Fixed Deposits in India really worth now: My Honest Take After 15 Years of Investing

Let me be honest with you. When I opened my first Fixed Deposit back in 2010 with ₹50,000 that my grandmother gave me, I thought I was making the smartest financial decision ever. The bank manager told me I’d get 8.5% returns, and that sounded fantastic to my 19-year-old self.

Fast forward to today, and my relationship with FDs has become… complicated. I still have them in my portfolio, but not for the reasons you might think.

If you’re wondering whether Fixed Deposits are worth your hard-earned money now, especially with inflation eating into everything, you’re asking the right questions. Let me share what I’ve learned through my own investing journey, complete with real numbers and calculations you can actually use.

What is a Fixed Deposit? Let Me Break it Down Simply

Think of a Fixed Deposit as a promise between you and your bank. You say, “Here’s my money, keep it safe for X months/years,” and the bank says, “Sure, and I’ll pay you Y% interest for trusting us.”

Unlike your savings account where you can withdraw money anytime (and earn a measly 3-4%), with an FD, your money is locked in. The trade-off? Higher interest rates.

How FDs Actually Work: My First Experience

When I opened that first FD, here’s what happened:

My Investment Details (2009):

- Amount: ₹50,000

- Tenure: 3 years

- Interest Rate: 8.5% per annum (those were the days!)

- Interest Type: Cumulative (quarterly compounding)

I didn’t touch that money for 3 years. When it matured, I received ₹63,869. Not bad, right? That’s ₹13,869 in interest. But wait—the tax department wanted their share, which we’ll discuss later.

The Two Types of FDs: Which One Should You Choose?

1. Cumulative FD (What I Prefer)

Your interest keeps getting added back to your principal every quarter, and you receive everything at maturity.

Example: ₹1,00,000 at 7% for 5 years

- You invest: ₹1,00,000

- You get back: ₹1,41,060

2. Non-Cumulative FD (For Monthly Income Seekers)

Interest is paid out regularly—monthly, quarterly, or annually.

Example: Same ₹1,00,000 at 7% for 5 years

- You invest: ₹1,00,000

- You get: ₹7,000 every year (or ₹583 monthly)

- Total after 5 years: ₹1,35,000

Notice the difference? Cumulative FDs give you ₹6,060 more because of compounding. That’s why I prefer them unless I need regular income.

Let Me Show You How FD Interest is Actually Calculated

This confused me for years until I sat down and figured it out myself. Let me save you the headache.

Simple Interest FD Calculation (Non-Cumulative)

Formula: Interest = (Principal × Rate × Time) / 100

My Example:

- Principal: ₹2,00,000

- Rate: 7% per annum

- Time: 3 years

Interest = (2,00,000 × 7 × 3) / 100 = ₹42,000

Maturity Amount = ₹2,00,000 + ₹42,000 = ₹2,42,000

Compound Interest FD Calculation (Cumulative) – The Real Deal

Formula: A = P (1 + r/n)^(nt)

Where:

- A = Maturity Amount

- P = Principal

- r = Annual interest rate (in decimal)

- n = Compounding frequency (4 for quarterly)

- t = Time in years

Real Example from My Own FD:

- Principal (P): ₹2,00,000

- Rate (r): 7.5% = 0.075

- Compounding: Quarterly (n = 4)

- Time (t): 5 years

A = 2,00,000 (1 + 0.075/4)^(4×5) A = 2,00,000 (1 + 0.01875)^20 A = 2,00,000 (1.01875)^20 A = 2,00,000 × 1.4533 A = ₹2,90,660

Interest Earned: ₹2,90,660 – ₹2,00,000 = ₹90,660

Monthly Interest Calculation (For Monthly Payout FDs)

If you want monthly income:

Monthly Interest = (Principal × Rate) / 12

For ₹2,00,000 at 7.5%: Monthly Interest = (2,00,000 × 7.5) / 1200 = ₹1,250 per month

Current FD Rates: What Banks Are Actually Offering

Last month, I did a rate comparison for my mother’s investment. Here’s what I found:

Major Banks (General Public):

- SBI: 6.5% – 7.1%

- HDFC Bank: 6.6% – 7.4%

- ICICI Bank: 6.7% – 7.5%

- Axis Bank: 6.75% – 7.6%

Senior Citizens (Add 0.5% to above rates)

The Inflation Reality Check: My Wake-Up Call

Here’s where my love affair with FDs got complicated. In 2022, I had ₹5 lakhs sitting in FDs earning 6.5%. I felt financially secure until I checked this calculation:

My Real Returns Calculation:

- FD Rate: 6.5%

- My Tax Bracket: 30%

- After-Tax Return: 6.5% × (1 – 0.30) = 4.55%

- Inflation Rate (2022-23): 6.7%

- Real Return: 4.55% – 6.7% = -2.15%

I was literally losing money! My ₹5 lakhs would have the purchasing power of only ₹4,89,000 after one year, even though my bank statement showed more money.

