How to Create a Perfect Financial Plan for an Indian Middle-Class Family with ₹6 LPA Income

Everyone is taking about finance but still people are confused about how the financial planning works. Lets make it more understandable for majority of Indian middle class family of 6 (Parents, Spouse & 2 Kids)

Understanding Your Financial Situation

Living on ₹6,00,000 per annum (₹50,000 per month) with a family of six requires careful planning and discipline. With dependent parents, a spouse, and two children, you’re managing a household that needs security, healthcare, education, and a path toward financial stability.

Monthly Take-Home: Approximately ₹42,000 – ₹45,000 (after basic deductions)

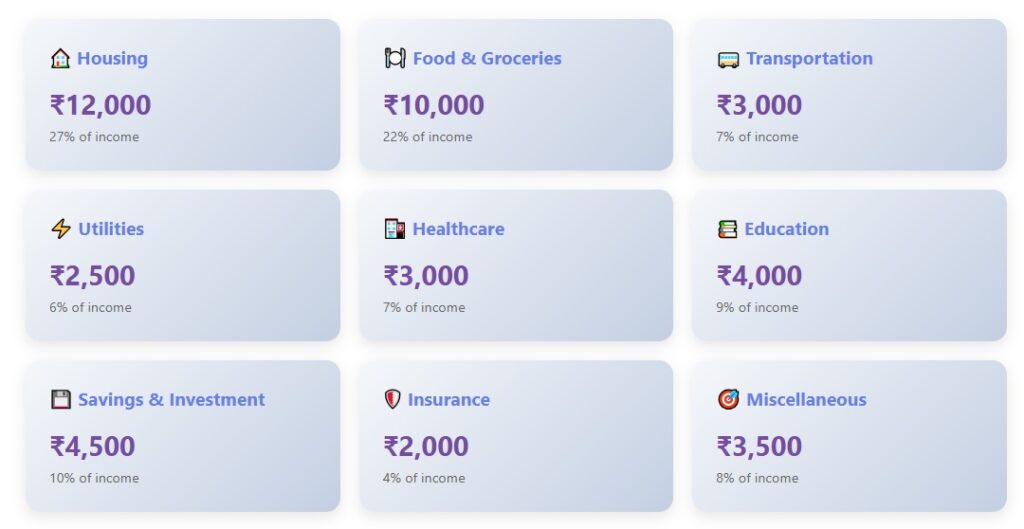

Recommended Budget Breakdown

Following the 50/30/20 rule adapted for Indian families:

Priority Financial Goals

1. Emergency Fund (First Priority)

Build an emergency fund covering 3-6 months of expenses (₹1,35,000 – ₹2,70,000). Start with a goal of ₹50,000 in the first year.

2. Insurance Coverage

- Term Life Insurance: ₹50-75 lakhs coverage (₹8,000-12,000/year)

- Health Insurance: Family floater of ₹5-10 lakhs (₹12,000-18,000/year). Consider super top-up for parents.

- Accident Insurance: ₹2,000-3,000/year for breadwinner

3. Children’s Education

Start a monthly SIP of ₹1,500-2,000 in equity mutual funds for each child. Use Sukanya Samriddhi Yojana for daughters (if applicable).

4. Retirement Planning

Contribute to EPF and start a PPF account. Invest ₹1,500 monthly in PPF for tax benefits and guaranteed returns.

5. Parents’ Healthcare

Set aside ₹500-1,000 monthly for parents’ medical expenses beyond insurance coverage.

Investment Strategy

Monthly Investment Allocation (₹4,500)

- PPF: ₹1,500 (tax benefit + safe returns)

- Equity Mutual Funds: ₹2,000 (children’s education/long-term growth)

- Recurring Deposit: ₹500 (emergency fund building)

- Gold (Digital/SGB): ₹500 (portfolio diversification)

Money-Saving Tips for Large Families

- Buy groceries in bulk from wholesale markets to save 15-20%

- Cook at home and pack lunch to save ₹3,000-5,000 monthly

- Use public transportation or carpool to reduce travel costs

- Take advantage of government schemes for children’s education and health

- Buy medicines online or from generic stores for 30-50% savings

- Use cashback and reward credit cards responsibly for regular expenses

- Negotiate rent and look for affordable housing options

- Use energy-efficient appliances to reduce electricity bills

- Teach children about money management early

- Avoid lifestyle inflation when income increases

Government Schemes to Leverage

- Ayushman Bharat: Free health insurance up to ₹5 lakhs for eligible families

- PM Kisan: If you own agricultural land

- Sukanya Samriddhi Yojana: For daughters under 10 years

- Atal Pension Yojana: Pension scheme for old age

- Pradhan Mantri Mudra Yojana: If considering a small business

Tax Planning

Maximize deductions under Section 80C (₹1.5 lakhs):

- EPF contributions

- PPF deposits

- Life insurance premiums

- Children’s tuition fees

- Tax-saving FDs or ELSS mutual funds

- Health insurance premiums under 80D (₹25,000 for self + ₹50,000 for parents)

Remember: This plan is a guideline. Adjust based on your specific circumstances, location, and family needs. Review and rebalance quarterly.

Share your thoughts in comments and subscribe nerdyfinance.org for more valuable lesson.