Funds?

The shortest lock-in period: ELSS has just a 3-year lock-in, compared to 5 years for tax-saver FDs and 15 years for PPF. Your money isn’t locked away forever.

Potential for higher returns: Unlike PPF or fixed deposits that give you fixed returns of around 7-8%, ELSS invests in equities and has historically delivered returns of 12-15% over the long term. Of course, these aren’t guaranteed—that’s the trade-off with market-linked investments.

Wealth creation along with tax saving: While other 80C options focus purely on saving tax, ELSS helps you build wealth simultaneously. It’s like hitting two birds with one stone.

How Does ELSS Mutual FundsWork? A Simple Example

Let’s say you’re Priya, a software engineer in Bangalore earning ₹12 lakh annually. Without any deductions, you’d pay around ₹1.4 lakh in taxes (old regime, 30% bracket).

Now, Priya invests ₹1.5 lakh in ELSS. Her taxable income drops to ₹10.5 lakh, reducing her tax liability by approximately ₹46,800. That’s immediate savings in her pocket.

But here’s where it gets interesting: that ₹1.5 lakh grows in the equity market. If her ELSS generates 12% returns annually, after the 3-year lock-in period, her investment could be worth around ₹2.1 lakh. She saved tax AND grew her wealth.

Understanding the Lock-in Period

The 3-year lock-in means you cannot withdraw or redeem your investment before this period ends. It’s calculated from the date of each SIP installment or lump sum investment.

If you invest ₹5,000 every month via SIP, each installment has its own 3-year lock-in. So your January 2026 SIP unlocks in January 2029, your February SIP unlocks in February 2029, and so on.

Who Should Invest in ELSS?

ELSS is ideal if you:

- Want to save tax under Section 80C

- Have a risk appetite for equity markets

- Can stay invested for at least 3-5 years (though the lock-in is 3 years, longer horizons work better for equity)

- Are looking for inflation-beating returns

- Want to build wealth alongside tax saving

ELSS might NOT be for you if:

- You need guaranteed returns

- You cannot handle market volatility

- You might need the money within 3 years

- You’re nearing retirement and have low risk tolerance

ELSS vs Other 80C Options: A Quick Comparison

ELSS vs PPF: PPF is safer with guaranteed returns but locks your money for 15 years and gives lower returns. ELSS offers potentially higher returns with just 3 years lock-in but comes with market risk.

ELSS vs NSC: NSC offers fixed returns (currently around 7.7%) with 5-year maturity. ELSS has historically outperformed but doesn’t guarantee returns.

ELSS vs Tax-Saver FD: FDs are the safest but have 5-year lock-in and lower returns. Interest is taxable at your slab rate, whereas ELSS enjoys equity taxation benefits.

ELSS vs Life Insurance: Term insurance premiums qualify for 80C, but insurance and investment should ideally be separate. If you need insurance, buy pure term insurance. For wealth creation, ELSS is more efficient.

Tax Benefits: How Much Can You Really Save?

Under Section 80C, you can invest up to ₹1.5 lakh in ELSS and claim that entire amount as a deduction from your taxable income.

Here’s what that means in real savings:

- If you’re in the 30% tax bracket: Save up to ₹46,800

- If you’re in the 20% tax bracket: Save up to ₹31,200

- If you’re in the 5% tax bracket: Save up to ₹7,800

Remember, these are tax deductions, not exemptions. You reduce your taxable income, which then lowers your tax liability based on your bracket.

What About Taxation on Returns?

When you redeem your ELSS after the lock-in period, the gains are taxed as Long Term Capital Gains (LTCG). As per current tax laws:

- LTCG up to ₹1.25 lakh per financial year is tax-free

- LTCG above ₹1.25 lakh is taxed at 12.5%

This is quite favorable compared to fixed deposits where interest is fully taxable at your slab rate.

How to Choose the Right ELSS Fund

Not all ELSS funds are created equal. Here’s what to look for:

Past performance: Check returns over 3, 5, and 10 years. While past performance doesn’t guarantee future returns, it shows consistency.

Fund manager track record: A good fund manager makes a real difference in equity funds.

Expense ratio: Lower is better. An expense ratio above 2% can eat into your returns significantly.

