50/30/20 Budget Rule: Guide to Money Management and Budgeting

What is the 50/30/20 Rule?

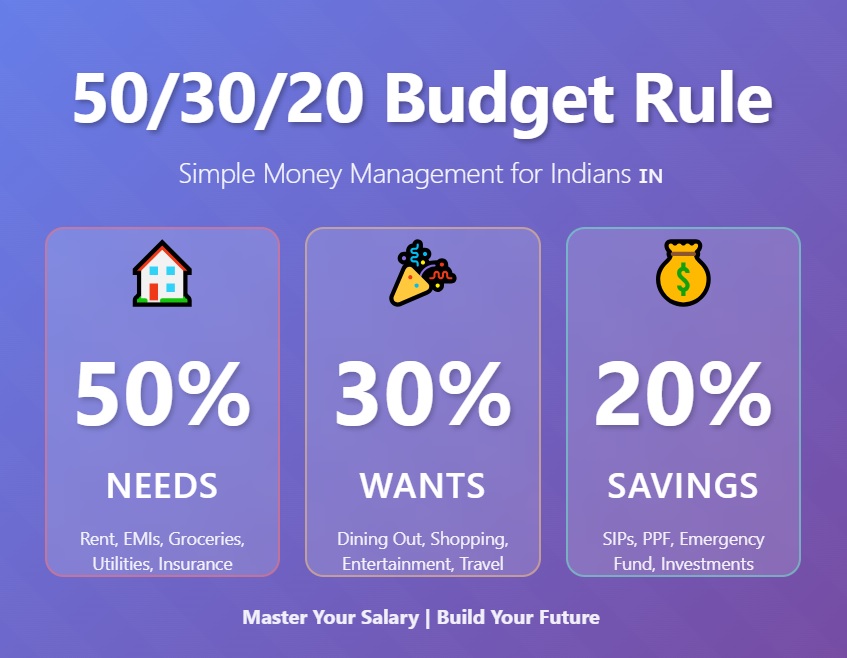

The 50/30/20 rule is a proven budgeting method that divides your take-home salary into three simple categories: 50% for needs, 30% for wants, and 20% for savings and investments. Created by Senator Elizabeth Warren, this budgeting strategy has helped millions worldwide take control of their finances, and it works perfectly for Indian households whether you’re earning ₹30,000 or ₹3 lakhs per month.

If you’re struggling to save money, living salary-to-salary, or simply want a straightforward approach to managing your finances without complex Excel sheets, the 50/30/20 budget could be the solution you’ve been looking for.

How Does the 50/30/20 Budget Work in India?

The Three Core Categories Explained

50% Needs: Your Essential Expenses

Needs are expenses you absolutely cannot avoid—the bills you must pay to maintain your basic standard of living. These include:

- Housing costs: Rent, home loan EMI, society maintenance charges, property tax

- Utilities: Electricity bill, water charges, cooking gas, WiFi/broadband

- Transportation: Petrol/diesel, auto/cab fares, metro/local train pass, bike/car EMI, vehicle insurance

- Groceries: Ration, vegetables, milk, and essential household items

- Insurance: Health insurance premiums, term life insurance

- Minimum debt payments: Minimum due on credit cards, personal loan EMIs, education loan EMIs

- Household help: Maid, cook, watchman (if necessary for dual-income households)

- Children’s education: School fees, tuition fees, uniform, books

The key word here is “essential.” If you could survive without it or find a cheaper alternative, it probably belongs in the wants category.

30% Wants: Your Lifestyle Choices

Wants are the extras that make life enjoyable but aren’t necessary for survival. This category includes:

- Dining out: Restaurants, Swiggy/Zomato orders, chai at cafes, weekend treats

- Entertainment: Netflix/Prime/Hotstar subscriptions, movie tickets, concerts, cricket matches

- Shopping: Fashion, electronics, home decor, gadgets

- Personal care: Salon visits, spa, parlour, premium grooming products

- Travel: Vacations, weekend getaways, trips to hometown beyond necessary visits

- Hobbies: Gym membership, sports equipment, art supplies, music classes

- Lifestyle upgrades: Premium mobile plans, latest smartphones, branded items

- Social expenses: Parties, gifts for weddings/birthdays, dining with friends

This 30% gives you the freedom to enjoy life while staying financially responsible. It’s about balance, not restriction.

