Personal Loan vs Credit Card: Which one is better

Understanding Your Borrowing Options in India

Choosing between a personal loan and a credit card is one of the most important financial decisions you’ll make. Both are unsecured credit options offered by banks and NBFCs in India, but they work very differently. This comprehensive guide will help you understand which option suits your needs, whether you’re planning a wedding, consolidating debt, or managing everyday expenses.

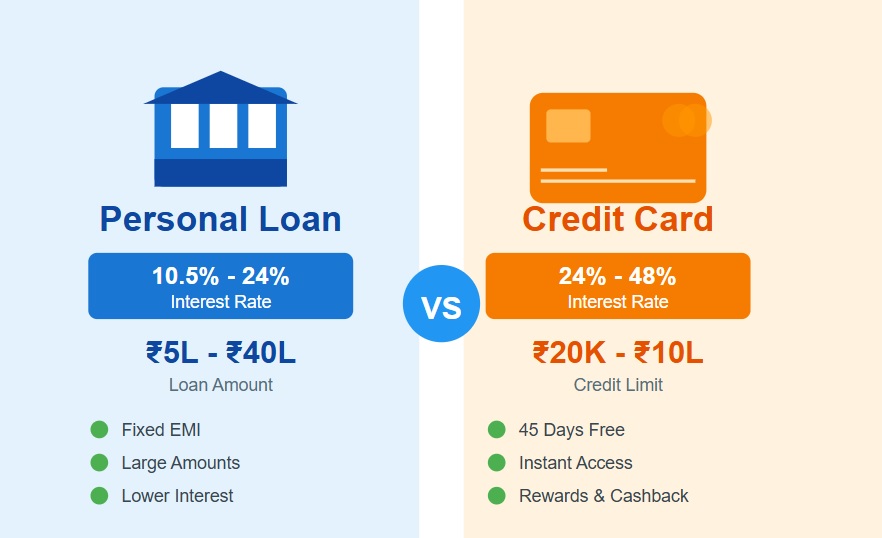

Quick Answer: Personal loans are better for large, one-time expenses with lower interest rates (10.5%-24% p.a.), while credit cards offer flexibility for smaller purchases with interest-free periods of 20-50 days but higher interest rates (24%-48% p.a.).

What is a Personal Loan?

A personal loan is a lump sum amount borrowed from a bank, NBFC, or digital lender that you repay in fixed Equated Monthly Installments (EMIs) over a predetermined tenure, typically ranging from 12 months to 60 months (1-5 years).

Key Features of Personal Loans in India:

- Loan Amount: ₹50,000 to ₹40 lakhs (varies by lender and eligibility)

- Interest Rate: 10.5% to 24% per annum (as of 2025)

- Tenure: 12 months to 60 months

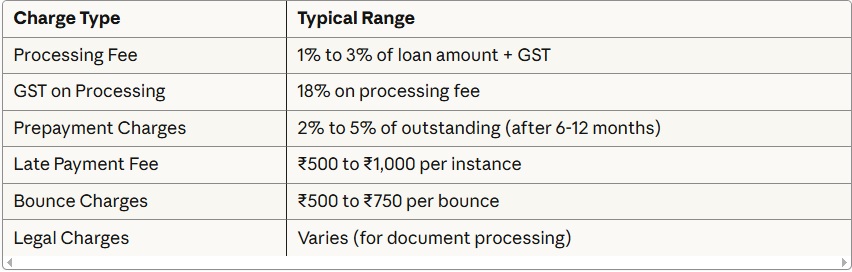

- Processing Fees: 1% to 3% of loan amount

- Prepayment Charges: 2% to 5% (foreclosure charges apply at some banks)

- Documentation: Minimal for salaried employees

What is a Credit Card?

A credit card is a revolving line of credit that allows you to borrow money repeatedly up to a pre-approved credit limit. You can make purchases, pay bills, and withdraw cash, then repay either in full or in parts.