Asset allocation: See where the fund invests—large-cap, mid-cap, small-cap. Choose based on your risk appetite.

Consistency: A fund that gives 10% consistently is better than one giving 20% one year and -5% the next.

Some well-regarded ELSS funds in India include Axis Long Term Equity Fund, Mirae Asset Tax Saver Fund, and Quant Tax Plan, but do your own research or consult a financial advisor before investing.

SIP or Lump Sum: What Works Better?

Both have their place, but here’s my take:

SIP (Systematic Investment Plan) is better if you’re salaried and want to invest regularly. Monthly SIPs of ₹12,500 will get you to the ₹1.5 lakh annual limit. Benefits include rupee cost averaging and disciplined investing.

Lump sum works if you have a bonus, inheritance, or year-end savings. You can invest the full ₹1.5 lakh in one go, usually in January-March when people rush for tax savings.

Pro tip: Don’t wait until March to invest. The earlier in the financial year you invest, the more time your money has to grow.

Common Mistakes to Avoid

Investing only for tax saving: Many invest in March, get the tax benefit, and forget about it. Choose quality funds that can grow your wealth.

Ignoring risk: Just because it saves tax doesn’t mean it’s risk-free. ELSS invests in equities and can be volatile.

Comparing with fixed-return options: Don’t expect guaranteed returns. Some years will be great, others might be flat or negative.

Not diversifying: Don’t put all your Section 80C limit into ELSS alone. Consider a mix based on your risk profile.

Withdrawing immediately after 3 years: While you can, equity investments work better over 5+ years. Let your money compound.

Real Talk: The Risks You Should Know

I won’t sugarcoat it—ELSS comes with risks:

Market volatility: Your investment value can go down, especially in the short term. During market crashes like March 2020, ELSS funds fell significantly (though they recovered later).

No guaranteed returns: Unlike PPF or FDs, there’s no certainty of returns.

Lock-in means no liquidity: You cannot access your money for 3 years, no matter what emergency arises.

That said, for long-term wealth creation with tax benefits, ELSS remains one of the most efficient options available to Indian taxpayers.

How to Invest in ELSS

Investing is straightforward:

- Decide your budget: How much can you invest? Up to ₹1.5 lakh qualifies for deduction.

- Choose your fund: Research and select based on the criteria mentioned above.

- Complete KYC: If you haven’t invested in mutual funds before, complete your KYC (PAN, Aadhaar, bank details).

- Invest directly or through platforms: You can invest through the fund house website, apps like Groww, Zerodha Coin, ET Money, or through a financial advisor.

- Set up SIP or invest lump sum: Choose what works for your cash flow.

- Get your ELSS certificate: You’ll receive proof of investment for filing your tax returns.

ELSS in the New vs Old Tax Regime

Here’s an important consideration for 2026: under the new tax regime (which became default from FY 2023-24), most deductions including Section 80C are not available.

So ELSS tax benefits only work if you opt for the old tax regime. Do the math to see which regime works better for you. For many people, especially those who maximize 80C deductions, the old regime still comes out ahead.

If you’re in the new regime for better tax rates, you can still invest in ELSS—you just won’t get the tax deduction. But it remains a good equity mutual fund option.

Final Thoughts: Is ELSS Right for You?

ELSS is not a magic bullet, but it’s one of the most efficient tax-saving cum wealth-creation tools available to Indians. It combines the tax benefits of traditional investments with the growth potential of equities.

The key is to invest with the right expectations:

- Don’t expect guaranteed returns

- Stay invested beyond the 3-year lock-in

- Choose quality funds, not just any ELSS

- Treat it as part of your overall financial plan

Whether you’re a first-time taxpayer or a seasoned investor, ELSS deserves a place in your portfolio—assuming you’re comfortable with equity exposure and are investing for the long term.

Remember, the best time to start investing was yesterday. The second best time is today. Don’t wait until March 31st!

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Markets are subject to risks. Please consult a certified financial advisor before making investment decisions. Tax laws can change, so verify current rules before investing.

Have you invested in ELSS? What’s been your experience? Share in the comments below!

One thought on “ELSS Mutual Funds: Your Complete Guide to Tax-Saving Investments in India”