Credit Card Debt: The New Middle-Class Trap in India

In 2026, India’s middle class is facing a quiet but growing crisis. What was once marketed as a tool for “financial freedom” has, for many, become a high-interest anchor.

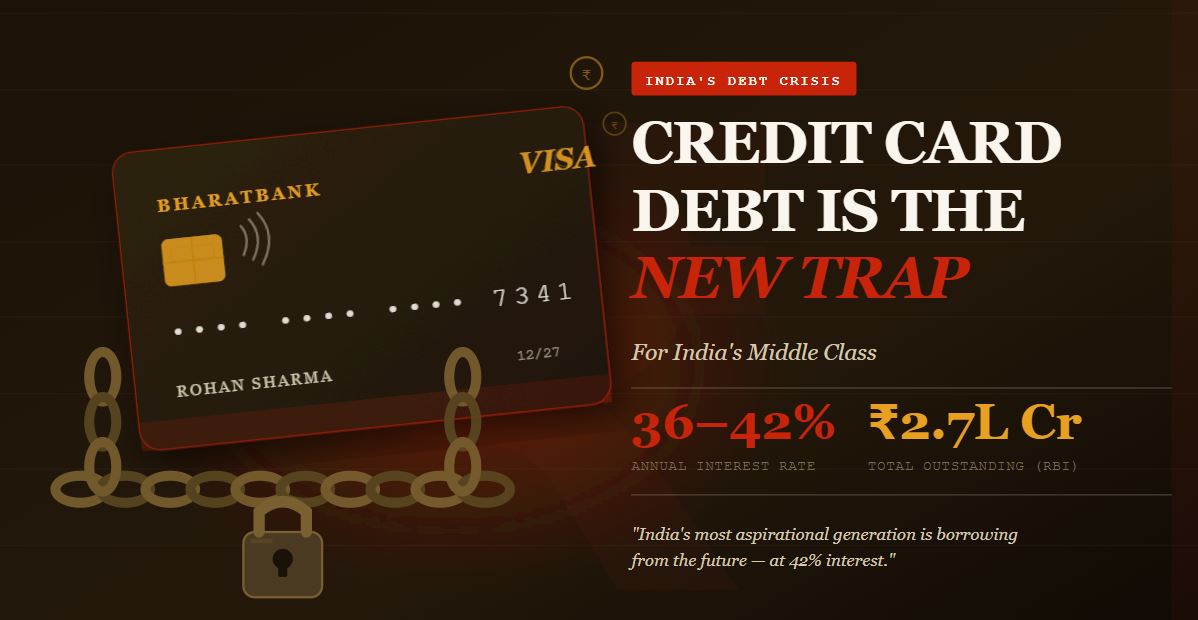

With household debt in India now crossing 41% of the GDP and credit card defaults jumping by nearly 28% in the last year, the “Credit Card Trap” is no longer just a buzzword—it’s a financial reality.

Rohan, 32, works as a marketing manager in Pune earning ₹85,000 a month. He owns a smartphone, streams on OTT platforms, orders food delivery on weekends, and takes a domestic trip twice a year. By all appearances, he lives the comfortable Indian middle-class life. But every night, he lies awake doing math — the kind that never quite works out.

His two credit cards carry a combined outstanding of ₹2.4 lakh. At an annualized interest rate of 36–42%, he’s paying nearly ₹8,000 a month just in interest. He has not touched the principal in seven months. He is not alone.

India’s middle class is in a debt trap. And the instrument of that trap is the credit card — once a symbol of arrival, now a mechanism of quiet financial ruin.

How Did We Get Here?

Ten years ago, a credit card was a privilege — something you got after submitting three years of IT returns and a letter from your employer. Today, card issuers send pre-approved offers over WhatsApp. Banks like HDFC, SBI, Axis, and ICICI have aggressively expanded their card portfolios, chasing the enormous, aspirationally-driven Indian middle market.

Meanwhile, the infrastructure for spending exploded. UPI enabled credit on tap. BNPL (Buy Now, Pay Later) schemes blurred the psychological barrier between spending and debt. EMI options appeared on everything from air conditioners to gym memberships. And targeted digital advertising perfected the art of making want feel like need.

