Debt Snowball vs. Debt Avalanche — How to become debt free in 2026

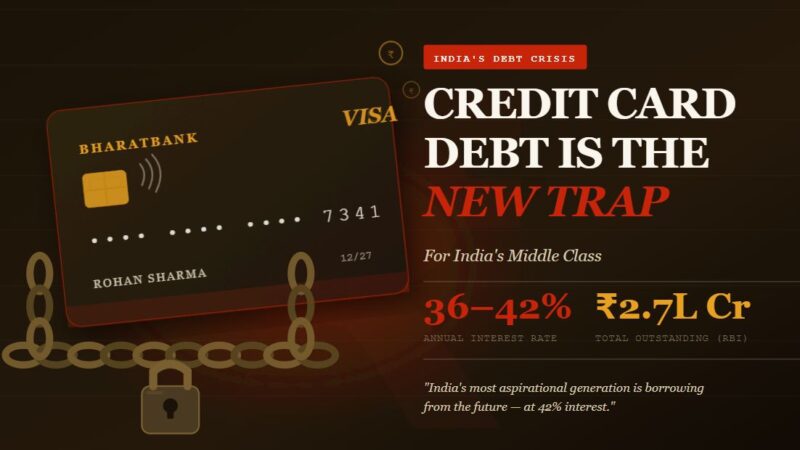

With credit card rates hitting 42% and personal loans at 24%+, India’s debt landscape is uniquely brutal. Here’s which repayment method will actually get you out faster — and save you more money.

“Indians collectively owe over ₹40 lakh crore in retail loans. If you’re reading this, you’re likely one of millions wondering: should I tackle my smallest debt first, or the most expensive one? The answer changes everything.”

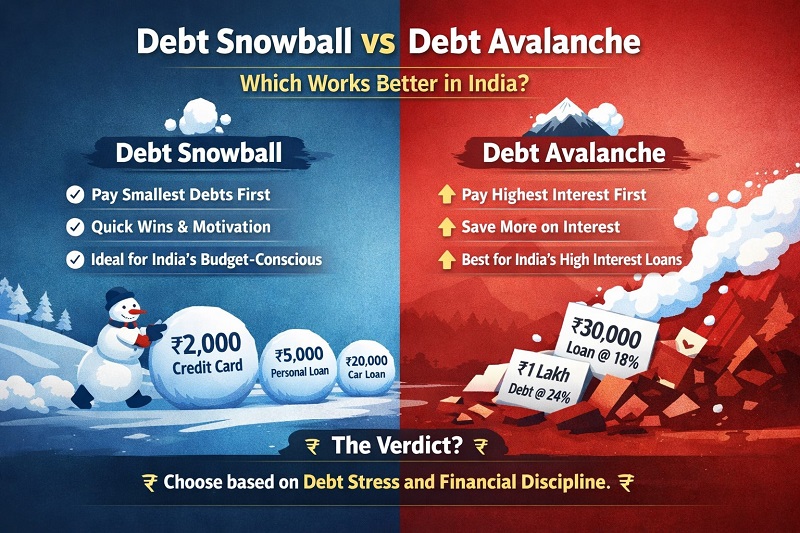

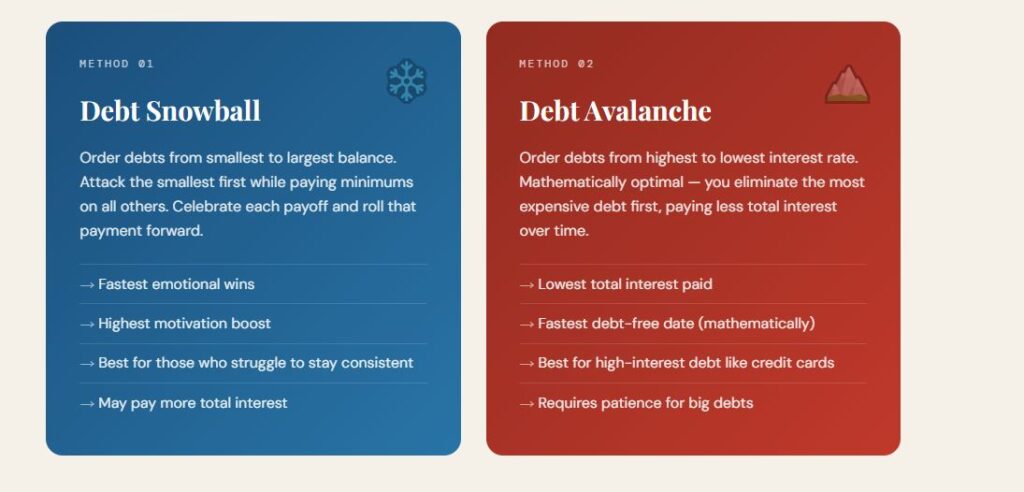

1. What is the Debt Snowball Method?

The Debt Snowball method, popularized by American personal finance expert Dave Ramsey, works on a simple psychological principle: pay off your smallest debt first, regardless of interest rate. Once it’s gone, roll that payment into the next smallest, and so on — like a snowball growing as it rolls downhill.

2. What is the Debt Avalanche Method?

The Debt Avalanche is the mathematically superior strategy. You rank all your debts by interest rate from highest to lowest, and aggressively pay off the most expensive debt first — typically your credit card.

