India’s UPI Revolution: The Digital Payment System Changing the World

A ₹10 cup of tea in Mumbai, farm seeds in Rajasthan, or dinner in Singapore—India’s UPI app is making payments instant, simple, and global. Wherever you are, your money moves with just a tap. This isn’t science fiction—this is India’s digital payment reality in 2026, where India’s UPI revolution is changing the world for digital payments.

The Numbers Tell an Incredible Story

India’s digital payments market has undergone a transformation that few countries can match. From a market valued at $3.3 trillion in 2023, projections suggest growth to $10 trillion by 2026—a threefold expansion in just three years. This isn’t just growth; it’s a financial revolution.

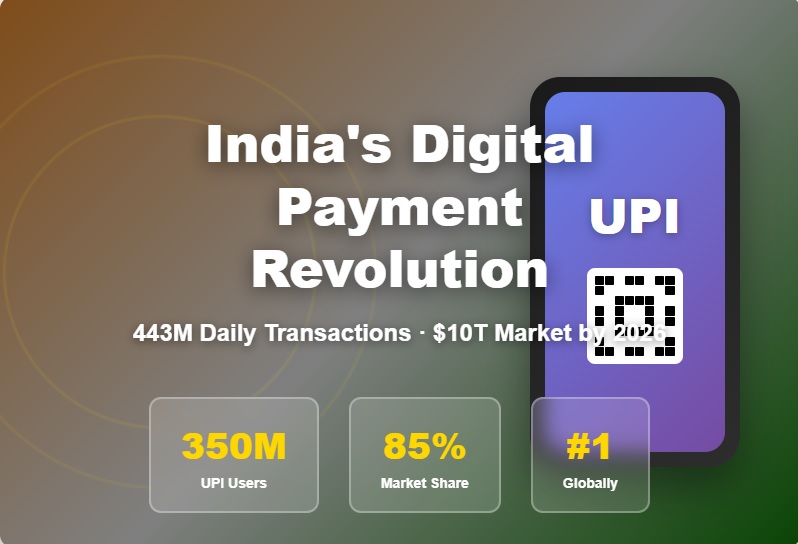

The backbone of this transformation is the Unified Payments Interface (UPI), which has achieved what seemed impossible just a decade ago. As of January 2026, UPI boasts 350 million users across India and processes an astounding 443 million transactions every single day. To put this in perspective, UPI now handles approximately 640 million transactions daily, surpassing even Visa’s 639 million daily transactions to become the world’s largest real-time payments system.

December 2025 marked a historic milestone when UPI transactions crossed 21 billion in a single month. Even more remarkable: UPI now powers nearly 50% of all global real-time digital payments and accounts for 85% of all digital transactions within India.

From Street Vendors to Shopping Malls: The Democratization of Digital Payments

What makes India’s digital payment revolution truly transformative is its reach across all economic strata. Unlike digital payment systems in many developed nations that primarily serve high-value transactions, UPI has become the default payment method even for life’s smallest purchases.

Data from August 2024 reveals that Person-to-Merchant (P2M) transactions account for 62.40% of all UPI activity, with 85% of these transactions valued at ₹500 or less. The volume of transactions under ₹100 has increased manifold, demonstrating that UPI has successfully digitized the cash-based micro-economy that defines much of India’s commerce.

Tea stalls, local kirana stores, auto-rickshaw rides, and street vendors—establishments that once dealt exclusively in cash—now routinely accept digital payments. This isn’t just convenient; it’s transformative for financial inclusion, taxation, and economic transparency.

The Giants Leading the Charge

PhonePe has emerged as the dominant force in India’s digital payments landscape, commanding a 48.3% market share of all UPI transactions. With 380 million registered users—meaning one in four Indians uses PhonePe—the platform has digitized over 30 million offline merchants covering 99% of India’s pin codes.

The competitive landscape has driven innovation and expansion at breakneck speed. Mobile wallet users have surpassed 500 million in 2026, and approximately 65% of small businesses now accept UPI or mobile wallet payments. Active UPI QR codes have grown by 21% over the past year alone, creating a ubiquitous payment infrastructure that spans from metropolitan cities to rural villages.

