You will never get run out of money. Choose SWP

Planning for retirement or looking for a steady income stream from your investments? A Systematic Withdrawal Plan might be exactly what you need. Let me walk you through everything about SWP in simple terms, with real examples that’ll help you decide if it’s right for you.

What is a Systematic Withdrawal Plan (SWP)?

Think of SWP as the opposite of a SIP (Systematic Investment Plan). While SIP helps you invest regularly, SWP lets you withdraw money regularly from your mutual fund investments. It’s like setting up a monthly salary for yourself from your own investment corpus.

You decide how much you want to withdraw and how often, and the mutual fund automatically transfers that amount to your bank account. Simple, systematic, and stress-free.

How Does SWP Work? A Real-Life Example

Let me share Priya’s story to make this crystal clear.

Priya’s Situation:

- Age: 58 years, recently retired

- Mutual fund investment: ₹50,00,000 in an equity mutual fund

- Monthly expense need: ₹25,000

- Expected fund return: 12% annually

What Priya Did:

She set up an SWP to withdraw ₹25,000 every month. Here’s what happens:

- On the 5th of every month, ₹25,000 gets automatically transferred to her bank account

- The fund house redeems the required number of units to generate this amount

- Her remaining investment continues to grow

The Math After One Year:

- Total withdrawals: ₹25,000 × 12 = ₹3,00,000

- Investment value growth: ₹50,00,000 × 12% = ₹6,00,000

- Net corpus value: ₹50,00,000 – ₹3,00,000 + ₹6,00,000 = ₹53,00,000

Even after withdrawing ₹3 lakh for her expenses, Priya’s corpus grew by ₹3 lakh because her returns exceeded her withdrawals. That’s the beauty of SWP when done right.

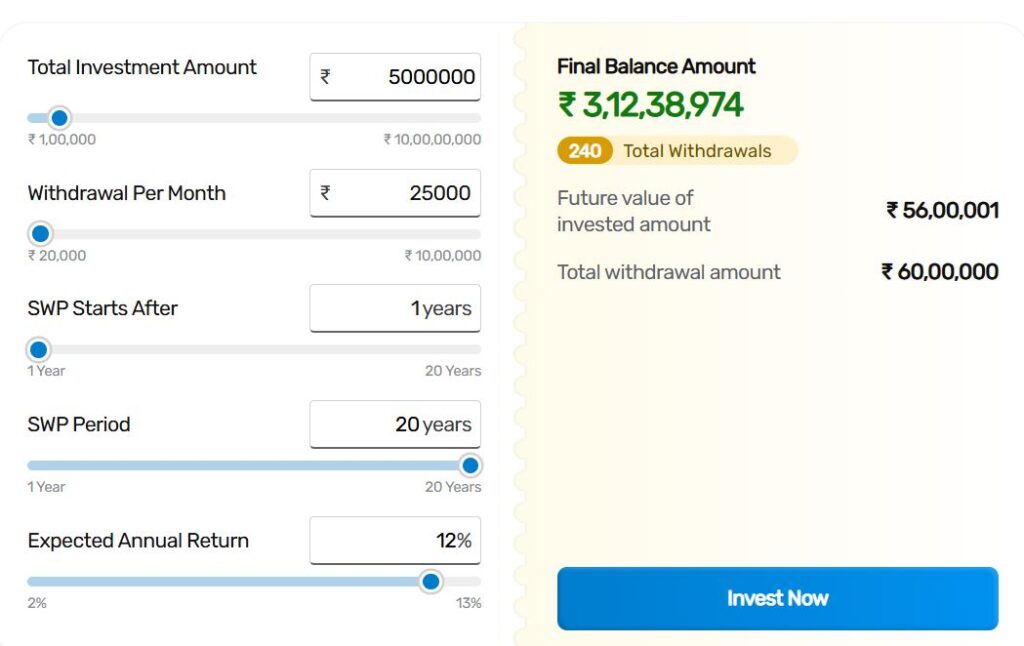

In this scenario the money will grow rapidly after withdrawal also. See the real picture below

Types of Systematic Withdrawal Plans

1. Fixed Withdrawal SWP

You withdraw the same amount every month. This is what Priya used—₹25,000 every month, no matter what.

Best for: People who need predictable monthly income, like retirees.

2. Appreciation Withdrawal SWP

You only withdraw the profits or gains, keeping your principal amount intact.