Real-Life Impact: The Rice Example

Let me make this super practical. When I opened my first FD in 2009:

- ₹50,000 could buy approximately 2,500 kg of decent rice (₹20/kg)

When it matured in 2012 with ₹63,869:

- Rice cost ₹35/kg

- I could buy 1,825 kg of rice

Despite earning ₹13,869 in interest, my purchasing power had decreased by 27%. This was my “aha” moment about inflation.

Tax on FD: The Part Nobody Tells You Upfront

This is where FDs hurt the most, and I learned it the hard way.

My Tax Shock Story

In FY 2021-22, my total FD interest across all banks was ₹1,85,000. I was in the 30% tax bracket.

Tax Liability: ₹1,85,000 × 30% = ₹55,500

Plus 4% cess = ₹2,220

Total Tax: ₹57,720

So from my ₹1,85,000 interest, I actually kept only ₹1,27,280. Ouch.

TDS on FD Interest: What to Expect

Banks deduct TDS automatically if your interest exceeds:

- ₹40,000 per year (for regular citizens)

- ₹50,000 per year (for senior citizens)

My Pro Tip: I now split my FDs across 3-4 banks to keep interest below ₹40,000 per bank. This way, no TDS is deducted, and I manage my tax at year-end.

Tax-Saving FD: The One Exception

I have a 5-year tax-saver FD where I invested ₹1,50,000. Under Section 80C, I got:

- Deduction: ₹1,50,000

- Tax Saved: ₹46,800 (at 30% bracket + cess)

But here’s the catch—the interest is still taxable, and the money is locked for 5 years.

Is FD Good for Long-Term? My Honest Opinion After 15 Years

Let me share my portfolio evolution:

2010(Starting Out):

- 100% in FDs and savings account

- I felt “safe”

2025 (Today):

- 25% in FDs (emergency fund + short-term goals)

- 60% in equity mutual funds

- 10% in PPF

- 5% in gold

Why the dramatic change?

Let me show you with real numbers from my own investments:

The 10-Year Comparison: FD vs Mutual Fund

Amount Invested: ₹10,000 per month for 10 years

My FD Route (7% average):

- Total Investment: ₹12,00,000

- Maturity Value: ₹17,40,000

- Gains: ₹5,40,000

My Mutual Fund SIP (12% average):

- Total Investment: ₹12,00,000

- Current Value: ₹23,23,000

- Gains: ₹11,23,000

The difference? ₹5,83,000! That’s almost half of my total investment.

This doesn’t mean FDs are bad—it means they’re not ideal for long-term wealth creation.

When FDs Make Perfect Sense: My Current Strategy

Despite everything, I still use FDs strategically. Here’s how:

1. My Emergency Fund (₹3 Lakhs)

I keep 6 months of expenses in an FD ladder:

- ₹50,000 for 3 months

- ₹50,000 for 6 months

- ₹1,00,000 for 1 year

- ₹1,00,000 for 2 years

Every time one matures, I reinvest it for 2 years. This gives me quarterly access to some funds while maximizing returns.

2. My Daughter’s School Fees (Due in 18 Months)

I need ₹2,50,000 for her admission next year. This money is sitting in an FD earning 7.5%. I can’t risk it in the stock market for such a short duration.

3. My Parents’ FDs (They’re 65+)

My parents have ₹15 lakhs in FDs across three banks earning 8-8.5%. For them, it makes sense because:

- They get ₹1,00,000+ annual income

- They can’t afford equity market volatility

- The higher senior citizen rates are attractive

- Peace of mind is priceless at their age

4. The House Down Payment Fund

I’m planning to buy a house in 3 years. I’m systematically building a ₹20 lakh corpus in FDs. Every 6 months, I add ₹2 lakhs. This goal is too important to expose to market risk.

My FD Maximization Strategies (That Actually Work)

Strategy 1: The Bank Hopping Technique

Instead of ₹10 lakhs in one bank, I spread it:

- ₹2.5 lakhs in SBI (for UPI limit benefits)

- ₹2.5 lakhs in HDFC (for credit card linkage)

- ₹2.5 lakhs in ICICI (highest rate)

- ₹2.5 lakhs in Axis

Benefit: If one bank fails, only ₹2.5L is at risk. Plus, I avoid TDS by keeping interest below ₹40,000 per bank.

Strategy 2: The Timing Game

I track RBI policy announcements. When repo rates are hiked, I immediately book longer-tenure FDs to lock in higher rates. In 2023, when rates peaked at 8%, I opened multiple 3-year FDs. Now rates are at 7-7.5%, but I’m still enjoying 8%.