Key Features of Credit Cards in India:

- Credit Limit: ₹20,000 to ₹10 lakhs+ (based on income and credit score)

- Interest Rate: 24% to 48% per annum (on unpaid balances)

- Interest-Free Period: 20-50 days (if full payment made)

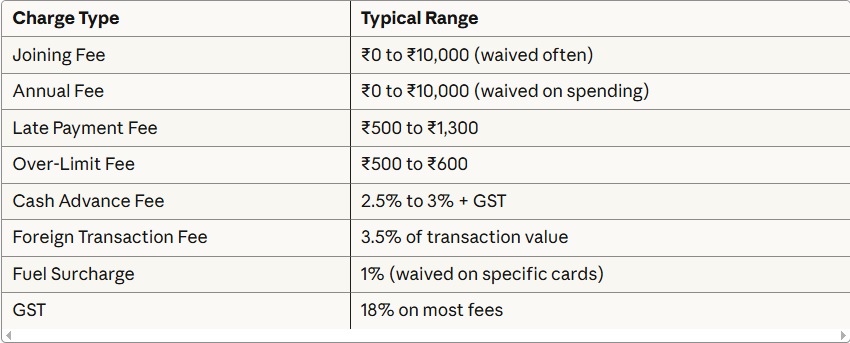

- Annual Fees: ₹0 to ₹10,000+ (premium cards)

- Late Payment Charges: ₹500 to ₹1,300 per instance

- Cash Withdrawal Charges: 2.5% to 3% + GST

Interest Rates: The Most Important Difference

This is where the two products show the biggest difference, and it directly impacts how much you’ll ultimately pay.

Personal Loan Interest Rates

Personal loan interest rates in India typically range from 10.5% to 24% per annum. The rate you receive depends on several factors:

- Credit Score: CIBIL score above 750 gets best rates (10.5%-15%)

- Income Level: Higher income = lower rates

- Employer Type: PSU/MNC employees get better rates than small company employees

- Existing Relationship: Pre-approved loans for existing customers at lower rates

- Loan Amount and Tenure: Larger amounts and longer tenures may have higher rates

Real Example: If you take a ₹5 lakh personal loan at 12% p.a. for 3 years:

- EMI: ₹16,607

- Total Interest Paid: ₹97,852

- Total Repayment: ₹5,97,852

Credit Card Interest Rates

Credit card interest rates in India are significantly higher, ranging from 24% to 48% per annum (2% to 4% per month) on unpaid balances.

However, credit cards offer a crucial advantage: the interest-free credit period of 20-50 days. If you pay your entire outstanding balance before the due date, you pay ZERO interest.

Real Example: Same ₹5 lakh on credit card at 36% p.a., paying ₹16,607 monthly:

- Time to Repay: 48 months (4 years)

- Total Interest Paid: ₹2,97,136

- Total Repayment: ₹7,97,136

The Difference: Using a credit card for the same expense costs ₹1,99,284 MORE in interest!

Winner: Personal Loan (for large expenses that can’t be repaid immediately)

EMI vs Minimum Payment: Repayment Structure Comparison

Personal Loan Repayment

Personal loans work on a fixed EMI structure calculated using the reducing balance method:

- Fixed EMI: Same amount every month (includes principal + interest)

- Reducing Balance: Interest calculated on outstanding principal

- Fixed Tenure: You know exactly when the loan ends

- No Flexibility: Must pay full EMI; missing payment affects credit score

Example EMI Calculation:

- Loan Amount: ₹3 lakhs

- Interest Rate: 14% p.a.

- Tenure: 2 years

- Monthly EMI: ₹14,374

Credit Card Repayment

Credit cards offer flexible repayment options:

- Full Payment: Pay entire outstanding, no interest charged

- Minimum Payment: 5% of outstanding or ₹200 (whichever higher)

- Partial Payment: Any amount between minimum and full

- Revolving Credit: Pay and borrow repeatedly

Example Minimum Payment Trap:

- Outstanding: ₹1 lakh

- Minimum Payment (5%): ₹5,000

- If you only pay minimum at 36% p.a., it takes 11+ years to clear the debt

- Total Interest Paid: ₹2,16,000+

Winner: Personal Loan (for discipline), Credit Card (for flexibility)

Processing Time and Approval: Speed Comparison

Personal Loan Processing Time

Traditional Banks:

- Application to Approval: 2-7 working days

- Documentation: Income proof, address proof, bank statements (3-6 months)

- Physical Verification: Sometimes required

- Disbursal: 1-3 days after approval

Digital Lenders:

- Application to Approval: 5 minutes to 24 hours

- Documentation: Minimal (Aadhaar, PAN, salary slips)

- Video KYC: Available

- Instant Disbursal: To bank account within hours

Pre-approved Personal Loans: Instant approval and disbursal for existing bank customers with good relationship.

