Debt Mutual Funds: Your Complete Guide to Stable Returns in 2026

Remember when your parents told you to “keep some money safe”? That’s essentially what debt mutual funds are about—except they’re far more sophisticated than hiding cash under your mattress.

If you’ve been watching your savings account interest rates and thinking “there must be something better,” you’re in the right place. Let’s talk about debt mutual funds in a way that actually makes sense.

What Are Debt Mutual Funds?

Think of debt mutual funds as the steady, reliable friend in your investment circle. While equity funds are out there chasing high returns with their rollercoaster rides, debt funds are more like that friend who always pays you back on time—with interest.

In simple terms, debt mutual funds invest your money in fixed-income securities like government bonds, corporate bonds, treasury bills, and other money market instruments. These are essentially IOUs from governments and companies, promising to pay you back with interest.

Why Should You Care About Debt Mutual Funds?

Here’s the thing: not everyone can stomach the ups and downs of the stock market. And honestly? You shouldn’t have to. Debt funds offer something equally valuable—predictability and stability.

Here’s what makes them attractive:

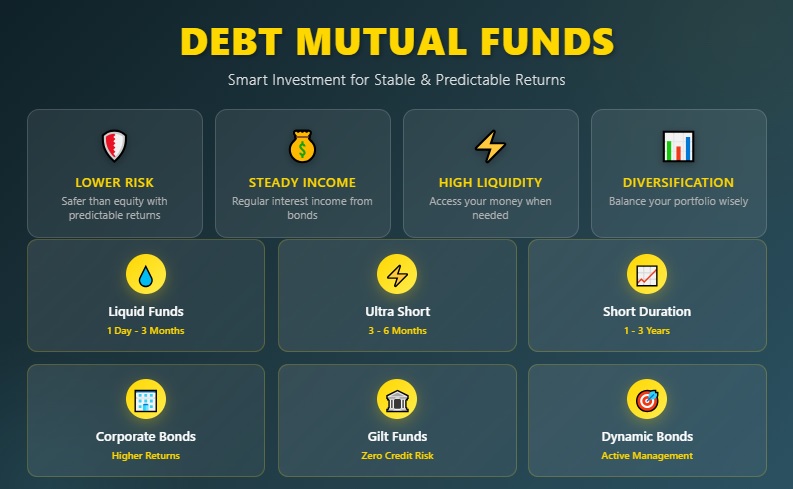

They’re generally safer than equity funds because you’re lending money rather than buying ownership. The returns are more predictable, though typically lower than equity investments. Your money stays relatively liquid—you can usually withdraw when you need to. They’re often more tax-efficient than fixed deposits, especially for longer holding periods.

Types of Debt Mutual Funds (And Which One Might Be Right For You)

Not all debt funds are created equal. Depending on what you’re trying to achieve, different types might suit you better.

Liquid Funds are perfect if you need money within days or weeks. Think of them as your emergency fund’s smarter cousin. They invest in very short-term instruments (up to 91 days) and offer better returns than your savings account without locking your money away.

Ultra Short Duration Funds are ideal when you’re parking money for 3-6 months. Maybe you’re saving for a vacation or waiting to invest in something else. These funds give you slightly better returns than liquid funds while keeping your money accessible.

Short Duration and Low Duration Funds work well for a 1-3 year horizon. Planning to buy a car? Saving for a wedding? These could be your answer.

Corporate Bond Funds invest primarily in highly-rated corporate bonds. They offer potentially higher returns but come with slightly more risk since you’re lending to companies, not the government.

Gilt Funds are for the ultra-cautious. They only invest in government securities, which means virtually zero credit risk. The returns might be modest, but you’ll sleep soundly at night.

Dynamic Bond Funds are for those who want professional management of interest rate risk. Fund managers actively adjust the portfolio based on rate movements, which can be beneficial but also adds complexity.

How Do Debt Funds Make Money?

Two main ways: interest income from the bonds they hold, and capital gains when bond prices move. Yes, bond prices change too, though usually not as dramatically as stocks.

Here’s something most people don’t realize: when interest rates fall, bond prices rise, and vice versa. So if your debt fund manager is good at predicting interest rate movements, you could see some nice gains beyond just the interest income.

The Tax Angle (Because It Matters)

This is where debt funds get interesting from a planning perspective. The tax treatment changed in April 2023, so here’s the current picture:

All gains from debt mutual funds are now taxed at your income tax slab rate, regardless of how long you hold them. This means debt funds lost some of their tax advantage over fixed deposits, but they can still be more efficient depending on your situation and the specific fund structure.

Real Talk: The Risks You Should Know About

Let me be straight with you—debt funds aren’t completely risk-free. Here’s what could go wrong:

Interest rate risk means when rates rise, your fund’s value could drop temporarily. Credit risk exists because companies can default on their bonds (though funds with high-quality portfolios minimize this). Liquidity risk applies to certain funds that might invest in less liquid securities.

But here’s the perspective you need: these risks are generally much lower than equity market risks, and good fund managers work hard to minimize them.

How to Choose the Right Debt Fund

Start with your goal and timeline. Need money within a year? Look at liquid or ultra-short duration funds. Investing for 2-3 years? Consider short duration or corporate bond funds.

Check the fund’s credit quality—funds investing in AAA and AA rated securities are safer. Look at the expense ratio because even 0.5% makes a difference over time when returns are in single digits. Review the fund manager’s track record and consistency, not just peak returns.

Common Mistakes People Make (Don’t Be That Person)

Chasing the highest returns without understanding the risk involved is a classic error. Funds offering significantly higher returns than peers are probably taking more risk.

Ignoring the exit load and redemption timelines can cost you. Some funds charge a fee if you withdraw too early.

Not matching the fund to your investment horizon creates unnecessary stress. Don’t put your emergency fund in a long-duration fund.

Should You Invest in Debt Funds Right Now?

The honest answer? It depends on the interest rate environment and your personal situation.

With inflation dynamics and RBI policies constantly evolving, debt funds remain relevant for diversification and capital preservation. They’re excellent for that portion of your portfolio that needs to be stable while still earning more than a savings account.

Getting Started Is Easier Than You Think

You don’t need lakhs to begin. Many debt funds allow investments starting from ₹500 or ₹1,000. You can invest through any mutual fund platform, directly through the fund house website, or via your bank’s investment portal.

Consider starting a SIP (Systematic Investment Plan) even in debt funds to build your safe corpus gradually.

The Bottom Line

Debt mutual funds aren’t sexy. They won’t give you stories to brag about at parties. But they’ll be there when you need them, steadily growing your money with minimal drama.

Think of them as the foundation of your financial house. Sure, equity investments might be the fancy upper floors, but you need a solid base to build on.

Whether you’re just starting out, nearing retirement, or simply want a break from market volatility, debt funds deserve a spot in your portfolio. They’re not about getting rich quick—they’re about staying on track with your financial goals without losing sleep.

Disclaimer: This article is for educational purposes only and should not be considered financial advice. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Consider consulting with a certified financial advisor for personalized recommendations based on your specific situation.