EPF vs PPF vs NPS : Which Is Better for a Salaried Indian in 2026?

Every salaried Indian juggles the same question every April: Should I invest more in my EPF, open a PPF, or go with NPS? What is best EPF vs PPF vs NPS. The trio dominates retirement planning conversations, yet most people make their choice based on half-understood rules from a colleague’s WhatsApp forward.

This guide cuts through the noise. We compare EPF vs PPF vs NPS across every dimension that matters — interest rates, tax treatment, liquidity, flexibility, and ultimate corpus size — so you can make an informed decision tailored to your life stage in 2026.

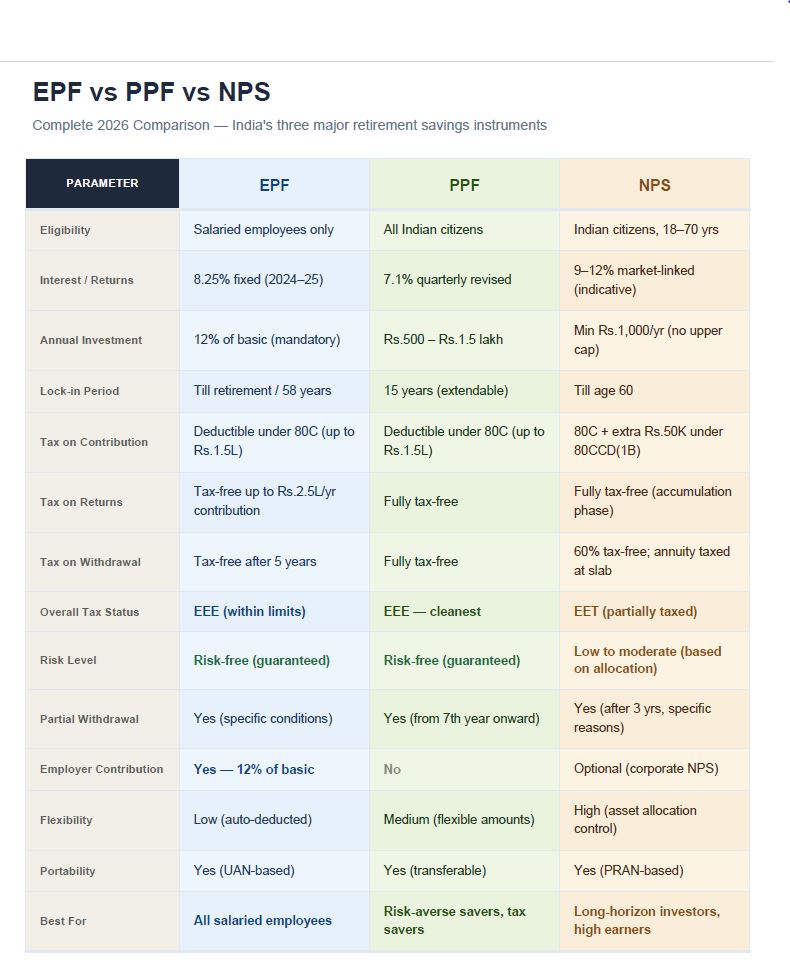

🏛️ EPF — The Retirement Bedrock

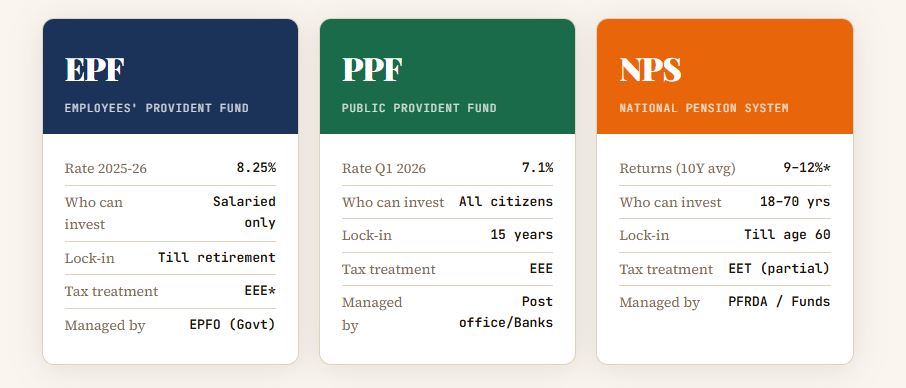

The Employees’ Provident Fund (EPF) is India’s oldest and most automatic retirement instrument. If your basic salary exceeds ₹15,000/month and your employer has 20+ employees, EPF membership is legally mandatory — you’re already enrolled whether you think about it or not.