Example: If Rajesh invested ₹20 lakh and it grew to ₹23 lakh, he could withdraw ₹3 lakh (only the appreciation) while keeping his original ₹20 lakh invested.

Best for: Long-term wealth preservation while enjoying returns.

3. Custom Withdrawal SWP

You set different amounts for different months based on your needs.

Example: Anita withdraws ₹30,000 during her children’s school months (April-March) but only ₹15,000 during vacation months.

Best for: People with varying monthly expenses.

Tax Benefits of SWP (This is Important!)

Here’s where SWP really shines compared to traditional options like Fixed Deposits.

Tax on Equity Mutual Funds:

- Short-term capital gains (sold within 1 year): 20% tax

- Long-term capital gains (held over 1 year): 12.5% tax on gains above ₹1.25 lakh per year

Tax on Debt Mutual Funds:

- Gains taxed according to your income tax slab

Who Should Use SWP?

SWP works beautifully for:

- Retirees seeking regular monthly income

- Parents funding their children’s education with staggered withdrawals

- Investors wanting to shift from equity to debt gradually

- Anyone needing regular cash flow while keeping investments growing

Real Example: Planning Your Child’s Education with SWP

Meet Vikram, who invested ₹30 lakh when his daughter was 15. She’d need money for college at 18.

His SWP Strategy:

- Year 1 (Age 16): No withdrawal, let it grow

- Year 2 (Age 17): No withdrawal

- Year 3 (Age 18): Withdraw ₹3 lakh for admission

- Years 4-6 (Age 18-21): Withdraw ₹2.5 lakh annually for fees

By setting up scheduled SWPs, Vikram ensured money was available exactly when needed, while the remaining corpus continued earning returns.

How to Set Up an SWP: Step-by-Step

- Choose your mutual fund (preferably one you’ve held for over a year)

- Decide withdrawal amount based on your needs and fund performance

- Select frequency (monthly, quarterly, or custom dates)

- Fill the SWP form with your fund house or through your distributor

- Provide bank details for automatic transfers

Most online platforms like Groww, Zerodha Coin, or Paytm Money make this incredibly simple—it takes just 5 minutes.

Common Mistakes to Avoid

1. Withdrawing More Than Your Returns

If your fund gives 10% returns but you withdraw 15% annually, you’re eating into your capital. Your corpus will deplete quickly.

Rule of thumb: Keep withdrawals at or below 6-8% of your corpus annually for equity funds.

2. Starting SWP Too Early

Wait at least one year to qualify for long-term capital gains tax benefits. Otherwise, you’ll pay higher taxes.

3. Choosing the Wrong Fund

Volatile equity funds aren’t ideal for SWP if you need stable income. Consider balanced or conservative hybrid funds for regular withdrawals.

4. Not Reviewing Periodically

Market conditions change. Review your SWP strategy annually to ensure your corpus isn’t depleting faster than expected.

SWP Calculator: Planning Your Withdrawals

Before starting an SWP, always use an online SWP calculator. Input your:

- Current investment amount

- Expected return rate

- Monthly withdrawal amount

- Time period

The calculator shows if your corpus will last and grow, or if you’re withdrawing too aggressively.

Final Thoughts

Systematic Withdrawal Plan isn’t just a financial product—it’s a retirement strategy, a tax-saving tool, and a way to make your money work smarter for you. Whether you’re 30 planning for the future or 60 living in retirement, SWP offers flexibility and control that few other options can match.

Start small, test the waters, and adjust as you go. Your future self will thank you for planning this well.

Have you used SWP or are you considering it? What’s your biggest question about setting one up? Share in the comments below!

Frequently Asked Questions (FAQs)

Q: Can I stop or modify my SWP anytime?

Yes, absolutely. You can increase, decrease, pause, or stop your SWP whenever you want.

Q: Is there a minimum investment required for SWP?

Most mutual funds require a minimum investment of ₹25,000 to ₹50,000 to start an SWP.

Q: Will I get the exact same amount every month?

Yes, in fixed SWP, you’ll receive the same amount. The number of units redeemed will vary based on NAV.

Q: What happens if my fund value drops significantly?

Your withdrawals continue, but more units get redeemed. This is why choosing the right fund and withdrawal rate is crucial.

Q: Can I have multiple SWPs from the same fund?

Yes, you can set up multiple SWPs with different amounts and dates from the same mutual fund investment.