20% Savings and Investments: Your Financial Future

This portion builds your financial security and freedom:

- Emergency fund: Aim for 6-12 months of expenses (kept in savings account or liquid funds)

- PPF (Public Provident Fund): Long-term tax-saving investment

- Mutual funds: SIPs in equity mutual funds for wealth creation

- Fixed deposits: Safe investment option for short to medium term

- EPF: Voluntary contributions beyond employer contribution

- NPS (National Pension System): Retirement planning with tax benefits

- Stocks: Direct equity investments if you understand the market

- Gold: Digital gold or Sovereign Gold Bonds

- Extra debt payments: Paying above minimum to eliminate high-interest debt faster

- Goal-based savings: Down payment for house, car fund, children’s education, marriage

This 20% is non-negotiable if you want to achieve long-term financial stability and financial independence.

Step-by-Step Guide: Implementing the 50/30/20 Budget in India

Step 1: Calculate Your In-Hand Salary

Start with your monthly take-home salary—the amount credited to your account after PF, TDS, professional tax, and other deductions. Don’t include reimbursements, bonuses, or variable pay initially.

Example: If your CTC is ₹12 lakhs annually but your monthly in-hand salary is ₹75,000, use ₹75,000 for budgeting:

- Needs: ₹37,500 (50%)

- Wants: ₹22,500 (30%)

- Savings/Investments: ₹15,000 (20%)

Step 2: Track Your Current Spending

Spend one month tracking every rupee to understand where your money actually goes. Check your bank statements, UPI transactions, credit card bills, and cash expenses. Use apps like Walnut, ET Money, or Money Manager, or simply maintain an Excel sheet.

Step 3: Compare Reality to Your Goals

Calculate what percentage of your income currently goes to each category. Many Indians find they’re spending 60-70% on needs and only 5-10% on savings. This gap shows exactly where adjustments are needed.

Step 4: Make Strategic Adjustments

If your percentages don’t match the 50/30/20 framework, consider these strategies:

Reduce needs below 50%:

- Shift to a more affordable rental area or get flatmates

- Use public transport instead of daily cab rides

- Cook at home more often, reduce outside food

- Switch to cheaper mobile/DTH plans

- Buy groceries in bulk from wholesale markets

- Negotiate lower rent with landlord

Trim wants from 30% to fund savings:

- Cancel unused OTT subscriptions (share with family instead)

- Set a monthly dining-out budget and stick to it

- Buy during sale seasons (Big Billion Day, Amazon Great Indian Festival)

- Use local trains/metros instead of Ola/Uber

- Find free entertainment (parks, beaches, community events)

- Wait 24 hours before making non-essential purchases

Boost savings to 20%:

- Set up automatic SIPs on salary day

- Open a PPF account and commit to annual contributions

- Increase EPF contribution percentage

- Direct festival bonuses and annual increments to investments

- Start with 10% if 20% seems impossible, then gradually increase

Step 5: Automate Your Budget

Set up automatic transfers and payments:

- SIPs on 1st or 5th of every month (after salary credit)

- Standing instructions for PPF, RD contributions

- Auto-pay for EMIs and insurance premiums

- Keep needs money in savings account

- Transfer wants money to separate account or UPI wallet

Real-World Examples of 50/30/20 Budget in India

Example 1: Young Professional in Bangalore (₹50,000/month in-hand)

Needs (50% = ₹25,000):

- Rent (PG/shared flat): ₹12,000

- Electricity, WiFi: ₹1,500

- Groceries and food: ₹4,000

- Metro pass and Ola/Uber: ₹3,000

- Mobile recharge: ₹500

- Health insurance: ₹2,000

- Credit card minimum payment: ₹2,000

Wants (30% = ₹15,000):

- Dining out and Swiggy: ₹5,000

- Shopping and clothes: ₹4,000

- Entertainment (OTT, movies): ₹1,000

- Gym membership: ₹2,000

- Social outings: ₹3,000

Savings/Investments (20% = ₹10,000):

- Equity mutual fund SIP: ₹5,000

- Emergency fund (liquid fund): ₹3,000

- PPF: ₹2,000

Example 2: Married Couple in Mumbai (₹1,50,000/month combined in-hand)

Needs (50% = ₹75,000):

- Rent (2BHK): ₹40,000

- Utilities and society charges: ₹5,000

- Groceries: ₹12,000

- Maid, cook: ₹5,000

- Petrol and vehicle maintenance: ₹4,000

- Car EMI: ₹15,000

- Insurance premiums: ₹4,000

Wants (30% = ₹45,000):

