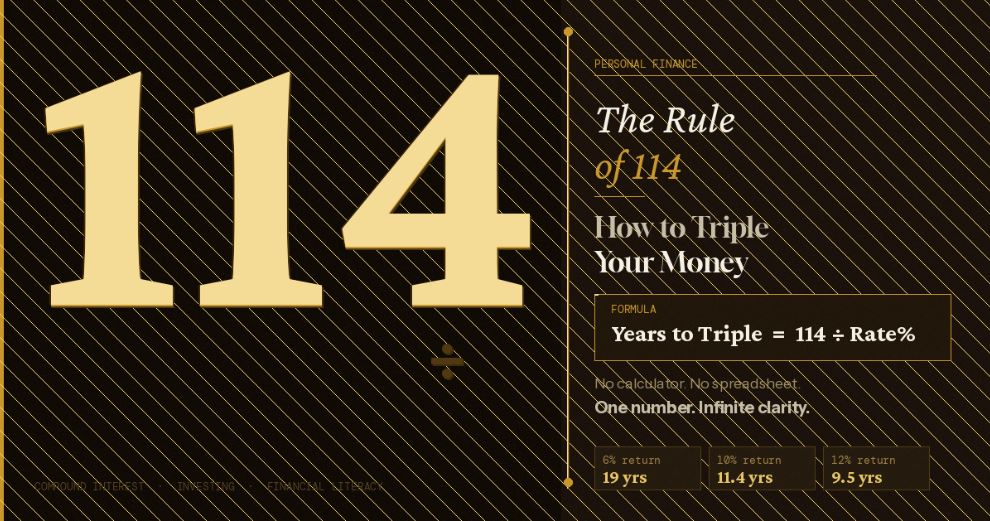

The Rule of 114: How to Triple Your Money (And Why It Matters)

If you’ve spent any time in the “FinTok” or FIRE (Financial Independence, Retire Early) communities, you’ve likely heard of the Rule of 72. It’s the classic shortcut to figure out when your money will double.

But what if doubling isn’t enough? What if you want to triple your investment?

Enter the Rule of 114.

What is the Rule of 114?

The Rule of 114 is a simplified formula used to estimate how many years it will take for an investment to triple in value, given a fixed annual rate of return.

How the Math Works

The formula is straightforward:

For example, if you have an investment earning a 6% annual return:

- 114 / 6 = 19

- It will take approximately 19 years to triple your initial investment.

Rule of 72 vs. Rule of 114 vs. Rule of 144

Serious investors use a trio of “rules” to map out their long-term wealth milestones:

| Goal | The Rule | Formula |

| Double Your Money | Rule of 72 | 72 / r |

| Triple Your Money | Rule of 114 | 114 / r |

| Quadruple Your Money | Rule of 144 | 144 / r |

Why This Matters for Your Portfolio

Understanding these rules helps you visualize the power of compounding. It shifts your mindset from “saving” to “growth.” When you realize that bumping your return from 5% to 8% can shave over 8 years off your “tripling” timeline, you start looking at expense ratios and asset allocation much more closely.

Pro Tip: These rules assume you are reinvesting all dividends and capital gains. Taxes and inflation aren’t included in the raw math, so always aim for a slightly higher “real” rate of return!

1. It Makes Abstract Numbers Concrete

Most people understand that “compound interest is good” in the abstract. But when you tell someone that their ₹5 lakh in a fixed deposit earning 6% will triple in 19 years — and that the same money in an equity index fund earning 12% will triple in under 10 years — suddenly the stakes feel very real.

2. It Reveals the True Cost of Low Returns

Keeping money in a savings account doesn’t feel like a decision. It feels like the safe default. The Rule of 114 exposes the hidden cost: at 4%, tripling takes 28+ years. At 12%, it takes under 10. Those 18 years are not an abstraction — they represent actual purchasing power, actual life goals, and actual opportunities you may be leaving on the table.

3. It Puts Inflation in Perspective

If inflation runs at 6% per year, your money’s purchasing power is being halved every 12 years (Rule of 72 in reverse). The Rule of 114 reminds you that you’re not just trying to grow your wealth — you’re in a race against inflation. To genuinely triple real wealth, your returns must meaningfully outpace inflation.

4. It Sharpens Investment Conversations

When comparing two investment options, you can now ask the right question instantly: “At this return rate, when do I triple my money?” It’s a cleaner, more visceral benchmark than comparing percentage points in a vacuum.

The Smartest Thing About Simple Rules

In a world of complex financial models, algorithmic trading, and machine-learning portfolios, there’s something quietly radical about a rule you can apply in five seconds with no tools at all.

The Rule of 114 works because it encodes a deep truth: time and rate are the only two levers that really matter in long-term investing. Everything else — stock selection, market timing, diversification strategies — operates at the margins compared to the foundational power of starting early and earning a strong return consistently.

Use it as a sanity check, motivator and a conversation starter with your family. And most importantly, use it to make the gap between your current investment behaviour and your future financial goals feel not just visible — but closeable.

Because that’s the real power of understanding compound interest: it transforms money from something that happens to you into something you actively direct toward the life you actually want.

“The best time to start was yesterday. The second best time is now. The Rule of 114 just told you how long you have to wait.”