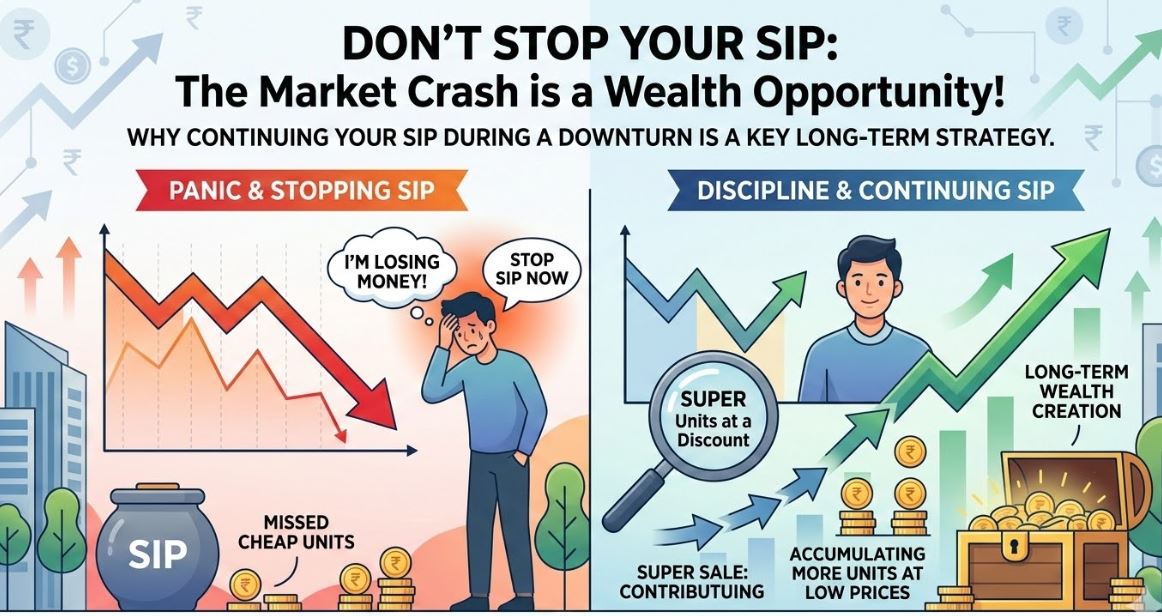

Why Stopping SIP in Market Crash is the blunder

Every time the market tumbles, I notice the same pattern.

Portfolios go red. Fear fills the news. And investors — thousands of them — quietly pause their Systematic Investment Plans (SIPs), telling themselves they’ll “restart when things settle down.”

It feels logical. It feels prudent. But it is, without question, one of the most financially damaging decisions a retail investor can make.

Let me explain why — with data, psychology, and a simple analogy that will change the way you think about market downturns forever.

The SIP Promise: What You Signed Up For

When you start a SIP, you commit to investing a fixed amount at regular intervals — regardless of market conditions. That last part is not fine print. It is the entire point.

SIPs are not just about automating savings. They are built on a powerful mathematical concept: Rupee Cost Averaging (RCA). Here’s how it works:

- When markets are HIGH, your fixed amount buys FEWER units.

- When markets are LOW, your fixed amount buys MORE units.

- Over time, this averages out your purchase cost — reducing risk and improving returns.

Stopping your SIP during a crash is like opting out of a sale at your favourite store. You’re skipping the months when every rupee works hardest for you.

The Psychology Behind the Panic

Humans are wired to avoid pain — and watching your portfolio drop 20–30% is painful. Our brains interpret this as a signal to flee.

This is called Loss Aversion, a concept made famous by behavioural economists Daniel Kahneman and Amos Tversky. Their research showed that the pain of losing ₹1,000 feels twice as intense as the pleasure of gaining ₹1,000.

This psychological bias causes investors to:

- Pause SIPs when markets fall (missing cheap accumulation)

- Redeem units at a loss to “stop the bleeding”

- Wait for “the right time” to re-enter — which never feels right

- Re-enter only after markets recover — buying expensive again

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett

Every time you let fear drive your SIP decisions, you hand that advantage to someone else.

What the Data Actually Shows

Let’s look at history. Every major market crash has eventually recovered — and rewarded those who stayed the course.

