Compounding -The 8th Wonder of the World

“Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.” While this quote is often attributed to Albert Einstein, its wisdom is particularly relevant for Indian investors navigating a rapidly growing economy. This powerful statement captures a fundamental truth about wealth building that separates financial success from struggle.

In this comprehensive guide tailored for Indian investors, you’ll discover how compound interest works, why it’s so powerful, and most importantly, how you can harness it to build lasting wealth through Indian investment instruments rather than fall victim to it through loans and credit cards.

What Is Compound Interest?

Compound interest is the process where your money earns returns, and then those returns generate their own returns. Unlike simple interest, which only calculates returns on your initial investment, compound interest creates a snowball effect that accelerates wealth growth over time.

Simple vs. Compound Interest: A Clear Example

Imagine you invest ₹1,00,000 at a 10% annual return:

With Simple Interest:

- Year 1: ₹1,00,000 + ₹10,000 = ₹1,10,000

- Year 2: ₹1,00,000 + ₹10,000 = ₹1,20,000

- Year 10: ₹1,00,000 + (₹10,000 × 10) = ₹2,00,000

With Compound Interest:

- Year 1: ₹1,00,000 + ₹10,000 = ₹1,10,000

- Year 2: ₹1,10,000 + ₹11,000 = ₹1,21,000

- Year 10: ₹2,59,374

After just 10 years, compound interest gives you nearly ₹60,000 more. After 30 years, the difference becomes staggering: ₹4,00,000 with simple interest versus ₹17,44,940 with compound interest.

The Mathematics Behind the Magic

The compound interest formula is:

A = P(1 + r/n)^(nt)

Where:

- A = Final amount (maturity value)

- P = Principal (initial investment)

- r = Annual interest rate (as a decimal)

- n = Number of times interest compounds per year

- t = Time in years

But you don’t need to be a mathematician to benefit from compound interest. You simply need to understand its three key drivers and know which Indian investment options offer the best compounding opportunities.

The Three Pillars of Compound Interest Success

1. Time: Your Most Valuable Asset

Time is the most powerful factor in compound interest. The longer your money compounds, the more dramatic the results.

Consider two investors:

Priya starts at age 25:

- Invests ₹5,000/month through SIP for 10 years (₹6,00,000 total)

- Stops investing at age 35

- Lets it grow until age 60

- Result at 12% annual return: ₹1,35,21,531

Rahul starts at age 35:

- Invests ₹5,000/month through SIP for 25 years (₹15,00,000 total)

- Continues until age 60

- Result at 12% annual return: ₹1,13,24,537

Priya invested ₹9,00,000 less but ended up with ₹21,96,994 more simply because she started 10 years earlier. This is the extraordinary power of time in compound interest.

2. Rate of Return: Every Percentage Point Matters

Small differences in return rates create massive differences in outcomes over time.

On a ₹1,00,000 investment over 25 years:

- 6% return (FD rate) = ₹4,29,187

- 10% return (balanced fund) = ₹10,83,471

- 12% return (equity fund) = ₹17,00,006

A 6% difference in return rate creates a ₹12,70,819 difference in final wealth. This is why choosing the right investment vehicles matters enormously for Indian investors.

3. Consistency: The Discipline That Builds Empires

Regular contributions through SIP amplify compound interest dramatically. Adding just ₹3,000 monthly to a ₹1,00,000 initial investment at 12% annual return gives you ₹43,89,119 after 25 years, compared to ₹17,00,006 without monthly contributions.

How to Earn Compound Interest: Investment Options for Indians

Best Indian Investment Instruments That Harness Compound Interest

1. Equity Mutual Funds (Direct Plans) Equity mutual funds have historically given 12-15% returns over long periods. Direct plans save you 1-1.5% in expense ratios, dramatically improving compound returns.

Popular Options:

- Large-cap funds (Nifty 50 index funds)

- Mid-cap and small-cap funds (higher risk, higher returns)

- Flexi-cap funds (diversified approach)

2. Public Provident Fund (PPF) Government-backed with current returns around 7.1% per annum, compounded annually. Benefits include tax deduction under Section 80C and tax-free returns under EEE status. 15-year lock-in makes it ideal for retirement planning.

3. Employee Provident Fund (EPF) Currently offers around 8.25% interest, compounded annually. Employer contributions double your investment, and it’s EEE (Exempt-Exempt-Exempt) for tax purposes.

4. Sukanya Samriddhi Yojana (SSY) For girl child education, offering 8.2% interest currently. Small investments of ₹250-₹1,50,000 annually grow tax-free for 21 years.

5. National Pension System (NPS) Market-linked returns (typically 9-12% historically) with tax benefits under Section 80CCD(1B). Choice between equity, corporate bonds, and government securities.

6. Systematic Investment Plans (SIP) in Mutual Funds The rupee cost averaging benefit combined with compound interest makes SIPs the most powerful wealth creation tool for salaried Indians.

7. Fixed Deposits with Auto-Renewal Banks and Post Office FDs offer 6-7.5% returns. Cumulative FDs (where interest is reinvested) provide compound interest, though returns are taxable.

8. Recurring Deposits (RD) