How to Calculate Mutual Fund Returns: A real truth of CAGR and XIRR

Investing in mutual funds is one thing—knowing whether your investments are actually growing is another. I’ve spoken to countless investors who simply look at their portfolio value and assume they’re doing well, without truly understanding their actual returns.

If you’re investing through SIPs (Systematic Investment Plans) or making irregular investments, calculating your true returns isn’t as simple as checking how much your investment has grown. This is where XIRR comes in—and trust me, once you understand it, you’ll never look at your mutual fund returns the same way again.

Understanding Mutual Fund Returns: Why It’s Not Always Simple

Let me share something that surprises many investors: if you invest ₹10,000 today and it becomes ₹12,000 after one year, your return is 20%. Simple, right? But what if you invested ₹5,000 in January, another ₹3,000 in April, and ₹2,000 in September—and your portfolio is now worth ₹11,500? What’s your return now?

This is the reality for most mutual fund investors, especially those using SIPs. Your money enters the fund at different times, experiences different market conditions, and grows at different rates. Traditional return calculation methods fall short here.

Common Methods to Calculate Mutual Fund Returns

1. Absolute Return

This is the simplest method, showing the total percentage gain or loss on your investment.

Formula:

Absolute Return = [(Current Value - Investment Amount) / Investment Amount] × 100Example: You invested ₹1,00,000 and it grew to ₹1,30,000.

Absolute Return = [(1,30,000 - 1,00,000) / 1,00,000] × 100 = 30%Limitation: This method doesn’t consider the time period. A 30% return in one year is excellent, but the same 30% over five years is quite average. This is why absolute return works only for short-term, lump-sum investments.

2. Annualized Return (CAGR)

CAGR (Compound Annual Growth Rate) smooths out returns over multiple years, giving you an average annual return.

Formula:

CAGR = [(Ending Value / Beginning Value)^(1/Number of Years) - 1] × 100Example: You invested ₹1,00,000 which grew to ₹1,60,000 in 3 years.

CAGR = [(1,60,000 / 1,00,000)^(1/3) - 1] × 100

CAGR = [1.6^0.333 - 1] × 100 = 16.96%This means your investment grew at an average rate of approximately 17% per year.

Limitation: CAGR assumes a single lump-sum investment. It doesn’t work for SIPs or multiple investments made at different times. This is where XIRR becomes essential.

What is XIRR? The Game-Changer for SIP Investors

XIRR stands for Extended Internal Rate of Return. Think of it as CAGR’s more sophisticated cousin—one that can handle the messy reality of multiple cash flows at irregular intervals.

Here’s what makes XIRR special: it considers every single transaction you make (whether it’s an investment or redemption) along with the exact date of that transaction. This gives you the most accurate picture of your investment performance.

Why XIRR Matters

- Accurate Performance Tracking: If you’re investing ₹5,000 every month through SIP, each installment enters at a different market level. XIRR accounts for this timing difference.

- Real Returns, Not Illusions: I’ve seen investors excited about a ₹50,000 profit on a ₹5,00,000 investment, thinking they’ve made 10%. But if that money was invested over five years through SIP, their actual annualized return (XIRR) might be just 3-4%—barely beating inflation.

- Better Investment Decisions: When you know your actual returns, you can compare funds meaningfully and decide whether to continue, switch, or stop investing in a particular fund.

- Accounts for Cash Flow Timing: If you invested heavily during a market crash and bought units at lower NAVs, XIRR will reflect the benefit of your good timing.

How to Calculate XIRR: Step-by-Step Guide

Using Microsoft Excel or Google Sheets

XIRR is built into Excel and Google Sheets, making the calculation straightforward once you understand the structure.

Step 1: Organize Your Data

Create three columns:

- Column A: Date of transaction

- Column B: Cash flow (negative for investments, positive for redemptions/current value)

- Column C: Description (optional, for your reference)

Step 2: Enter Your Transactions

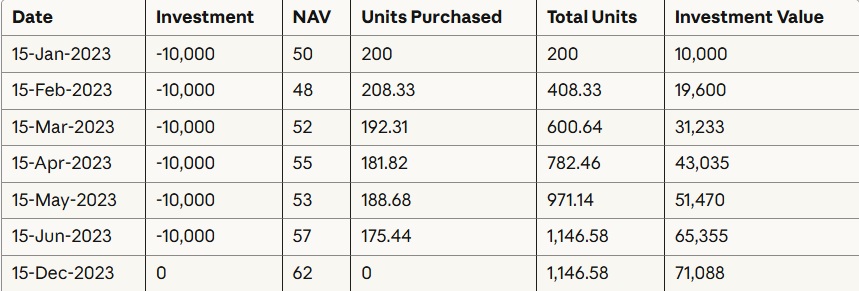

Example data:

Notice that investments are negative (money going out) and the current value is positive (money you’d receive if you redeem).

Step 3: Use the XIRR Formula

In a new cell, type:

=XIRR(B2:B8, A2:A8)Where B2:B8 is your cash flow range and A2:A8 is your date range.

Step 4: Format as Percentage

The result will be a decimal. Format the cell as percentage to get your XIRR. In this example, the XIRR would be approximately 18.89%, meaning your annualized return is nearly 19%.

Understanding the Result

An XIRR of 18.89% means that if your money had grown at a constant rate of 18.89% per year (compounded), you’d have the same ending value. It’s the equalizing rate that accounts for all your investments at different times.