3. Why India is Different: Interest Rates & EMI Culture

The Debt Snowball vs. Avalanche debate was largely developed in the US context, where credit card rates average 20–22%. In India, the dynamics are sharply different — and this matters enormously for which strategy you pick.

India’s Unique Debt Landscape

EMI culture is deeply embedded in India. Unlike Western countries where revolving credit dominates, Indian borrowers tend to have multiple structured EMIs — for home appliances, phones, vacations, education, and more. This creates a complex web of fixed monthly obligations that makes debt management harder to optimize manually.

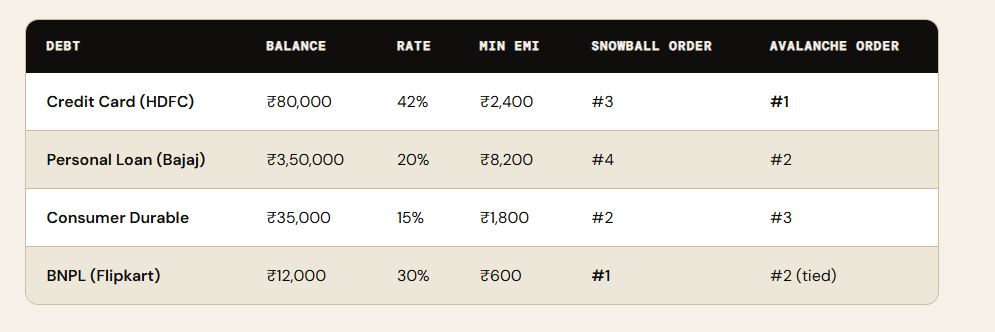

Here’s a typical Indian borrower’s debt stack:

4. Real Example: ₹8 Lakh Debt in India

Let’s look at a real-world Indian scenario. Meet Ravi, 31, a software engineer from Bengaluru with ₹8 lakhs in debt across four sources. He has ₹15,000 extra per month after minimum EMIs to accelerate repayment.

Snowball Outcome for Ravi

Ravi clears the ₹12,000 BNPL in month 1 (quick win!), then the ₹35,000 consumer durable loan by month 4. However, his 42% credit card keeps accumulating interest while he chases smaller balances. Total interest paid: approximately ₹1,87,000. Debt-free in ~38 months.

Avalanche Outcome for Ravi

Ravi hammers the 42% credit card first — it’s gone in month 5. The BNPL follows shortly. He then attacks the personal loan. His consumer durable loan sits quietly at 15% with minimum payments. Total interest paid: approximately ₹1,39,000. Debt-free in ~35 months.

💡 Key Insight

In Ravi’s case, the Avalanche saves him ₹48,000 in interest and gets him debt-free 3 months earlier. Over an Indian middle-class income, that’s almost a month’s salary recovered — just by changing the order of repayment.

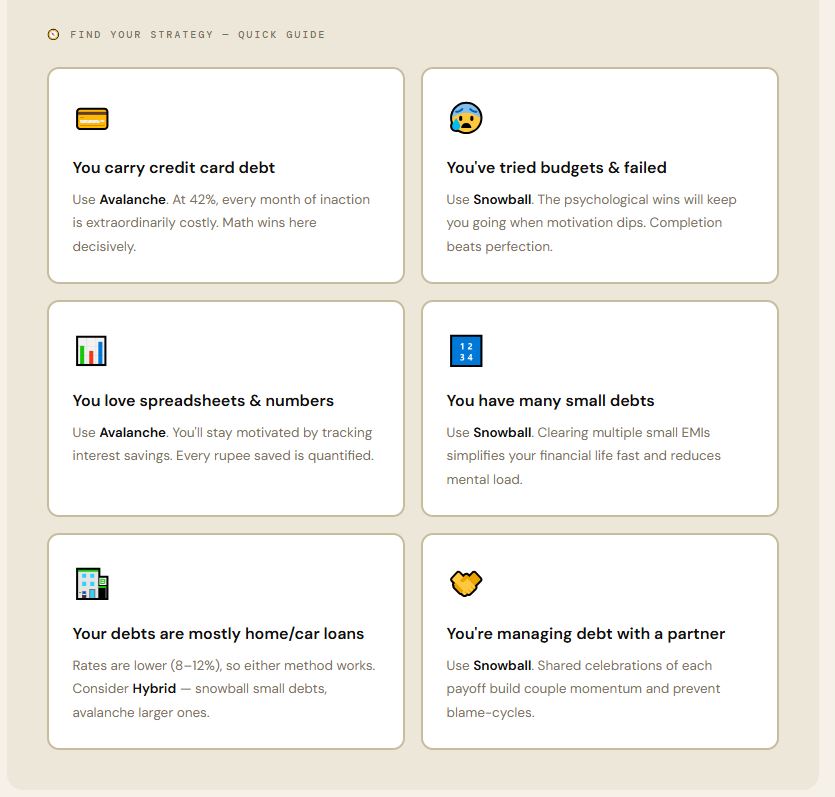

5. Which Strategy is Right for You?

There is no single correct answer — but for most Indians, the right choice depends on one critical question: Do you have credit card debt?

🏆 Our Verdict for India

For most Indian borrowers: Start with Avalanche if you have credit card or BNPL debt — the 36–42% rates make it mathematically non-negotiable. Switch to Snowball psychology for small sundry debts. Use a Hybrid approach for long-term motivation. And above all — any consistent strategy beats no strategy by years and lakhs.