The result: millions of salaried Indians now carry revolving credit card balances they cannot pay off — funding a lifestyle they can’t quite afford on salaries that haven’t kept pace with inflation.

The 7 Hidden Traps Built Into Every Credit Card

Credit card companies are not charities. Every feature is a carefully engineered psychological mechanism. Here’s what the fine print never explains clearly:

1. The Minimum Payment Illusion-Paying only the minimum due (usually 5% of outstanding) feels responsible. It isn’t. The remaining 95% attracts interest at 3–3.5% per month — that’s over 42% annually. A ₹1 lakh balance at minimum payment takes over 8 years to clear and costs you nearly ₹1.8 lakh in interest.

2. Interest-Free Period Myth-The 45–50 day interest-free period disappears the moment you carry a balance. Once you don’t pay in full, every new purchase starts accruing interest from Day 1 — no grace period. Most cardholders don’t know this.

3. Cash Advance Traps-Withdrawing cash from an ATM using your credit card incurs a 2.5–3% transaction fee plus interest from the very moment of withdrawal — no grace period at all. It is one of the most expensive forms of borrowing.

4. Reward Points as Bait-Spend ₹100, earn 1–2 points. Redeem 1,000 points for ₹7–10 in value. The math only works if you never carry a balance. For revolvers (those who don’t pay in full), rewards are irrelevant — interest charges dwarf any cashback earned.

5. EMI Conversion — The Hidden Anchor– Converting a large purchase into EMIs feels manageable. But most banks charge 12–18% per annum on card EMIs — far above SBI or home loan rates. And your credit limit remains blocked, creating a double bind.

6. Limit Increases You Didn’t Ask For- Banks regularly increase credit limits without your request. This isn’t generosity — it’s a nudge to spend more. Higher limits, psychological research shows, lead to higher spending regardless of income.

7. Lifestyle Inflation Lock-In– Once swiped into a higher-spend lifestyle, scaling back feels like deprivation. The card makes tomorrow’s problem seem abstract; today’s purchase feels real. This is the most dangerous trap — it’s not financial, it’s psychological.

The Warning Signs of a Debt Trap

Are you in control, or is the card controlling you? Watch out for these red flags:

- The Revolving Door: You only pay the minimum due every month.

- Credit Utilization: Your balance is consistently above 30% of your total limit.

- The ATM Trap: You’ve started withdrawing cash from your credit card (one of the most expensive ways to borrow).

- Loan Stacking: You’re taking “Top-up” personal loans just to clear your credit card bills.

How to Escape the Credit Card Debt Trap: A 6-Step Plan

- Calculate Your True Debt Position-List every card, its outstanding balance, minimum payment, and interest rate. Most people are shocked when they see the total clearly for the first time. Clarity is the first act of liberation.

- Stop All New Swipes Immediately-Freeze the cards — literally, put them in a zip-lock bag with water in your freezer. Use UPI or debit for all spending while you clear the debt. The card must not grow while you fight it.

- Use the Avalanche Method-Pay the minimum on all cards. Direct every extra rupee at the highest-interest card first. Once cleared, roll that payment to the next card. This minimizes total interest paid mathematically.

- Refinance with a Lower-Rate Option-Take a personal loan at 14–16% from your bank and clear all card outstanding. You convert 42% debt into 16% debt — your EMI may feel similar but the payoff timeline collapses dramatically.

- Negotiate with Your BankBanks – would rather restructure than write off. If you’re genuinely stressed, call the bank, explain your situation, and ask for a one-time settlement or EMI conversion at a lower rate. Many people don’t realize this is an option.

- Build a 3-Month Emergency Fund-Most people land in credit card debt due to an emergency with no backup. Before investing, build a buffer — even ₹50,000 in a liquid fund — so the next emergency doesn’t restart the cycle.

The Bottom Line

Credit cards aren’t inherently “evil,” but in an economy where credit is easier to get than a steady raise, they require extreme discipline. The goal is to use credit as a convenience tool, not a life support system.

One thought on “Credit Card Debt: The New Middle-Class Trap in India”