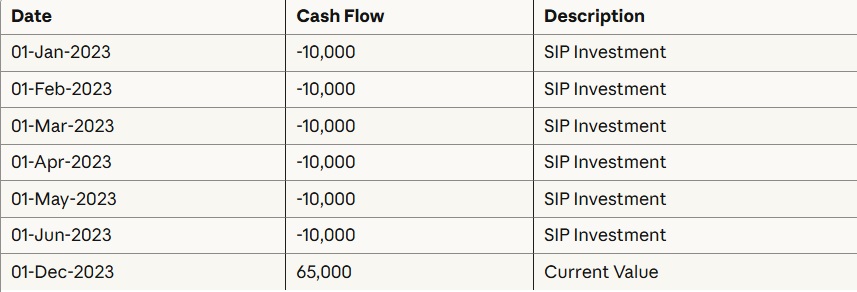

Real-World XIRR Example: SIP Investment

Let me walk you through a realistic scenario that mirrors what many investors experience.

Scenario: You started a monthly SIP of ₹10,000 in a large-cap mutual fund.

Your total investment: ₹60,000

Current value: ₹71,088

Absolute return: 18.48%

But what’s your annualized return? Using XIRR calculation:

=XIRR(B2:B8, A2:A8)

Result: 32.54%Your XIRR is 32.54%—significantly higher than the absolute return! Why? Because you invested gradually over the year, not all at once on day one. The later investments had less time to grow, which the XIRR calculation properly accounts for.

XIRR vs. CAGR: When to Use Each

Use CAGR when:

- You made a single lump-sum investment

- You want to compare fund performance over a specific period

- You’re looking at mutual fund factsheets (they typically show CAGR)

Use XIRR when:

- You’re investing through SIP

- You’ve made multiple investments at different times

- You’ve partially redeemed your investments

- You want to know YOUR actual returns (not just fund returns)

Here’s an important distinction many investors miss: The CAGR shown in fund factsheets shows how the fund performed. The XIRR shows how YOUR investment in that fund performed. These can be very different numbers.

Tips for Maximizing Your Mutual Fund Returns

1. Calculate XIRR Quarterly

Don’t wait until you redeem to check your returns. Calculate your XIRR every quarter to see if your funds are meeting your expectations. If a fund consistently underperforms its benchmark or category, it might be time to review your choice.

2. Compare Against Benchmarks

Your fund gave you 12% XIRR? Great! But if the benchmark index returned 15%, your fund actually underperformed. Always compare your XIRR against relevant benchmarks and category averages.

3. Account for Redemptions Properly

If you’ve partially redeemed your investment, include those transactions with positive values and their exact dates. This gives you a complete picture of your realized and unrealized returns.

4. Don’t Chase Past Returns

A fund showing 30% CAGR over the last three years doesn’t guarantee future performance. Use XIRR to track your own investment performance, and make decisions based on consistency, not just past glory.

5. Factor in Tax Implications

Your XIRR shows gross returns. Remember to account for capital gains tax when calculating your actual take-home returns. For equity funds, long-term gains above ₹1.25 lakh are taxed at 12.5%, while short-term gains are taxed at 20%.

Common XIRR Calculation Mistakes to Avoid

Mistake 1: Wrong Sign Convention

Remember: money going out (investments) should be negative, money coming in (redemptions, current value) should be positive. Reversing this will give you incorrect results.

Mistake 2: Not Using Consistent Dates

If you invested on the 15th of every month, don’t mix it with calculations ending on the 30th unless that’s your actual current value date. XIRR is sensitive to exact dates.

Mistake 3: Forgetting to Update Current Value

When calculating XIRR for ongoing investments, always use the latest NAV to determine your current portfolio value. An outdated value will give you outdated returns.

Mistake 4: Comparing XIRR Across Different Time Periods

An XIRR of 15% over ten years is more meaningful than an XIRR of 20% over six months. Returns stabilize over longer periods, so be cautious when comparing XIRRs of significantly different durations.

Using Online XIRR Calculators

If Excel isn’t your thing, several mutual fund platforms and financial websites offer XIRR calculators. Here’s what to look for:

Good calculators should:

- Allow multiple transaction entries

- Accept both investments and redemptions

- Calculate based on exact dates

- Show detailed breakup of your returns

- Popular options use Groww XIRR calculator

Most fund houses also show XIRR in their investor statements, though it’s always good to verify calculations yourself.

The Bottom Line: Know Your Real Returns

Understanding XIRR isn’t just about numbers—it’s about taking control of your financial future. When you know your actual returns, you can make informed decisions about where your hard-earned money should go.

I’ve seen too many investors either panic during market dips or become overconfident during bull runs, simply because they didn’t understand their true performance. XIRR gives you that clarity.

Start calculating your XIRR today. You might be pleasantly surprised to find your returns are better than you thought. Or you might discover that a fund you believed was performing well is actually lagging. Either way, you’ll have the knowledge to make better investment decisions.

Remember: in investing, knowledge isn’t just power—it’s profit.

FAQs About XIRR

Q: Is a higher XIRR always better?

Not necessarily. While higher returns are desirable, also consider the risk taken to achieve those returns. A 15% XIRR with lower volatility might be better than 20% XIRR with extreme ups and downs.

Q: How often should I calculate XIRR?

For actively managed portfolios, quarterly reviews are ideal. For long-term SIPs, annual calculations are sufficient unless you’re considering major changes.

Q: Can XIRR be negative?

Yes, if your current portfolio value is less than your total investments, your XIRR will be negative, indicating a loss.

Q: What’s a good XIRR for equity mutual funds?

Historically, equity funds have delivered 12-15% XIRR over long periods. Anything above 15% is considered excellent, though short-term XIRRs can be much higher or lower due to market volatility.

Q: Should I include dividends in XIRR calculation?

Yes, include dividend receipts as positive cash flows on the dates you received them for accurate XIRR calculation.

Have you calculated your mutual fund XIRR? What surprises did you discover about your returns? Share your experiences in the comments below!

One thought on “How to Calculate Mutual Fund Returns: A real truth of CAGR and XIRR”