Direct vs Regular Mutual Funds: Which Should You Choose

If you’ve been exploring mutual fund investments lately, you’ve probably come across the terms “Direct” and “Regular” plans. I know it can be confusing at first—I mean, aren’t all mutual funds just… mutual funds? Well, not quite. The difference between these two might seem subtle, but it can significantly impact your returns over time.

Let me break this down for you in the simplest way possible, and by the end of this article, you’ll know exactly which one suits your investment style.

What Are Direct Mutual Funds?

Direct mutual funds are schemes that you purchase directly from the Asset Management Company (AMC) without involving any intermediary or distributor. Think of it like buying vegetables directly from the farm instead of going through a middleman.

When you invest in direct plans, you’re essentially cutting out the commission that would otherwise go to distributors or financial advisors. This means lower expense ratios and potentially higher returns for you.

Real Example of Direct Plans

Let’s say you want to invest in HDFC Top 100 Fund. You can go to the HDFC Mutual Fund website, complete your KYC, and invest directly. No broker, no advisor—just you and the AMC.

What Are Regular Mutual Funds?

Regular mutual funds are the same schemes but purchased through intermediaries like financial advisors, banks, or online platforms that charge a commission. These distributors help you select funds, manage paperwork, and provide ongoing support.

The AMC pays these intermediaries a commission, which is built into the expense ratio of the fund. This is why regular plans have higher expense ratios compared to direct plans.

Real Example of Regular Plans

If you walk into your bank and ask them to help you invest in mutual funds, or if you use a platform where a relationship manager assists you, you’re likely investing in regular plans.

The Core Difference: Expense Ratio

The main difference boils down to one thing: expense ratio.

The expense ratio is the annual fee charged by the fund house to manage your money. It’s expressed as a percentage of your investment.

Example:

- Direct Plan of Fund X: Expense Ratio = 0.80%

- Regular Plan of Fund X: Expense Ratio = 1.55%

That 0.75% difference might seem small, but over 20-30 years, it compounds into a massive amount.

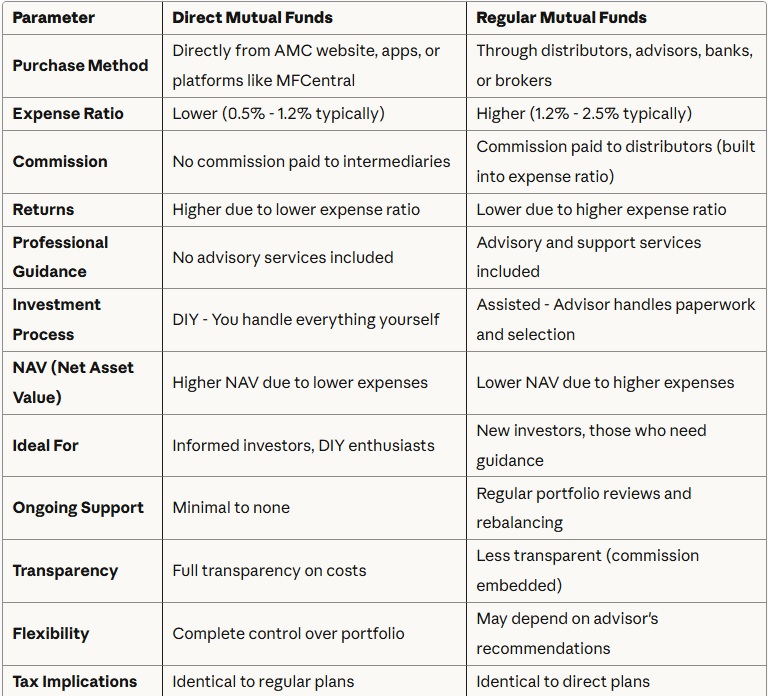

Direct vs Regular Mutual Funds: Detailed Comparison

Real-World Example: The Power of Compounding

Let me show you how this plays out with actual numbers.

Scenario:

- Initial Investment: ₹10,00,000 (₹10 lakh)

- Investment Period: 20 years

- Expected Annual Return: 12% (before expenses)

Direct Plan Calculation:

- Expense Ratio: 0.80%

- Net Return: 12% – 0.80% = 11.20%

- Final Corpus: ₹92,45,925

Regular Plan Calculation:

- Expense Ratio: 1.55%

- Net Return: 12% – 1.55% = 10.45%

- Final Corpus: ₹78,23,876

The Difference: ₹14,22,049

Yes, you read that right. Just by choosing the direct plan, you could potentially earn over ₹14 lakhs more on a ₹10 lakh investment over 20 years. That’s the power of compounding working in your favor!