- Dining out: ₹10,000

- Shopping: ₹12,000

- Entertainment: ₹3,000

- Vacations (monthly average): ₹10,000

- Parents’ gifts and support: ₹5,000

- Personal care: ₹5,000

Savings/Investments (20% = ₹30,000):

- Equity mutual fund SIPs: ₹15,000

- PPF (both): ₹8,000

- Emergency fund: ₹5,000

- NPS: ₹2,000

Example 3: Middle-Class Family in Pune (₹80,000/month in-hand)

Needs (50% = ₹40,000):

- Home loan EMI: ₹18,000

- Utilities: ₹3,000

- Groceries: ₹8,000

- School fees (monthly average): ₹6,000

- Transportation: ₹3,000

- Insurance: ₹2,000

Wants (30% = ₹24,000):

- Dining out: ₹5,000

- Entertainment and outings: ₹4,000

- Shopping: ₹6,000

- Children’s activities: ₹4,000

- Miscellaneous: ₹5,000

Savings/Investments (20% = ₹16,000):

- Mutual fund SIPs: ₹8,000

- Children’s education fund: ₹4,000

- PPF: ₹2,000

- Emergency fund: ₹2,000

Common Challenges for Indians and Solutions

Challenge 1: “My Needs Exceed 50%”

This is extremely common in metros like Mumbai, Bangalore, and Delhi where rent alone can consume 40-50% of salary.

Solutions:

- Short-term: Adjust to 60/20/20 or 55/25/20 temporarily

- Reduce housing costs: Move to suburbs, get flatmates, negotiate rent

- Long-term: Work toward higher salary, consider smaller cities with lower living costs

- Side income: Start freelancing, tutoring, or small business to supplement income

Challenge 2: “Family Obligations Eat My Budget”

Indian families often have responsibilities toward parents, siblings’ education, or extended family support.

Solutions:

- Include regular family support in “needs” category (up to a limit)

- Set boundaries on non-emergency family requests

- Discuss financial responsibilities with siblings to share burden

- Plan for predictable expenses (festivals, weddings) in advance

Challenge 3: “EMIs Are Killing My Budget”

Many Indians have multiple EMIs—home loan, car loan, personal loans, credit card debt.

Solutions:

- Prioritize paying off high-interest debt (credit cards, personal loans) first

- Consolidate loans if possible for lower interest rates

- Avoid new EMIs until existing ones are manageable

- Make extra payments whenever you get bonuses

Challenge 4: “I’m Starting From Zero Savings”

Many Indians in their 20s and 30s have no emergency fund or investments.

Solutions:

- Start with even 5% savings, increase gradually

- Build ₹50,000-1 lakh emergency fund first before aggressive investing

- Take advantage of employer’s EPF matching

- Begin with one small SIP of ₹1,000-2,000 monthly

Challenge 5: “Festival Season Destroys My Budget”

Diwali, weddings, family functions can wreck months of careful budgeting.

Solutions:

- Create a separate “festival fund” within savings

- Save ₹2,000-5,000 monthly for annual festival expenses

- Set clear limits on gifts and celebration expenses

- Plan shopping during sales to maximize value

50/30/20 Budget vs Other Indian Budgeting Methods

50/30/20 vs Traditional Indian Saving (Save First, Spend Later)

Our parents’ generation believed in “save whatever is left.” The 50/30/20 flips this by allocating 20% to savings first, ensuring you save before spending. Both prioritize savings, but 50/30/20 provides clearer spending guidelines.

50/30/20 vs Zero-Based Budget

Zero-based budgeting tracks every rupee and assigns each one a purpose. It’s more detailed but requires more time. Choose 50/30/20 if you want simplicity; choose zero-based if you want maximum control over every expense.

50/30/20 vs Envelope/Jar Method

Popular in Indian households, this involves physically separating money into jars or envelopes. The 50/30/20 rule works similarly but can be implemented digitally using separate bank accounts or UPI wallets.