Credit Card Processing Time

New Credit Card Application:

- Application to Approval: 7-21 days

- Documentation: Income proof, identity proof, address proof

- Physical Card Delivery: 7-10 days post-approval

- Activation: Immediate after receiving card

Instant Digital Cards: Some banks offer instant virtual cards that can be used immediately for online transactions.

Winner: Pre-approved personal loans and existing credit cards (instant access)

Usage and Flexibility: How They Differ

Personal Loan Usage

Advantages:

- Lump sum disbursement to your bank account

- Use for any purpose (no restrictions)

- Popular uses: Wedding expenses, medical emergencies, home renovation, debt consolidation, education

- Can transfer to anyone’s account

- No transaction limits

Limitations:

- One-time disbursal only

- Cannot re-borrow without new application

- Cannot access additional funds mid-tenure

- Must wait for closure before applying for new loan

Common Uses in India:

- Wedding expenses (₹5-15 lakhs)

- Medical emergencies (₹2-10 lakhs)

- Home renovation (₹3-8 lakhs)

- Debt consolidation (₹2-20 lakhs)

- Education abroad (₹10-30 lakhs)

Credit Card Usage

Advantages:

- Use anywhere cards accepted (online and offline)

- Revolving credit (pay and borrow repeatedly)

- Instant access for purchases

- EMI conversion available for large purchases

- Additional benefits: rewards, cashback, lounge access

Limitations:

- Limited to credit limit

- Not all merchants accept cards

- Cash withdrawal expensive (2.5%-3% charges)

- Can lead to overspending

- High interest on unpaid balances

Common Uses in India:

- Online shopping (Flipkart, Amazon)

- Utility bill payments

- Fuel purchases (with surcharge waiver)

- Travel bookings (flight, hotel)

- Dining and entertainment

- Emergency expenses

Winner: Credit Card (for flexibility and convenience)

Costs and Charges: Hidden Fees Comparison

Personal Loan Charges

Example:

- Loan Amount: ₹5 lakhs

- Processing Fee (2%): ₹10,000

- GST (18%): ₹1,800

- Total Upfront Cost: ₹11,800

Credit Card Charges

Hidden Charges to Watch:

- Minimum interest charge (₹100-₹500 even on small balances)

- Dynamic currency conversion fees (3-4%)

- Reward point redemption fees

- Duplicate statement charges (₹50-₹100)

Winner: Personal Loan (more transparent pricing for large amounts)

Eligibility Criteria: Who Can Apply?

Personal Loan Eligibility

Basic Requirements:

- Age: 21 to 60/65 years

- Income: Minimum ₹15,000 to ₹25,000 per month (salaried)

- Credit Score: 700+ (750+ for best rates)

- Employment: Minimum 6 months in current job, 2 years total experience

- Residence: Minimum 1 year at current address

Salaried Employees: Higher approval chances, lower rates Self-Employed: Higher rates, more documentation required

Top-Up Personal Loans: Existing customers with good repayment history can get instant top-ups at lower rates.

Credit Card Eligibility

Basic Requirements:

- Age: 18 to 65 years (add-on cards from 18)

- Income: Minimum ₹15,000 to ₹3 lakhs per month (varies by card)

- Credit Score: 750+ for premium cards

- Employment: Proof of regular income

- Address: Proof of residence

Income-Based Credit Limits:

- ₹15,000-₹25,000/month: ₹20,000-₹50,000 limit

- ₹50,000-₹1 lakh/month: ₹1-₹2 lakh limit

- ₹1 lakh-₹3 lakhs/month: ₹3-₹10 lakh+ limit

Special Categories:

- Students: Secured cards against FD

- Housewives: Add-on cards or cards based on family income

- Senior Citizens: Age relaxation up to 70 years

Winner: Credit Card (easier entry, wider accessibility)

Impact on Credit Score (CIBIL Score)

Both products significantly impact your CIBIL score, but in different ways.