How EPF Works in 2026

Both you and your employer each contribute 12% of your basic salary + dearness allowance. Your entire 12% goes into your EPF account. Of the employer’s 12%, only 3.67% goes to EPF; the remaining 8.33% (capped at ₹1,250/month) flows into the Employees’ Pension Scheme (EPS).

For someone with ₹50,000 basic salary, the combined monthly EPF contribution is ₹12,000 — ₹6,000 each. Over 30 years at 8.25%, that alone builds a corpus of over ₹1.8 crore.

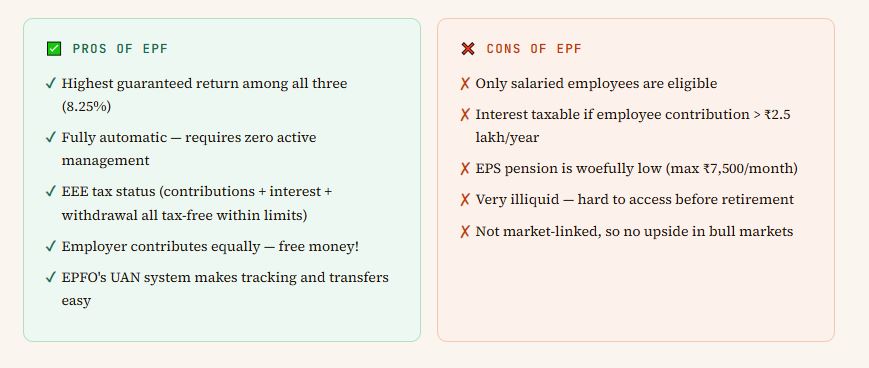

The EPFO declared an interest rate of 8.25% for 2024-25, making EPF one of the highest guaranteed returns in any government-backed scheme. The rate is reviewed annually by the Central Board of Trustees.

EPF Withdrawal Rules 2026

Full withdrawal is allowed after retirement (age 58) or after 2 months of unemployment. Partial withdrawal is permitted for emergencies: medical treatment (up to 6 months’ salary), marriage/education of children (up to 50% of employee share after 7 years), home purchase or construction (up to 90% after 5 years), and COVID-like crises (if declared).

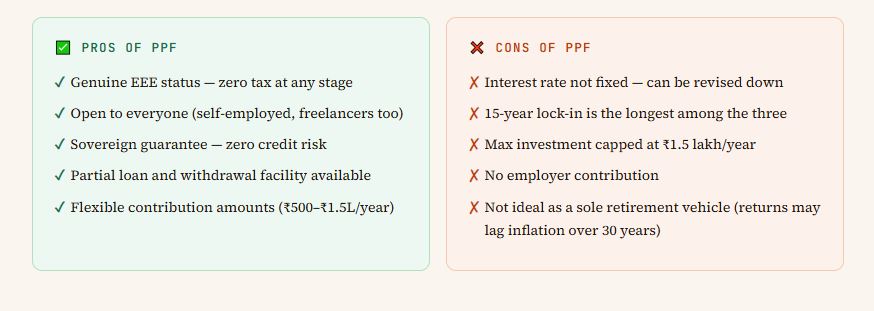

🏦 PPF — The Tax-Free Fortress

The Public Provident Fund (PPF) is open to every Indian citizen — salaried, self-employed, or even a homemaker. It is the gold standard of tax-free, risk-free investing, earning a government-declared interest rate that is revised quarterly.

PPF in 2026: Key Features

The current PPF rate stands at 7.1%, unchanged since April 2020. You can invest a minimum of ₹500 and a maximum of ₹1.5 lakh per financial year across all your PPF accounts combined. The account matures in 15 years, but you can extend it in 5-year blocks indefinitely thereafter.

Loan facility is available between the 3rd and 6th year. Partial withdrawal (up to 50% of balance at the end of the 4th year) is permitted from the 7th year onward. The account cannot be prematurely closed before 5 years — and even then, only under specific conditions like life-threatening illness.

PPF as a Debt Allocation Tool

For investors who already have EPF, PPF serves beautifully as the tax-free debt component in their overall portfolio. Unlike EPF, where the rate might change, PPF’s compounding on a 15+ year horizon is unmatched in the risk-free space.

📈 NPS — The Market-Linked Multiplier

The National Pension System (NPS) is India’s most flexible and potentially highest-returning retirement instrument. Regulated by the PFRDA, it invests your money across Equity (E), Corporate Bonds (C), Government Securities (G), and Alternative Assets (A) based on your chosen asset allocation or life-cycle fund.

NPS Returns: What to Realistically Expect

Unlike EPF and PPF, NPS returns are market-linked and not guaranteed. However, over a 10-year rolling period, NPS Tier-I Equity funds have delivered average returns of 9–12% annually. Top-performing fund managers (SBI Pension, HDFC Pension, ICICI Pru Pension) have beaten the benchmark consistently.