Beyond Metro Cities: The Tier 3-6 Revolution

One of the most significant aspects of this digital transformation is its geographic spread. Tier 3-6 cities have contributed 60-70% of new customers over the past two years, demonstrating that digital payments aren’t just an urban phenomenon. UPI adoption has surged from 35% in FY21 to an expected 75% within the next five years, with much of this growth coming from smaller towns and rural areas.

This geographic expansion has been fueled by rising internet penetration, smartphone affordability, government initiatives like Digital India, and the sheer convenience and security that digital payments offer compared to carrying cash.

Going Global: UPI’s International Expansion

India isn’t keeping this innovation to itself. UPI is now operational in seven countries including the UAE, Singapore, Bhutan, Nepal, Sri Lanka, France, and Mauritius. Indian travelers can use their familiar UPI apps abroad, while these countries benefit from a proven, efficient payment infrastructure.

India is now focusing expansion efforts in East Asia, potentially bringing its digital payment revolution to billions more people. This global expansion positions Indian fintech companies and the UPI framework as serious competitors to established international payment networks.

The Investment Landscape: Opportunities in the Digital Payment Ecosystem

The explosive growth of digital payments has created a thriving ecosystem of investment and business opportunities:

Fintech Innovation: Companies building on UPI infrastructure are developing solutions for lending, insurance, wealth management, and financial services that leverage the massive transaction data generated daily.

Merchant Services: Payment gateway providers, point-of-sale solutions, and merchant acceptance tools represent significant opportunities as millions more businesses come online.

Rural Penetration: Companies focused on bringing digital payments to India’s remaining unbanked or underbanked populations have substantial growth potential.

Cross-Border Solutions: As UPI expands internationally, businesses facilitating cross-border payments and currency conversion will find fertile ground.

QR Code Infrastructure: The hardware and software behind India’s QR code revolution continues to evolve, creating opportunities in hardware manufacturing, software development, and merchant onboarding.

Cybersecurity: With hundreds of millions of daily transactions, the need for robust security, fraud detection, and consumer protection creates opportunities for specialized security firms.

What’s Driving This Unprecedented Growth?

Several factors have converged to create India’s digital payment revolution:

Zero Transaction Fees: Unlike credit card networks that charge merchants 2-3%, UPI transactions are essentially free, making them viable even for small-value purchases.

Interoperability: Any UPI app can pay any merchant QR code, regardless of which bank or platform either party uses—a level of interoperability rarely seen in payment systems globally.

Government Support: Initiatives like Digital India, demonetization’s push away from cash, and regulatory frameworks that encourage innovation while ensuring security have all played crucial roles.

Smartphone Penetration: Affordable smartphones and cheap data plans have brought hundreds of millions of Indians online, creating the infrastructure necessary for digital payments.

Cultural Shift: Indians have rapidly embraced digital payments, moving from skepticism to preference in less than a decade—a cultural transformation as significant as the technological one.

Challenges on the Horizon

Despite the remarkable success, challenges remain. Digital literacy gaps still exist, particularly among older populations and in remote areas. Cybersecurity concerns and fraud attempts require constant vigilance and technological upgrades. Infrastructure issues like internet connectivity in remote regions can hinder transactions. Regulatory evolution must keep pace with innovation to ensure consumer protection without stifling growth.

The Road Ahead

As we move through 2026, India’s digital payment revolution shows no signs of slowing. The projected growth to a $10 trillion market appears not just achievable but potentially conservative. With UPI continuing to add features, expand internationally, and penetrate deeper into rural India, the transformation of how a billion-plus people handle money is still in its early chapters.

For investors, entrepreneurs, and policymakers worldwide, India’s digital payment story offers valuable lessons in how technology, policy, and cultural adoption can converge to create transformative change. For Indians, it represents a future where financial services are accessible, affordable, and available to everyone—from the street vendor to the corporate executive.

The revolution isn’t just about technology; it’s about financial inclusion, economic transparency, and empowering every Indian to participate fully in the modern economy. And if current trends continue, India’s digital payment infrastructure may well become the global standard for how nations can leapfrog traditional banking systems to create truly inclusive financial ecosystems.

One thought on “India’s UPI Revolution: The Digital Payment System Changing the World”