Personal Loan Impact

Positive Impact:

- Timely EMI payments boost score (+50 to +100 points over time)

- Adds installment loan diversity to credit mix

- Shows responsible debt management

- Improves repayment history

Negative Impact:

- Multiple loan applications reduce score (-10 to -30 points per hard inquiry)

- Missing EMIs severely damages score (-50 to -100 points)

- High debt-to-income ratio raises red flags

- Defaults reported to CIBIL (remain for 7 years)

Credit Card Impact

Positive Impact:

- Regular usage and full payment builds strong credit history

- Long credit history improves score

- Low credit utilization (<30%) is ideal

- On-time minimum payments maintain score

Negative Impact:

- High credit utilization (>50%) lowers score

- Missing minimum payments drastically reduces score

- Multiple card applications hurt score

- Card closure reduces available credit

Credit Utilization Example:

- Credit Limit: ₹2 lakhs

- Ideal Usage: Below ₹60,000 (30%)

- Danger Zone: Above ₹1 lakh (50%)

Winner: Both can help or hurt depending on usage discipline

Credit Card Tax Benefits

No Direct Tax Benefits: Credit card spending and interest payments are NOT tax-deductible for personal use.

Exceptions:

- Business Expenses: If used for business, expenses can be claimed as business deductions

- Profession-Related: Doctors, lawyers, consultants can claim professional expenses

- GST Input Credit: Businesses can claim GST on card charges

Winner: Neither offers significant tax benefits for personal use

Real-Life Scenarios: Which One to Choose?

Scenario 1: Wedding Expenses (₹8 Lakhs)

Situation: Raj needs ₹8 lakhs for his wedding in 3 months.

Personal Loan Option:

- Amount: ₹8 lakhs

- Rate: 13% p.a.

- Tenure: 4 years

- EMI: ₹21,372

- Total Interest: ₹2,25,856

Credit Card Option:

- Split across 2-3 cards

- Rate: 36% p.a.

- If paying ₹21,372 monthly

- Time: 6+ years

- Total Interest: ₹6,00,000+

Best Choice: Personal Loan (saves ₹3.7+ lakhs in interest)

Scenario 2: Emergency Medical Expense (₹50,000)

Situation: Priya needs ₹50,000 for her father’s urgent medical procedure.

Personal Loan Option:

- Processing time: 2-7 days

- Processing fee: ₹1,000-₹1,500

- Interest: Starts immediately

Credit Card Option:

- Available immediately if card exists

- No processing fee

- 45-day interest-free period

- Can repay when insurance claim arrives

Best Choice: Credit Card (instant access, no interest if paid within 45 days)

Scenario 3: Debt Consolidation (₹5 Lakhs Credit Card Debt)

Situation: Amit has ₹5 lakhs spread across 4 credit cards at 36-42% interest.

Current Scenario:

- Total Outstanding: ₹5 lakhs

- Average Interest: 38% p.a.

- Minimum Payments: ₹25,000/month

- Time to Clear: 10+ years paying minimums

- Total Interest: ₹20+ lakhs

Personal Loan Consolidation:

- Amount: ₹5 lakhs

- Rate: 15% p.a.

- Tenure: 3 years

- EMI: ₹17,327

- Total Interest: ₹1,23,772

Savings: ₹18+ lakhs in interest, debt-free in 3 years instead of 10+

Best Choice: Personal Loan (massive savings)

Scenario 4: Online Shopping (₹30,000)

Situation: Sneha wants to buy a laptop for ₹30,000.

Personal Loan Option:

- Overkill for small amount

- High processing charges

- Locked into EMI tenure

Credit Card Option:

- Instant purchase

- Rewards/cashback (₹600-₹1,500)

- No-cost EMI options available

- 45-day interest-free period

Best Choice: Credit Card (convenience + rewards)

Scenario 5: Home Renovation (₹4 Lakhs)

Situation: Deepak needs to renovate his bathroom and kitchen.