NPS has two tiers: Tier-I (the pension account with tax benefits and restricted withdrawal) and Tier-II (a flexible savings account with no tax benefits but full liquidity). For retirement planning, Tier-I is what matters.

NPS Exit & Annuity Rules

At 60, you can withdraw up to 60% of the Tier-I corpus tax-free. The remaining 40% must be used to purchase an annuity — a monthly pension — from PFRDA-empanelled insurers. Early exit before 60 allows only 20% as lump sum; the remaining 80% must be annuitised.

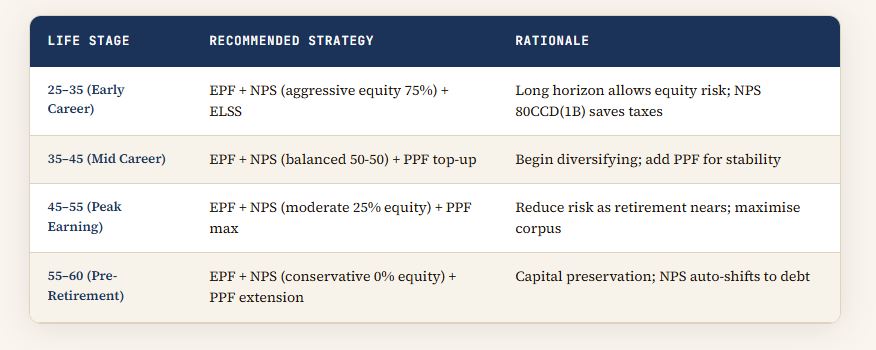

Age-by-Age Strategy

🎯 Bottom Line for 2026

The real answer isn’t EPF or PPF or NPS — it’s a strategic combination of all three, calibrated to your age and income. Think of EPF as your mandatory foundation, NPS as your tax-optimised equity engine, and PPF as your sovereign-guaranteed debt anchor.

If you must pick just one beyond EPF: choose NPS if you’re in the 30% tax bracket and have more than 15 years to retirement. Choose PPF if you’re conservative, self-employed, or less than 10 years from retirement.

❓ Frequently Asked Questions

These are the questions Indian investors search for most in 2026:

Can I have EPF, PPF, and NPS at the same time?

Yes, absolutely. There is no rule preventing you from contributing to all three simultaneously. In fact, this is the optimal strategy for most salaried Indians. EPF is mandatory; PPF and NPS are voluntary add-ons.

Which gives the highest return — EPF, PPF, or NPS?

In the long run (20+ years), NPS has the highest return potential due to equity exposure — historically 9–12% for equity-heavy portfolios. EPF at 8.25% currently beats PPF’s 7.1%, but both are guaranteed. NPS returns are not guaranteed and carry market risk.

Is NPS worth it under the New Tax Regime in 2026?

Partially. Under the New Regime, the personal 80CCD(1B) deduction of ₹50,000 is not available. However, the employer’s contribution to NPS (up to 14% for government, 10% for private) remains exempt under Section 80CCD(2) even in the New Regime. If your employer offers corporate NPS, this is worth maximising regardless of which regime you choose.

What happens to my EPF if I change jobs?

Your EPF balance can be seamlessly transferred to your new employer’s PF trust using your UAN (Universal Account Number). This is now largely automated through the EPFO portal. Do not withdraw — withdrawing before 5 years makes the entire amount taxable and surrenders years of compounding.

Can I withdraw PPF before 15 years?

Premature closure is allowed only after 5 complete financial years, and only under specific conditions: serious illness of account holder/spouse/children/parents, or higher education of account holder or minor child. Even then, a 1% interest penalty applies. Partial withdrawal (up to 50%) is allowed from the 7th year without penalty.

Is EPF interest rate guaranteed every year?

The EPF rate is declared annually by the Central Board of Trustees and approved by the Ministry of Finance. While it is not contractually guaranteed and can be revised year-to-year, the EPFO has consistently maintained it above 8% for several years. For 2024-25, it stands at 8.25%.

Which is better for tax saving: PPF or ELSS?

Both fall under 80C. ELSS (Equity Linked Saving Scheme) has a shorter 3-year lock-in and higher return potential (12–15% historically) but comes with market risk and LTCG tax of 10% on gains above ₹1 lakh. PPF is tax-free with zero market risk but a 15-year lock-in. For aggressive investors with a long horizon, ELSS often wins on post-tax returns; for conservative savers, PPF’s EEE status is unbeatable.

What is the minimum amount to invest in NPS per year?

For NPS Tier-I accounts, the minimum contribution is ₹1,000 per year. There is no upper limit on how much you can invest, though tax deduction benefits are capped at ₹1.5 lakh (80C) + ₹50,000 (80CCD1B) for own contributions, plus employer contribution up to 10% of salary.