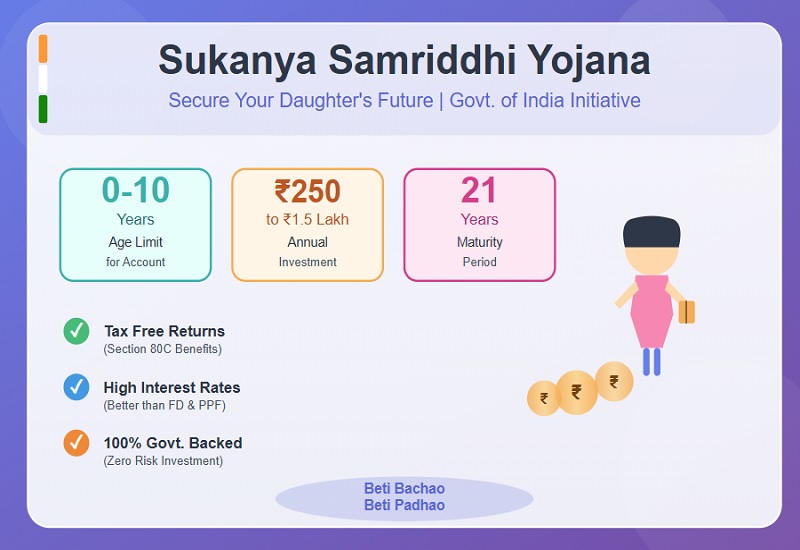

Create wealth for your daughter : Sukanya Samriddhi Yojana (SSY)

If you’re a parent of a young daughter in India, you’ve probably heard friends and family mention the Sukanya Samriddhi Yojana. But what exactly is it, and why are so many parents choosing this scheme over other investment options? Let me break it down for you in simple terms.

What is Sukanya Samriddhi Yojana?

Sukanya Samriddhi Yojana (SSY) is a government-backed savings scheme launched in 2015 as part of the Beti Bachao Beti Padhao campaign. Think of it as a special savings account designed exclusively for your daughter’s education and marriage expenses. The best part? It comes with attractive interest rates and significant tax benefits that you won’t find in regular savings accounts.

Who Can Open a Sukanya Samriddhi Account?

Here’s what you need to know about eligibility:

For Your Daughter:

- She must be below 10 years of age at the time of opening the account

- She must be an Indian citizen

- Only two accounts are allowed per family (one for each daughter)

Exception: If you have twins or triplets, you can open three accounts.

For Parents/Guardians:

- Any parent or legal guardian can open the account on behalf of the girl child

- You need to provide the birth certificate of your daughter

How Much Do You Need to Invest?

The investment limits are quite flexible:

- Minimum deposit: ₹250 per year (that’s less than ₹21 per month!)

- Maximum deposit: ₹1.5 lakh per financial year

- You can deposit in lump sum or in installments throughout the year

- Deposits required only for first 15 years

- Account continues to earn interest for 21 years

This flexibility means whether you want to save small amounts regularly or make larger annual deposits, the scheme accommodates your financial situation.

Interest Rates and Returns

The Sukanya Samriddhi Yojana interest rate is revised quarterly by the Government of India. As of the latest updates, the scheme offers one of the highest interest rates among all government-backed small savings schemes—significantly better than PPF, Fixed Deposits, or regular savings accounts.

As of January 1, 2024, Sukanya Samriddhi Yojana offers an attractive 8.2% annual interest rate. The rate is declared quarterly by the Government of India and comes with tax-free, compounded returns, helping parents build a secure and predictable financial corpus for their daughter.

Example:-

If you invest ₹1.5 lakh every year for 15 years:

- Total investment: ₹22.5 lakh

- Expected maturity value: ₹60–70 lakh (approx.)

- Actual returns depend on future interest rates, but the power of compounding works strongly in SSY’s favor.

Click to Calculate your return

Tax Benefits Under Sukanya Samriddhi Yojana

Here’s where SSY really shines. It falls under the EEE (Exempt-Exempt-Exempt) category:

Triple Tax Benefits:

- Tax deduction on investment: You can claim deductions up to ₹1.5 lakh under Section 80C of the Income Tax Act

- Tax-free interest: The interest earned is completely tax-free

- Tax-free maturity amount: The entire amount you receive at maturity is exempt from tax

This makes SSY one of the most tax-efficient investment options available for parents today.

When Can You Withdraw Money?

The account matures 21 years from the date of opening. However, the scheme understands that you might need funds for your daughter’s education or marriage:

Partial Withdrawal:

- Allowed after your daughter turns 18

- You can withdraw up to 50% of the balance for higher education expenses

- Requires proof of admission to an educational institution

Account Closure Before Maturity:

- After your daughter turns 18, the account can be closed for marriage purposes

- In case of the account holder’s unfortunate death, the account can be closed immediately

- Medical emergencies may also allow premature closure (with proper documentation)

How to Open a Sukanya Samriddhi Account

Opening an SSY account is straightforward:

Step 1: Visit Your Nearest Branch You can open the account at:

- Any Post Office branch across India

- Authorized branches of public and private sector banks

Step 2: Documents Required

- Birth certificate of your daughter (mandatory)

- Identity proof of parent/guardian (Aadhaar, PAN card, Passport, etc.)

