Do you know the truth of banks ? Read this now

Have you ever wondered how your bank can afford those sprawling branches across every city, the endless advertising campaigns, and still offer you free chequebooks? Indian banks are among the most profitable institutions in the country, yet most account holders don’t fully understand how they actually make their money. Let’s decode the business model of Indian banking.

The Interest Rate Game: Borrowing Cheap, Lending Dear

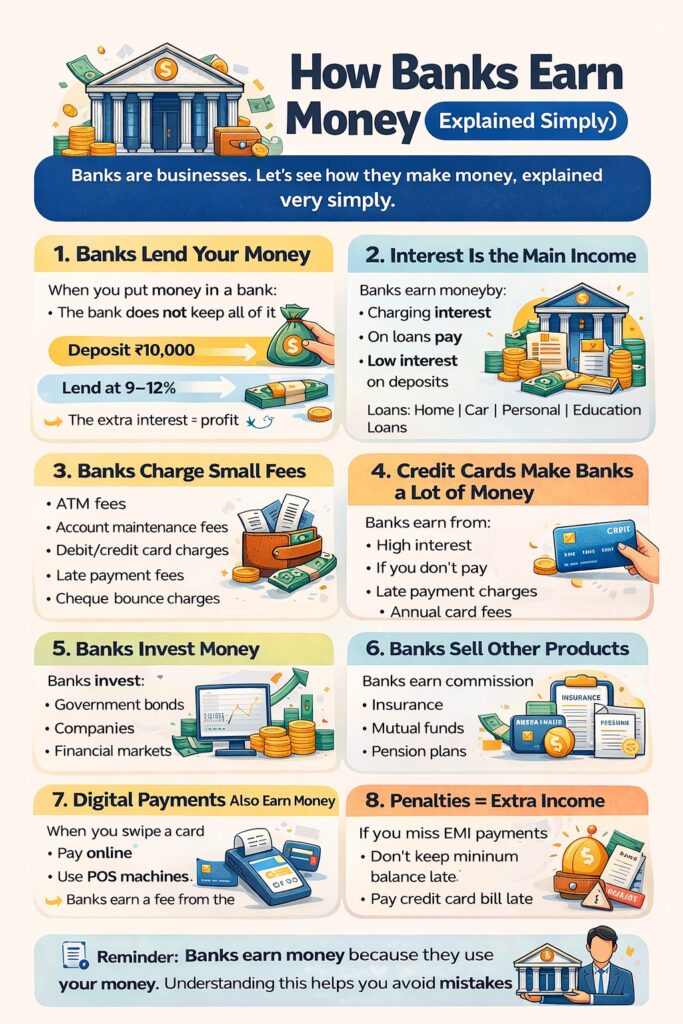

The primary way Indian banks earn money is through the spread between what they pay depositors and what they charge borrowers. This is the foundation of banking in India.

When you keep ₹1 lakh in your savings account earning 3-4% interest per annum, the bank doesn’t simply store it in a locker. They lend this money to a home loan customer at 8-9%, a personal loan seeker at 11-15%, or a credit card user at 36-42% per annum. The difference between these rates is the bank’s profit margin.

For instance, if a bank pays you ₹3,500 as interest on your ₹1 lakh savings annually but lends the same amount as a personal loan at 12%, they earn ₹12,000. After accounting for operational costs and risks, the bank pockets a healthy profit.

This works because of the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) mandated by the Reserve Bank of India, which requires banks to maintain only a portion of deposits in reserve, allowing them to lend out the rest.

The Fee Goldmine: Death by a Thousand Cuts

Indian banks have become increasingly creative with fees and charges. While individually these seem small, collectively they generate massive revenue.

Common fees include minimum balance penalties (a major revenue source, as many account holders struggle to maintain the required balance), SMS and mobile banking charges, cheque book fees, NEFT/RTGS charges beyond free transactions, demand draft and pay order charges, ATM withdrawal fees after the free limit, and account closure charges. Many public sector banks also charge for services that private banks offer free, like passbook updates or annual debit card fees.

For many Indian banks, fee-based income now constitutes 15-25% of total revenue, a number that keeps growing each year.

Credit Cards: The Profit Powerhouse

Credit cards are extraordinarily lucrative for Indian banks. They earn through annual fees ranging from ₹500 for basic cards to ₹10,000+ for premium cards, interest on outstanding balances (typically 36-42% per annum, among the highest in the world), late payment fees, over-limit charges, and fuel surcharge recovery.

But there’s another significant revenue stream most people don’t know about: Merchant Discount Rate (MDR). Every time you swipe your card at a shop, the merchant pays the bank 1-3% of the transaction value. On a ₹10,000 purchase, the bank earns ₹100-300 just for processing the payment, though recent government regulations have changed MDR rules for certain transactions.

The Cross-Selling Strategy: One Customer, Multiple Products

Indian banks have become aggressive at selling multiple products to the same customer. Once you have a savings account, you’ll likely be offered a credit card, personal loan, insurance policy, mutual fund, fixed deposit, or demat account.

Each product generates revenue differently. Insurance products give banks significant commissions, sometimes 15-30% of the first year’s premium. Mutual fund distributors earn trail commissions annually. Loan processing fees add to the income. Banks prefer this approach because acquiring a new customer is expensive, so maximizing revenue from existing customers is more profitable.

Investment Income: Playing the Market

Indian banks don’t just lend your deposits; they also invest them. They purchase government securities (which also helps them meet SLR requirements), invest in corporate bonds, trade in the stock market through their treasury divisions, and deal in foreign exchange trading.

The profit from these investments, known as “treasury income,” can be substantial, especially for larger banks with sophisticated trading desks.

Digital Banking: Lower Costs, Higher Margins

The push toward digital banking isn’t just about convenience. For banks, it’s about dramatically reducing costs. A transaction at a bank branch costs ₹50-100 to process, while the same transaction on a mobile app costs less than ₹5.

This is why banks aggressively promote UPI, mobile banking apps, and net banking. Every customer who shifts to digital channels increases the bank’s profit margin. The rise of payment banks and neobanks has only accelerated this trend.

Priority Sector Lending: Profit with Purpose

RBI mandates that banks lend 40% of their credit to priority sectors like agriculture, MSMEs, education, and housing. While this is primarily a regulatory requirement, banks have found ways to make it profitable through Kisan Credit Cards with government interest subsidies, MSME loans at moderate rates but high volume, and education loans that build long-term customer relationships.

Some banks even buy Priority Sector Lending Certificates (PSLCs) from other banks to meet targets, creating another revenue stream.

The Changing Landscape

Indian banking is evolving rapidly. With UPI transactions crossing 10 billion per month, digital lending platforms growing exponentially, and fintechs disrupting traditional models, banks are constantly adapting their revenue strategies.

The next time your bank offers you a “free” account or an “exclusive” credit card, remember that in banking, nothing is truly free. Behind every service lies a carefully calculated business model designed to turn your money into their profit. Understanding this doesn’t make banks villains; it simply makes you a more informed customer who can make better financial decisions.

After all, banks aren’t charities. They’re businesses. And like any business, they’re very good at making money.