Personal Loan Option:

- Amount: ₹4 lakhs

- Rate: 12% p.a.

- Tenure: 3 years

- EMI: ₹13,286

- Total Interest: ₹78,296

Credit Card Option (assuming ₹3 lakh limit):

- Interest: 36% p.a. on unpaid balance

- Flexible payment but expensive

- Total Interest: ₹1.5+ lakhs if not paid quickly

Best Choice: Personal Loan (structured repayment, lower interest)

Advantages and Disadvantages

Personal Loan Advantages

✅ Lower Interest Rates: 10.5%-24% vs 24%-48% for credit cards ✅ Fixed EMI: Predictable monthly payments ✅ Large Loan Amounts: Up to ₹40 lakhs available ✅ Fixed Tenure: Clear debt-free date ✅ Better for Big Expenses: Weddings, medical, education ✅ Lower Total Interest: Saves lakhs compared to credit cards ✅ No Temptation to Overspend: One-time disbursal

Personal Loan Disadvantages

❌ Processing Charges: 1%-3% + GST upfront ❌ No Flexibility: Fixed EMI must be paid ❌ Prepayment Charges: 2%-5% for foreclosure ❌ Processing Time: 2-7 days for approval ❌ Documentation Required: Income proof, bank statements ❌ Cannot Re-borrow: Need fresh application for more funds ❌ Credit Score Impact: Multiple applications hurt score

Credit Card Advantages

✅ Interest-Free Period: 20-50 days if paid in full ✅ Revolving Credit: Borrow repeatedly up to limit ✅ Instant Access: Use immediately for purchases ✅ Flexible Repayment: Choose payment amount ✅ Rewards and Benefits: Cashback, points, lounge access ✅ No Processing Fees: For regular usage ✅ Emergency Backup: Available 24/7 ✅ EMI Conversion: Large purchases can be converted

Credit Card Disadvantages

❌ Very High Interest: 24%-48% p.a. on unpaid balances ❌ Minimum Payment Trap: Takes years to clear debt ❌ Easy to Overspend: Psychological temptation ❌ Multiple Charges: Late fee, over-limit, cash advance ❌ Annual Fees: ₹500-₹10,000 per year ❌ Lower Limits: Typically ₹20,000-₹5 lakhs ❌ Credit Score Risk: High utilization hurts score

When to Choose Personal Loan

Choose a personal loan if you:

- Need a Large Amount: ₹2 lakhs to ₹40 lakhs for major expenses

- Have Planned Expenses: Wedding, home renovation, medical procedure

- Want Lower Interest: Save significantly on interest costs

- Need Structured Repayment: Prefer fixed EMIs and discipline

- Can Repay Over Time: 1-5 years repayment is acceptable

- Want Debt Consolidation: Combining multiple credit card debts

- Have Good Credit Score: Can get rates below 15%

- Don’t Need Repeated Access: One-time requirement

When to Choose Credit Card

Choose a credit card if you:

- Need Smaller Amounts: ₹5,000 to ₹2 lakhs typically

- Have Short-Term Needs: Can repay within 20-50 days

- Want Flexibility: Need revolving credit option

- Need Instant Access: Emergency or immediate purchase

- Can Pay in Full: Discipline to avoid interest charges

- Want Rewards: Cashback, points, travel benefits important

- Make Regular Purchases: Shopping, bills, dining, travel

- Build Credit History: Starting credit journey

Pro Tips for Smart Borrowing

Personal Loan Pro Tips

- Compare Multiple Lenders: Check at least 5 banks/NBFCs for best rates

- Check Pre-Approved Offers: Existing bank customers get instant approval at better rates

- Negotiate Rate: Ask for rate reduction based on credit score and relationship

- Choose Optimal Tenure: Shorter tenure = less interest but higher EMI

- Avoid Multiple Applications: Each application is a hard inquiry on CIBIL

- Read Fine Print: Check prepayment charges before signing

- Keep EMI Under 40%: Total EMIs shouldn’t exceed 40% of monthly income

- Document Purpose: Helps with tax benefits if applicable

Credit Card Pro Tips

- Always Pay Full Balance: Avoid interest by paying entire outstanding

- Set Up Auto-Pay: Never miss minimum payment date

- Keep Utilization Low: Use less than 30% of credit limit

- Convert to EMI Smartly: Large purchases can be converted to 0% EMI

- Track Spending: Use apps to monitor credit card expenses

- Don’t Withdraw Cash: Cash advance fees are expensive (2.5%-3%)

