Understanding Your Salary Slip: A Complete decode for Indian Employees

Remember the first time you received your salary slip? I do. I was fresh out of college, holding what looked like a complex financial document filled with abbreviations and numbers that seemed to dance around my “actual” salary. The excitement of my first paycheck quickly turned into confusion as I tried to decode terms like “Basic Pay,” “HRA,” “PF,” and those mysterious deductions that made my take-home salary significantly smaller than what I’d discussed during my job offer.

If you’ve ever felt the same way, you’re not alone. Millions of Indian employees receive their salary slips every month without fully understanding what they’re looking at. Today, let’s change that. Let’s break down every component of your salary slip so you can truly understand where your money comes from and where it goes.

What Exactly Is a Salary Slip?

A salary slip, also called a payslip or pay stub, is an official document issued by your employer that details your earnings and deductions for a specific month. Think of it as your monthly financial report card—it tells the story of your compensation, benefits, and contributions.

More importantly, it’s a legal document you’ll need for various purposes: applying for loans, renting apartments, visa applications, or even during job changes. Keep them safe, preferably both physical and digital copies.

The Anatomy of an Indian Salary Slip

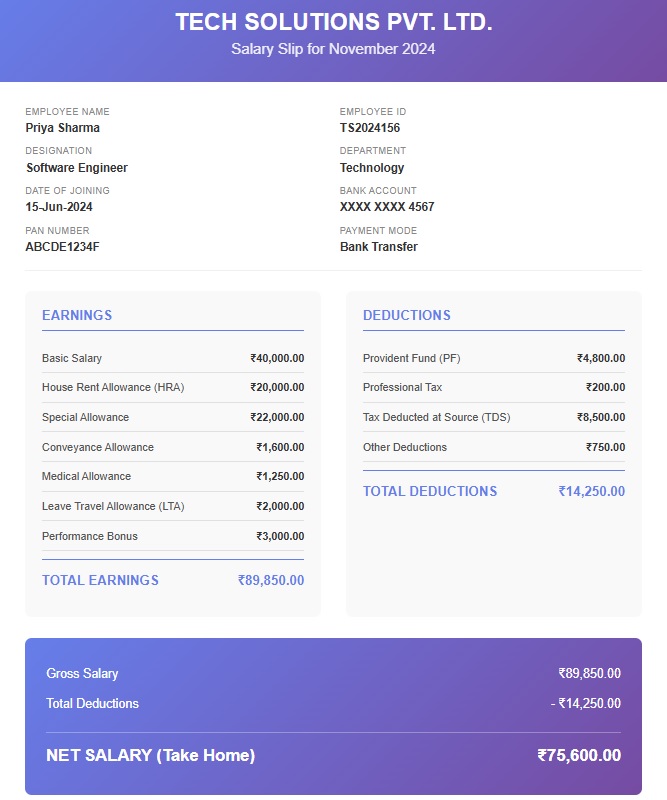

Let’s walk through a sample salary slip to understand each component. Meet Priya, a software engineer in Bangalore with a CTC (Cost to Company) of ₹12,00,000 per annum.

Sample Salary Slip

Company: Tech Solutions Pvt. Ltd.

Employee Name: Priya Sharma

Employee ID: TS2024156

Designation: Software Engineer

Month: November 2024

Bank Account: XXXX XXXX 4567

Earnings Breakdown

1. Basic Salary: ₹40,000

This is the foundation of your salary structure, typically 40-50% of your CTC. Basic salary is crucial because many other components are calculated as a percentage of this amount.

Why it matters: Your Provident Fund (PF), gratuity, and often your annual increments are based on your basic salary. A higher basic means better retirement savings and stronger financial security.

2. House Rent Allowance (HRA): ₹20,000

HRA is meant to help you cover your housing costs. The good news? If you’re living in rented accommodation, a portion of your HRA is tax-exempt.

Tax benefit calculation: You can claim the minimum of:

- Actual HRA received (₹20,000)

- Actual rent paid minus 10% of basic (Rent – ₹4,000)

- 50% of basic salary if you live in a metro city (₹20,000), or 40% for non-metro (₹16,000)

Priya’s scenario: She pays ₹18,000 as monthly rent in Bangalore. She can claim tax exemption on ₹14,000 (₹18,000 – ₹4,000), which is the minimum of the three calculations above.

3. Special Allowance: ₹22,000

This is a flexible component that employers use to balance the salary structure. It’s fully taxable but gives companies flexibility in structuring your compensation.

4. Conveyance Allowance: ₹1,600

Meant to cover your commuting expenses, up to ₹1,600 per month (₹19,200 annually) is tax-exempt without needing to submit bills.

5. Medical Allowance: ₹1,250

This covers medical expenses. While the allowance itself is taxable, you can claim reimbursement against actual medical bills up to ₹15,000 per year under the old tax regime.

6. Leave Travel Allowance (LTA): ₹2,000

LTA is designed to encourage you to travel within India with your family. It’s tax-exempt twice in a block of four years, but only against actual travel bills for you and your family.

7. Performance Bonus: ₹3,000

Some companies pay monthly bonuses or quarterly incentives. These are fully taxable but reflect your hard work and achievements.

Total Earnings: ₹89,850

Deductions: Where Does Your Money Go?

1. Provident Fund (PF): ₹4,800 (12% of Basic)

This is your retirement corpus. Both you and your employer contribute 12% of your basic salary. Your contribution is deducted from your salary, while your employer’s contribution is additional.

The real magic: Your employer’s 12% (₹4,800) doesn’t show on your salary slip as an earning, but it’s part of your CTC. This ₹4,800 + ₹4,800 = ₹9,600 goes into your PF account monthly, growing with interest (currently around 8.15% per annum).

