What will happen RBI prints more money ?

Central banks wield enormous power through their ability to create money, a tool that can either stabilize economies or unleash devastating consequences. Understanding what happens when this power is used excessively requires examining the mechanisms, benefits, risks, and regulatory frameworks that govern monetary policy worldwide. Let’s understand What will happen when RBI prints more money ?

Understanding Money Creation

Central banks don’t literally “print” most money in modern economies. Instead, they create money electronically through processes like purchasing government bonds or lending to commercial banks. When a central bank buys assets, it credits the seller’s account with newly created money, expanding the monetary base. This process, known as quantitative easing in its modern form, has become increasingly common since the 2008 financial crisis.

The Potential Benefits of Monetary Expansion

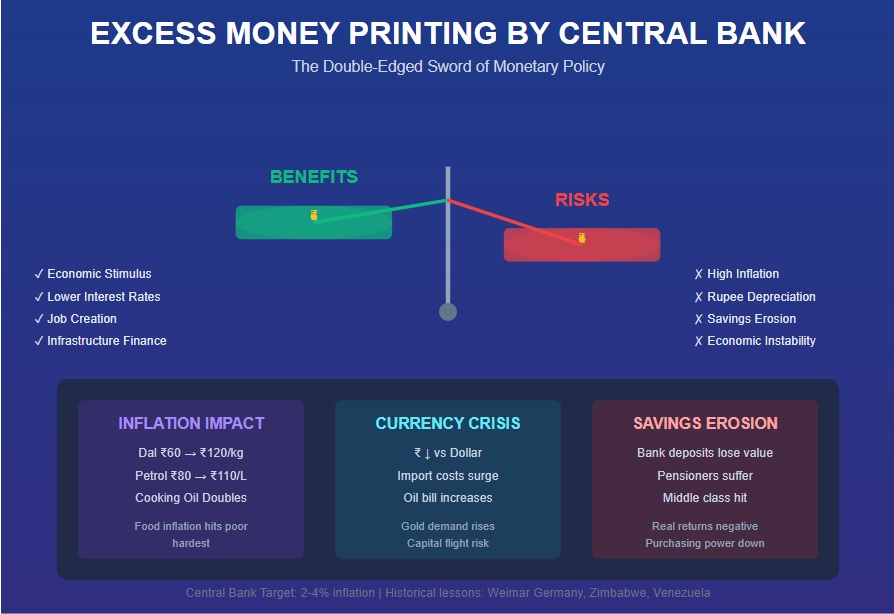

When deployed strategically, increasing the money supply can serve legitimate economic purposes. During recessions, additional money can stimulate spending and investment when private sector demand collapses. Lower interest rates resulting from monetary expansion make borrowing cheaper for businesses and consumers, potentially jumpstarting economic activity. Central banks used this approach aggressively during the 2008 crisis and the COVID-19 pandemic, preventing what could have been far worse economic contractions.

Moderate inflation, often a result of careful monetary expansion, can actually benefit economies by encouraging spending rather than hoarding cash, reducing the real burden of debt, and providing central banks with room to cut interest rates during downturns. Many economists consider 2-3% annual inflation optimal for healthy economic growth.

The Dangers of Excessive Money Printing

The risks of printing too much money, however, can be catastrophic. The most obvious danger is inflation, which erodes purchasing power and can spiral out of control if expectations shift. When people expect prices to rise, they spend money quickly before it loses value, creating a self-fulfilling cycle. In extreme cases, this becomes hyperinflation.

History provides stark warnings. Weimar Germany in the early 1920s printed money to pay war reparations, leading to hyperinflation where prices doubled every few days. People carried money in wheelbarrows to buy bread. Zimbabwe in the late 2000s printed money to finance government spending, resulting in inflation rates reaching billions of percent annually, eventually forcing the country to abandon its currency entirely. More recently, Venezuela printed money to cover budget deficits, leading to hyperinflation, economic collapse, and mass emigration.

Beyond inflation, excessive money printing creates other problems. It distorts price signals that guide economic decision-making, leading to misallocation of resources. Asset bubbles can form as excess money flows into stocks, real estate, or other investments. Currency devaluation makes imports more expensive and can trigger capital flight as people move wealth to more stable currencies. Income inequality often worsens as those with assets benefit from rising prices while wage earners see their purchasing power decline.

The Mechanisms of Harm

When central banks create too much money relative to economic output, the consequences unfold through several channels. Domestic prices rise as more money chases the same goods and services. International exchange rates fall as foreign investors lose confidence, making imports more expensive and potentially triggering inflation in imported goods. Creditors suffer as the real value of loans decreases, while debtors benefit, creating unfair wealth transfers. Perhaps most insidiously, once inflation expectations become entrenched, they’re extremely difficult to reverse without painful economic contractions.