Advanced Tips for 50/30/20 Success in India

Optimize Your Needs Category

- Negotiate rent annually, switch localities if needed

- Use LED bulbs and energy-efficient appliances to reduce electricity bills

- Buy groceries from wholesale markets or mom-and-pop stores instead of supermarkets

- Use RO+UV water purifier instead of buying bottled water

- Compare and switch to cheaper insurance policies without compromising coverage

Maximize Your Wants Category

- Use credit cards with cashback for wants purchases (pay full amount monthly)

- Take advantage of bank offers on dining, shopping, travel

- Share OTT subscriptions with family/friends

- Use Paytm/PhonePe cashback for daily purchases

- Practice “no-spend weekends” monthly

Supercharge Your 20% Savings

- Max out Section 80C deductions (₹1.5 lakhs): EPF, PPF, ELSS, life insurance

- Invest in NPS for additional ₹50,000 deduction under 80CCD(1B)

- Start SIPs in diversified equity mutual funds for long-term wealth

- Use Sukanya Samriddhi Yojana for daughter’s future

- Consider sovereign gold bonds instead of physical gold

- Open high-interest savings accounts (up to 7% p.a.)

Tax Planning Within 50/30/20 Framework

Smart tax planning can effectively increase your savings:

Section 80C (₹1.5 lakh limit):

- EPF contributions

- PPF deposits

- ELSS mutual funds

- Life insurance premiums

- Home loan principal repayment

- Children’s tuition fees

Additional Deductions:

- 80D: Health insurance (₹25,000-₹50,000)

- 80CCD(1B): NPS (additional ₹50,000)

- 24B: Home loan interest (₹2 lakhs)

- 80E: Education loan interest (no limit)

Proper tax planning can save ₹50,000-1 lakh annually in taxes, effectively boosting your 20% savings category.

Frequently Asked Questions

Is the 50/30/20 rule realistic for Indian salaries?

Yes, though you may need adjustments. In metros with high living costs, you might start with 60/20/20 and work toward 50/30/20 as income grows or expenses reduce.

Should EPF be included in the 20%?

Mandatory EPF (12%) is deducted before calculating in-hand salary. Voluntary EPF contributions beyond this should go in the 20% savings category.

How do I handle annual expenses like insurance premiums?

Divide annual expenses by 12 and include the monthly amount in your needs category. Set aside money monthly so you’re prepared when the payment is due.

What about supporting parents financially?

Regular monthly support to parents should be included in your needs category (up to a reasonable limit). One-time emergency support comes from your emergency fund.

Should I save 20% while having high-interest debt?

Build a small emergency fund (₹25,000-50,000) first, then aggressively pay off high-interest debt before focusing on investments. Minimum debt payments go in needs; extra payments go in the 20% category.

What if I’m self-employed or have irregular income?

Base your budget on your minimum expected monthly income. In high-earning months, put extra toward savings. Build a larger emergency fund (12 months) for income stability.

How do I budget for weddings and festivals?

Create a “festival fund” by saving 5-10% monthly throughout the year. This comes from your savings category and prevents festival spending from derailing your budget.

Special Considerations for Different Life Stages

Fresh Graduates (₹25,000-40,000/month)

Focus: Emergency fund and learning to budget

- Keep needs low by sharing accommodation

- Invest minimally (₹2,000-5,000 monthly)

- Avoid lifestyle inflation as salary grows

Mid-Career Professionals (₹75,000-1.5 lakhs/month)

Focus: Aggressive wealth building

- Maximize equity mutual fund SIPs

- Build 6-month emergency fund

- Plan for major goals (house, car, marriage)

Married Couples with Kids (₹1-3 lakhs/month)

Focus: Goal-based planning and security

- Children’s education fund

- Adequate life and health insurance

- Home loan prepayment vs. investments balance

Pre-Retirement (50+ years)

Focus: Capital preservation and retirement corpus

- Shift from equity to debt gradually

- Maximize NPS contributions for tax benefits

- Clear all debts before retirement

Final Thoughts: Making the 50/30/20 Rule Work for You

The 50/30/20 budget rule isn’t about perfection—it’s about progress and financial discipline. It provides a simple, sustainable framework for managing money that works whether you’re earning ₹30,000 in Indore or ₹3 lakhs in Mumbai.

Remember, India has unique financial challenges: high living costs in metros, family obligations, festival expenses, and limited financial literacy. The 50/30/20 rule adapts to all these while giving you clear guidelines.

Start today by calculating your in-hand salary, tracking expenses for one month, and making gradual adjustments. The goal is financial freedom: having enough for your needs, room for your wants, and a growing foundation for your future.

With inflation rising, job security uncertain, and retirement dependent on your own planning (unlike pension days), having a solid budget is no longer optional—it’s essential.

Ready to take control of your finances? Calculate your monthly in-hand salary today and start your 50/30/20 budget journey. Your future self will thank you.

One thought on “50/30/20 Budget Rule: Guide to Money Management and Budgeting”