- 2008 Global Financial Crisis: Sensex fell ~60%. By 2010, it had fully recovered and gone higher.

- 2020 COVID Crash: Markets fell 38% in 6 weeks. By December 2020, Sensex hit new all-time highs.

- 2015–16 correction, 2018 IL&FS crisis, 2022 global selloff — same story every time.

Now consider two investors — Priya and Rahul — both investing ₹10,000/month via SIP in a large-cap fund.

During a crash, Priya panics and stops her SIP for 6 months. Rahul stays invested.

When the market recovers:

- Rahul accumulated more units at lower prices during those 6 months.

- His average cost is lower.

- His returns over 10 years are significantly higher — not because he was smarter, but because he was consistent.

Priya didn’t just lose 6 months of investment. She lost the compounding effect on those units — and the most valuable buying window of the cycle.

The Sale Analogy Nobody Talks About

Imagine you buy groceries from the same supermarket every month. One month, there’s a 30% sale across the board. Everything you normally buy is cheaper.

Would you stop shopping that month?

Of course not. You’d buy more.

A market crash is exactly that — a 30–40% sale on quality businesses, diversified funds, and productive assets. The only difference is that our emotions tell us the “sale” is a warning sign, not an opportunity.

Markets go on sale regularly. SIP investors who stay consistent are the ones filling their cart — while others are running out of the store.

The Compounding Multiplier You’re Throwing Away

Let’s talk about what’s truly at stake when you stop a SIP — even for just a few months.

Assume you invest ₹10,000/month at an average annual return of 12%.

- Over 20 years: Your wealth grows to approximately ₹96 lakhs.

- If you skip just 12 months during market dips: You potentially lose ₹8–12 lakhs in final corpus, depending on when the pause happens.

The earlier you stop — even briefly — the greater the compounding loss. The units you miss buying at low prices would have compounded for 10, 15, or 20 years.

Time in the market always beats timing the market.

But What If the Market Keeps Falling?

This is the fear everyone has. “What if this crash is different? What if it doesn’t recover?”

Here’s the honest answer: If equity markets permanently collapse and never recover, your SIP investments are the least of your worries. The entire financial system — savings accounts, real estate, gold — would be equally affected.

But in a diversified equity market — especially in a growing economy like India — this scenario is extremely unlikely over a long horizon.

India’s GDP is growing. Its middle class is expanding. Its corporate earnings, over time, trend upward. A SIP in a diversified fund is a bet on India’s long-term economic story — and that story has not changed because of a 6-month market correction.

What You Should Do Instead

If you’re worried during a market crash, here’s a more productive checklist:

- Keep your SIP running — non-negotiable.

- Review your asset allocation — not your SIP amount.

- Check your investment horizon — if it’s 10+ years, short-term volatility is noise.

- Consider a top-up SIP — buy more units while they’re cheap.

- Avoid checking your portfolio daily — it will trigger panic unnecessarily.

- Revisit your financial goals — your goals haven’t changed because the market dipped.

And if the volatility is genuinely too stressful, it may be worth consulting a financial advisor to review whether your fund selection aligns with your actual risk tolerance — not to stop investing, but to invest smarter.

The Investors Who Built Real Wealth

I’ve spoken with dozens of people who built meaningful wealth through mutual fund SIPs over 15–20 years. Not a single one built it by timing the market.

They built it by doing something remarkably simple:

They didn’t stop. Not in 2008. Not in 2011. Not in 2015. Not in 2020. They just didn’t stop.

The market rewarded their discipline — not their intelligence, not their timing, not their luck. Their discipline.

Final Thought

Market crashes are temporary. The wealth you fail to build because of fear is permanent.

Your SIP is not just a financial instrument. It is a commitment to your future self — a promise that you’ll stay the course even when it’s uncomfortable. The investors who honour that promise are the ones who look back 20 years later, amazed at what consistency quietly built for them.

Don’t stop the SIP. Especially not now.

Follow Nerdyfinance and Share this if you know someone who needs to hear it right now.

💬 Drop your thoughts below — have you ever paused a SIP and regretted it?

#PersonalFinance #SIP #MutualFunds #InvestingMindset #WealthCreation #FinancialPlanning #MarketCrash #LongTermInvesting #IndianInvestors #RupeeCostAveraging #nerdyfinance