Regulatory Frameworks and Safeguards

Recognizing these dangers, most developed countries have established robust frameworks to prevent excessive money creation. Central bank independence stands as the primary safeguard, with institutions like the Federal Reserve, Reserve Bank of India, European Central Bank, and Bank of England operating free from direct political control. Politicians facing elections often favor short-term stimulus over long-term stability, making independence crucial.

Explicit inflation targeting provides another check, with most major central banks mandating they keep inflation around 2% annually. This creates accountability and anchors public expectations. Many countries also prohibit or strictly limit monetary financing, where central banks directly fund government spending by creating money. The European Union’s Maastricht Treaty explicitly bans this practice, forcing governments to borrow from markets rather than printing money.

Transparency requirements compel central banks to publish detailed reports, meeting minutes, and economic projections, allowing public scrutiny of their decisions. Dual mandates, like the Federal Reserve’s requirement to pursue both price stability and maximum employment, prevent single-minded focus that might miss broader economic impacts. International coordination through institutions like the Bank for International Settlements helps prevent competitive devaluations and promotes sound monetary practices globally.

The Modern Challenge: Quantitative Easing

Since 2008, central banks in developed economies have engaged in unprecedented monetary expansion through quantitative easing, purchasing trillions in government bonds and other assets. This raises important questions about whether traditional concerns about money printing still apply.

Proponents argue that when economies are in deep recession with low inflation, additional money simply fills a gap left by reduced private spending rather than causing inflation. The experience of Japan, the United States, and Europe seemed to support this view, as massive monetary expansion didn’t trigger the inflation many predicted. However, the inflation surge of 2021-2023 following pandemic-era monetary and fiscal expansion has renewed concerns that central banks pushed too far.

Critics warn that even if inflation remains contained initially, excessive money creation can fuel asset bubbles, create zombie companies dependent on cheap credit, reduce central bank effectiveness when future crises hit, and ultimately undermine confidence in fiat currencies. The line between appropriate crisis response and excessive money printing remains hotly debated among economists.

Balancing Act: Finding the Right Amount

The fundamental challenge facing central banks is determining how much money creation is appropriate. Too little, and economies may suffer unnecessary unemployment and stagnation. Too much, and inflation erodes prosperity and trust in the monetary system. This balance depends on numerous factors including economic growth rates, unemployment levels, inflation expectations, global economic conditions, and financial system stability.

Central banks rely on sophisticated economic models, vast datasets, and expert judgment to navigate these tradeoffs. Even with these tools, they sometimes make mistakes, responding too slowly to emerging problems or overcorrecting in ways that create new issues. The lag between policy changes and their economic effects, often 12-18 months, makes real-time adjustment extraordinarily difficult.

Lessons from History

Examining monetary disasters reveals common patterns. Excessive money printing typically occurs when governments face fiscal crises they can’t resolve through taxation or borrowing, during wars requiring massive spending, under political pressure to boost short-term growth, or when weak institutions fail to maintain discipline. The consequences invariably include economic hardship, loss of savings, social unrest, and sometimes political upheaval.

Successful monetary management requires political will to maintain institutional independence, public understanding of the importance of price stability, credible commitment to long-term thinking over short-term gains, and learning from both successes and failures. Countries that maintain these principles generally avoid the worst outcomes of monetary excess.

The Future of Money Creation

As economies evolve, so do the challenges of monetary policy. Digital currencies, both private cryptocurrencies and central bank digital currencies, may fundamentally alter how money creation works. Some argue cryptocurrencies with fixed supplies could constrain central bank power, while others worry that digital central bank currencies could enable even more aggressive monetary expansion. Climate change, demographic shifts, and technological disruption will all influence how much monetary expansion economies can sustain without inflation.

The pandemic experience, where massive monetary and fiscal expansion initially seemed consequence-free before inflation surged, suggests that the relationship between money creation and inflation may be more complex and delayed than traditional models suggest. Central banks are reassessing their frameworks in light of this experience.

Conclusion

The power to create money is both essential and dangerous. Used wisely, it allows central banks to smooth economic cycles, support employment, and prevent financial catastrophes. Used recklessly, it destroys savings, impoverishes citizens, and can collapse entire economies. The difference lies not just in the amount of money created, but in the institutional frameworks, regulatory safeguards, and commitment to long-term stability that guide monetary policy.

History demonstrates that while moderate money creation serves legitimate purposes, excess invariably leads to economic pain. The regulations and independence mechanisms developed over decades exist precisely because the temptation to print money is so strong and the consequences of doing so excessively are so severe. As economies face new challenges in coming years, maintaining the delicate balance between monetary expansion and stability will remain one of the most critical tasks facing policymakers worldwide.

The lesson is clear: central banks can and should create money to serve economic needs, but only within carefully constructed limits enforced by strong institutions, transparent processes, and unwavering commitment to price stability. When these guardrails fail, the results are predictable and devastating.