- Rotate Cards: Don’t let cards become inactive (use once in 3 months)

- Leverage Rewards: Choose cards matching spending pattern

Common Mistakes to Avoid

❌ Taking personal loan for small amounts under ₹50,000 ❌ Paying only minimum due on credit cards ❌ Taking personal loan to pay credit card bills without closing cards ❌ Applying for multiple loans/cards simultaneously ❌ Not reading terms and conditions thoroughly ❌ Exceeding credit limit on cards ❌ Missing EMI/payment due dates ❌ Not comparing interest rates across lenders ❌ Borrowing more than you can afford to repay

Conclusion: Making the Right Choice

Both personal loans and credit cards are valuable financial tools when used wisely. The key is understanding your specific need and choosing accordingly.

Choose Personal Loan for:

- Large one-time expenses (₹2 lakhs+)

- Lower interest rates (saves lakhs)

- Structured repayment discipline

- Debt consolidation from multiple credit cards

Choose Credit Card for:

- Everyday purchases and convenience

- Short-term needs (can repay in 20-50 days)

- Building credit history

- Emergency backup fund

- Earning rewards and benefits

The Golden Rule: Use credit cards like debit cards—spend only what you can pay back in full by the due date. Use personal loans only for necessary large expenses that genuinely require time to repay.

Remember, both products will appear on your CIBIL report. Responsible usage builds strong credit history, while misuse can damage your financial future for years.

Frequently Asked Questions (FAQs)

1. Can I pay off my credit card bill with a personal loan?

Yes, this is called debt consolidation. If you have high credit card debt at 36-42% interest, taking a personal loan at 12-18% can save you lakhs in interest. However, ensure you close or stop using those credit cards to avoid falling back into debt.

2. What is the minimum CIBIL score for personal loan and credit card?

For personal loans, 700+ is acceptable but 750+ gets best rates. For credit cards, 750+ is ideal for premium cards, though some banks issue basic cards at 650+ scores.

3. How much personal loan can I get on ₹50,000 salary?

Typically 10-15x your monthly salary. On ₹50,000 salary, you can get ₹5-7.5 lakhs personal loan depending on existing obligations, credit score, and lender policy.

4. Is personal loan better than credit card EMI?

Personal loans have lower interest (10.5-24%) compared to credit card EMI conversion (15-24%). However, some merchants offer 0% EMI on credit cards (cost borne by merchant), which is better than personal loans.

5. Can I get personal loan and credit card with same bank?

Yes, having existing relationship actually helps. Banks offer better rates and pre-approved limits to existing customers.

6. Which is easier to get approved – personal loan or credit card?

Credit cards are generally easier to get approved with lower income requirements. Personal loans require more documentation and have stricter eligibility criteria.

7. Do personal loans hurt credit score more than credit cards?

No, if managed properly. Both impact credit score similarly. Timely payments improve score for both. The key difference: high credit card utilization (>50%) hurts score more than personal loan EMI.

8. Can I convert my credit card outstanding to a personal loan?

Yes, many banks offer balance transfer facilities or personal loans specifically for credit card debt consolidation at lower interest rates (typically 14-18% vs 36-42% on cards).

9. What happens if I default on personal loan vs credit card?

Both are reported to CIBIL and severely damage credit score. Personal loan default may lead to legal action faster. Credit card default leads to mounting interest, collection calls, and eventual legal notice. Both remain on credit report for 7 years.

10. Which is better for medical emergency – personal loan or credit card?

Credit card is better for immediate emergencies (instant access, interest-free for 45 days). If treatment cost is very high or you need time to repay, convert to personal loan after initial treatment for lower interest rates.

Disclaimer: Interest rates, charges, and policies mentioned are indicative and based on market rates. Actual rates vary by lender, individual eligibility, and credit profile. Always read loan/credit card terms and conditions before applying. Consult a financial advisor for personalized advice.