Tax benefit: Your contribution is eligible for deduction under Section 80C (up to ₹1.5 lakh annually).

2. Employee State Insurance (ESI): ₹750 (if applicable)

If your gross salary is below ₹21,000 per month, ESI is mandatory. It’s a health insurance scheme where you contribute 0.75% and your employer contributes 3.25% of your wages. Since Priya earns more, this doesn’t apply to her.

3. Professional Tax: ₹200

This is a state-level tax that varies by state. In Karnataka, it’s ₹200 per month (₹2,400 annually). Maharashtra has different slabs. Some states don’t have professional tax at all.

Silver lining: Professional tax paid is deductible from your income tax under the old regime.

4. Tax Deducted at Source (TDS): ₹8,500

Based on your income, tax regime choice, and declarations, your employer deducts income tax monthly and deposits it with the government on your behalf.

How it’s calculated: Your employer considers your annual salary, investments under Section 80C, Section 80D, HRA exemption, and other deductions to arrive at your taxable income, then deducts tax accordingly.

Important: Keep track of TDS deducted throughout the year. You’ll need this information while filing your income tax return to claim refunds if excess tax was deducted.

Total Deductions: ₹14,250

The Final Number: Net Salary

Gross Salary: ₹89,850

Total Deductions: ₹14,250

Net Salary (Take-Home): ₹75,600

This is the amount that hits your bank account. This is your real, spendable money.

Understanding Your CTC vs Take-Home

Here’s where many people get confused during salary negotiations. Priya’s CTC is ₹12,00,000 per annum, but her monthly take-home is ₹75,600. Let’s break down the annual picture:

CTC Components:

- Your monthly earnings × 12: ₹89,850 × 12 = ₹10,78,200

- Employer’s PF contribution: ₹4,800 × 12 = ₹57,600

- Gratuity provision: ₹64,200 (approximately)

- Total CTC: ₹12,00,000

Annual Take-Home:

- ₹75,600 × 12 = ₹9,07,200

The difference of approximately ₹2,92,800 goes into:

- Your PF (retirement savings): ₹57,600

- Employer’s PF: ₹57,600

- TDS (tax to government): ₹1,02,000

- Professional Tax: ₹2,400

- Gratuity provision: ₹64,200

- Other statutory contributions

Common Salary Components You Might Encounter

Food Allowance/Meal Coupons

Some companies provide meal vouchers (like Sodexo) worth ₹2,200-2,600 per month, which are tax-exempt and can be used at restaurants and grocery stores.

Children Education Allowance

Up to ₹100 per month per child (maximum two children) is tax-exempt.

Uniform Allowance

Any amount spent on uniform maintenance can be claimed as exempt if your job requires a uniform.

Overtime Allowance

Payment for extra hours worked, fully taxable.

Variable Pay/Retention Bonus

Performance-linked payments, typically paid quarterly or annually.

Making Sense of Your Deductions

Why Such High Deductions?

It’s natural to feel a pinch when you see deductions eating into your gross salary. But here’s the perspective shift: these aren’t losses; they’re investments and obligations.

Your PF contribution is your future self thanking your present self. That ₹57,600 annually, compounding at 8%+, becomes a substantial corpus when you retire.

Your TDS means you’re contributing to nation-building—roads, schools, infrastructure. Plus, it’s not extra money lost; you would have had to pay this tax anyway when filing returns.

Professional tax funds state development projects.

Smart Tips for Maximizing Your Take-Home

1. Optimize Your Tax Declarations

Submit investment proofs under Section 80C (PPF, ELSS, life insurance), Section 80D (health insurance), and HRA receipts to reduce TDS.

2. Choose Your Tax Regime Wisely

The new tax regime offers lower rates but no deductions. The old regime has higher rates but allows deductions. Calculate which works better for you.

3. Negotiate Smartly

During salary negotiations, understand the structure. A higher basic salary (within limits) benefits your PF and gratuity. However, ensure adequate allowances for tax optimization.

4. Reimbursement Benefits

Utilize meal coupons, phone reimbursements, and internet allowances if your company offers them. These reduce your taxable income.

5. Keep Records

Maintain all rent receipts, medical bills, LTA travel tickets, and investment proofs. These are your tax-saving arsenal.

Red Flags to Watch For

While reviewing your salary slip, watch out for:

- PF contribution not deposited: Check your PF passbook regularly. Employers must deposit PF by the 15th of the following month.

- Incorrect TDS deduction: If you’ve submitted all declarations but TDS seems high, check with HR.

- Professional tax variation: Ensure it matches your state’s rules.

- Missing employer’s PF contribution: This should reflect in your PF account statement.

- Salary credited but no salary slip: Always insist on a salary slip. It’s your legal right.

Beyond the Numbers: Why Your Salary Slip Matters

Your salary slip is more than a monthly financial statement. It’s:

- Proof of employment and income for loans, visas, and rentals

- A record of your tax payments for filing returns

- Evidence for claiming social security benefits like PF, gratuity, and pension

- Documentation for insurance claims and financial planning

- Legal protection in case of employment disputes

Final Thoughts

Understanding your salary slip empowers you to make better financial decisions. It helps you during tax planning, loan applications, job switches, and retirement planning.

Don’t be that person who receives their salary slip, glances at the net pay, and files it away. Be curious. Ask questions. Understand where your hard-earned money goes and how it’s working for you.

The next time you receive your salary slip, you won’t just see numbers and abbreviations. You’ll see a comprehensive picture of your financial relationship with your employer, the government, and your future self.

After all, financial literacy begins with understanding what you earn, what you keep, and what you’re building for tomorrow.

Have questions about specific components of your salary slip? Your HR department is there to help. Don’t hesitate to ask for clarification—it’s your money, and you have every right to understand it completely.