- Address proof (Aadhaar, Passport, Utility bills, etc.)

- Recent passport-size photographs

Step 3: Fill the Application Form Complete the SSY account opening form available at the branch

Step 4: Make the Initial Deposit Deposit a minimum of ₹250 to activate the account

You’ll receive a passbook that tracks all your deposits and interest earned.

Key Features and Rules to Remember

Deposit Period: You need to make deposits for 15 years from the date of opening. After that, the account continues to earn interest until maturity (21 years) without requiring further deposits.

Default Account: If you fail to deposit the minimum ₹250 in any financial year, your account becomes inactive. You can revive it by paying ₹50 as a penalty along with the minimum deposit for each default year.

Transfer Facility: You can transfer your SSY account from one post office to another or from a post office to a bank (and vice versa) if you move to a different city.

Account Operation: Initially, the parent/guardian operates the account. Once your daughter turns 18, she can operate the account herself.

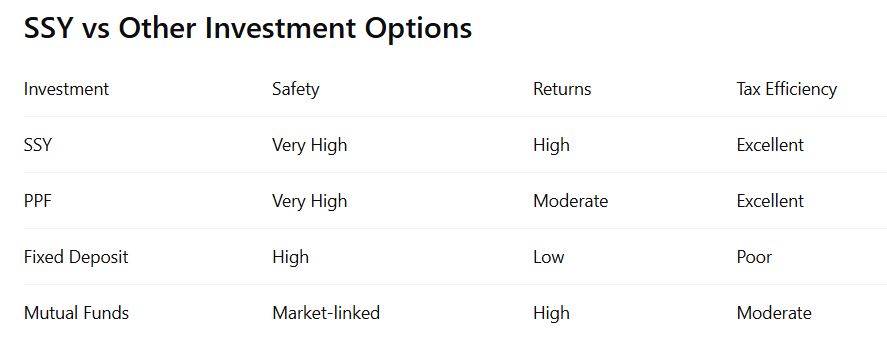

Sukanya Samriddhi Yojana vs Other Investment Options

When compared to other popular investment schemes:

Smart Tips for Maximizing Benefits

- Start Early: Open the account as soon as your daughter is born to maximize the compounding benefits over 21 years.

- Maximize Deposits: If possible, try to deposit the full ₹1.5 lakh annually to build a substantial corpus for your daughter’s future.

- Keep Records Safe: Maintain all receipts and the passbook carefully. You’ll need them for withdrawals and at maturity.

- Don’t Let It Default: Set reminders to ensure you deposit at least the minimum amount every year to keep the account active.

- Combine with Other Schemes: SSY works great alongside term insurance and health insurance for comprehensive financial planning for your family.

Common Questions Parents Ask

Can NRIs open an SSY account? No, only resident Indians can open and maintain Sukanya Samriddhi accounts. If your daughter becomes an NRI after opening the account, it needs to be closed.

What happens if I have more than two daughters? You can open accounts for only two daughters. However, in case of twins or triplets born after the first child, you may open a third account with proper documentation.

Can I open accounts in multiple post offices or banks? No, only one account per girl child is permitted across all branches and banks.

Why Sukanya Samriddhi Yojana Makes Sense

In today’s world, education costs are skyrocketing, and providing a secure financial future for daughters has never been more important. The Sukanya Samriddhi Yojana offers a perfect combination of safety, attractive returns, and tax benefits that few other investment options can match.

Whether you’re planning for your daughter’s engineering degree, medical education, or dream wedding, this scheme ensures you’ll have a substantial corpus ready when you need it most. The government backing provides complete safety, and the tax benefits mean more money stays in your pocket.

Final Thoughts

The Sukanya Samriddhi Yojana is more than just a savings scheme. It’s a commitment to your daughter’s dreams and aspirations. By starting early and staying consistent with your deposits, you’re not just building a financial corpus but also teaching your daughter the value of disciplined savings and financial planning.

If you haven’t opened an account yet and your daughter is under 10 years old, visit your nearest post office or bank branch today. The earlier you start, the more your money grows through the power of compounding. Your future self (and your daughter) will thank you for making this smart financial decision.

Remember, securing your daughter’s future doesn’t require enormous sacrifices. Even small, regular investments in Sukanya Samriddhi Yojana can create a significant difference over two decades. Start today, stay consistent, and watch your daughter’s dreams turn into reality.

If your goal is to secure your daughter’s future without taking market risk, Sukanya Samriddhi Yojana deserves a place in your financial plan.

It may not make headlines like stocks or crypto, but when it comes to safe, tax-free, long-term wealth creation, SSY quietly does its job—and does it well.

Disclaimer: Interest rates and scheme rules are subject to change by the Government of India. Please verify current rates and terms with your bank or post office before making investment decisions.