Strategy 3: Using My Parents’ PAN

Controversial, but legal: My parents are in the 5% tax bracket. When they invest in FDs:

- Their ₹5 lakh FD at 8% = ₹40,000 interest

- Tax at 5% = ₹2,000

- Net interest: ₹38,000

If I invested the same:

- Interest: ₹40,000

- Tax at 30% = ₹12,000

- Net interest: ₹28,000

I gift them the money, they invest, and eventually, the maturity amount comes back to the family with ₹10,000 saved in taxes.

Strategy 4: Form 15G Submission

My younger sister is doing her PhD and has no other income. Her FD interest is ₹35,000 annually, well below the taxable limit. I taught her to submit Form 15G at the start of every financial year to prevent TDS deduction.

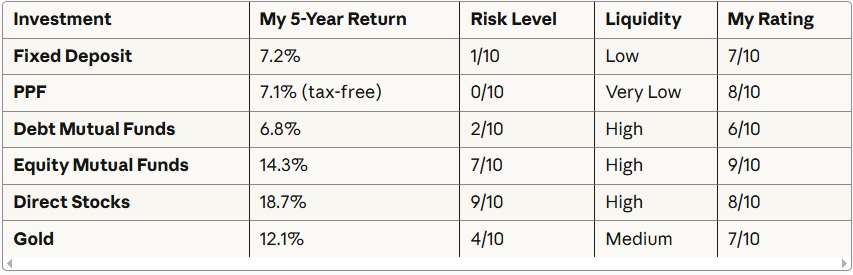

The Fixed Deposit vs Everything Else: My Personal Rankings

Based on my actual returns over the years:

My Final Verdict: The 3-Bucket Strategy

After 15 years of investing, here’s what works for me:

1: Safety (30%) – FDs + PPF

- Emergency fund

- Short-term goals (0-3 years)

- Sleep-well-at-night money

2: Growth (60%) – Equity

- Mutual fund SIPs

- Direct stocks

- Long-term wealth creation

3: Stability (10%) – Gold + Alternatives

- Inflation hedge

- Portfolio diversification

This allocation has given me 11.3% average returns over the last 7 years while letting me sleep peacefully at night.

Real Questions from My Friends (That You Probably Have Too)

Q: “Should I break my 6% FD to invest in stocks now?”

I did this in 2020 during the COVID crash with ₹2 lakhs from my FD (lost 1% interest as penalty). That ₹2 lakhs is now worth ₹4.8 lakhs. But would I do it again? Only if you:

- Have 6 months emergency fund separately

- Can hold for 5+ years

- Won’t panic during market crashes

Q: “Can I really take a loan against my FD?”

Yes! Last year, I needed ₹1.5 lakhs urgently. Instead of breaking my ₹2 lakh FD (earning 7.5%), I took a loan against it at 8.5%. I paid 1% extra but saved my compounding and avoided the penalty. Paid it back in 4 months.

Q: “Are online FDs safe?”

I’ve opened FDs through bank apps, Paytm, and even Google Pay. As long as the FD is with a scheduled commercial bank, it’s DICGC insured. I’ve had zero issues. Plus, it’s so convenient—no branch visits!

My Personal Mistakes (Learn from Them!)

Mistake 1: In 2015, I put ₹8 lakhs in a single 5-year FD at 8.5%. When rates jumped to 9% after 6 months, I was stuck. Now I ladder my FDs.

Mistake 2: I ignored the ₹40,000 TDS limit and ended up with ₹2.8 lakhs interest in one bank. They deducted ₹28,000 as TDS, and I had to wait till ITR filing to get my refund. Cash flow nightmare!

Mistake 3: I renewed an FD without checking current rates. The bank auto-renewed it at 6.2% when other banks were offering 7.5%. Always manually renew and rate-shop!

The Bottom Line: Should YOU Invest in FDs?

Here’s my honest take for different situations:

FDs are GREAT if you:

- Need money in the next 1-3 years

- Can’t afford to lose any capital

- Are above 60 years old

- Have an emergency fund to build

- Are in the 5% or nil tax bracket

FDs are NOT ideal if you:

- Want to beat inflation significantly

- Have a 5+ year investment horizon

- Are in the 20-30% tax bracket

- Want to build wealth for retirement

- Can tolerate some market volatility

For me, FDs are like the reliable friend who’ll never surprise you—positively or negatively. They have their place, but they shouldn’t be your only friend.

One Last Personal Note

That ₹50,000 FD my grandmother gave me? I still have it—well, I’ve renewed it multiple times. It’s now worth ₹1,84,000. But if I’d invested it in a Nifty 50 index fund, it would be worth ₹3,87,000 today.

Does that make me regret it? Not entirely. That FD taught me the basics of investing, discipline, and patience. Sometimes the real return on investment is the education you get along the way.

Just make sure you’re learning the right lessons for your financial goals.

What’s your FD story? Have you calculated your real returns after inflation and tax? Let me know in the comments below!