Monthly SIP Example

Let’s look at a more relatable scenario with a monthly SIP:

Scenario:

- Monthly SIP: ₹10,000

- Investment Period: 25 years

- Expected Annual Return: 12%

Direct Plan:

- Net Return: 11.20%

- Final Corpus: ₹1,89,76,432

Regular Plan:

- Net Return: 10.45%

- Final Corpus: ₹1,61,83,256

The Difference: ₹27,93,176

By choosing direct plans for your SIP, you could accumulate nearly ₹28 lakhs more over 25 years!

When Should You Choose Direct Mutual Funds?

Direct plans are ideal if you:

- Have investment knowledge – You understand basic financial concepts and can research funds yourself

- Are comfortable with technology – You can navigate AMC websites and investment apps

- Want to maximize returns – Every percentage point matters to you

- Don’t need hand-holding – You’re confident making investment decisions independently

- Have time to monitor – You can track your portfolio and rebalance when needed

When Should You Choose Regular Mutual Funds?

Regular plans make sense if you:

- Are a complete beginner – You need someone to guide you through the process

- Value professional advice – You want expert recommendations on fund selection

- Lack time – You’d rather outsource portfolio management

- Need comprehensive planning – Your advisor provides holistic financial planning services

- Want ongoing support – You appreciate regular reviews and rebalancing assistance

How to Identify Direct vs Regular Plans

When you’re investing, here’s how to spot the difference:

- Fund Name: Direct plans typically have “Direct” or “Direct Plan” in the name

- Example: “HDFC Top 100 Fund – Direct Plan – Growth”

- Regular: “HDFC Top 100 Fund – Growth”

- NAV: Check the NAV on AMC websites—direct plans will have a higher NAV than regular plans for the same fund

- Expense Ratio: Always listed in the fund’s fact sheet—direct plans will show a lower percentage

My Honest Take: Which Is Better?

Look, I’ll be straight with you. If you’re reading investment blogs and researching this topic yourself, you’re probably capable of going the direct route. The cost savings are too significant to ignore.

However, there’s no shame in choosing regular plans if you genuinely benefit from advisory services. Good financial advisors do much more than just help you invest—they provide tax planning, retirement planning, insurance guidance, and emotional support during market crashes (which is invaluable!).

The key question is: Are you paying for value?

If your advisor is actively helping you with comprehensive financial planning and you’re comfortable with the cost, regular plans are fine. But if you’re simply paying commission for a one-time transaction with no ongoing support, you’re better off going direct.

Can You Switch from Regular to Direct (or Vice Versa)?

Yes, but there’s a catch. Switching from regular to direct plans (or vice versa) is treated as redemption and fresh purchase. This means:

- Exit load may apply if you switch before the exit load period ends (usually 1 year)

- Capital gains tax implications based on your holding period

- You’ll need to evaluate if the switch makes financial sense after considering these costs

Popular Platforms for Direct Mutual Funds

If you’ve decided to go direct, here are some reliable platforms:

- AMC Websites – Direct investment with each fund house

- MFCentral – Single platform to invest across multiple AMCs

Common Myths Debunked

1: “Direct plans are only for experienced investors”

- Reality: If you can use a smartphone, you can invest in direct plans. Most platforms are extremely user-friendly.

2: “Regular plans perform better”

- Reality: Both invest in the same portfolio. The only difference is expense ratio.

3: “You can’t get advice with direct plans”

- Reality: You can hire fee-only financial advisors who charge for advice separately and recommend direct plans.

The Bottom Line

Between direct and regular mutual funds, direct plans are mathematically superior for investors who can manage their own investments. The cost savings compound significantly over time, potentially adding lakhs to your retirement corpus.

However, if you’re truly benefiting from professional advisory services and comprehensive financial planning, the extra cost of regular plans might be justified. Just make sure you’re getting real value for the money you’re paying.

My suggestion? Start with direct plans for index funds and simple equity funds. As you gain confidence, you can expand your direct portfolio. And if you need advice on complex matters, consider hiring a fee-only financial advisor rather than going through commission-based distributors.

Remember, the best mutual fund plan is the one that gets you to invest consistently and stay invested for the long term. Whether direct or regular, what matters most is that you start investing today.

Disclaimer: This article is for educational purposes only and should not be considered financial advice. Please consult with a certified financial advisor before making investment decisions. Past performance does not guarantee future returns.

Comment if you want to know more.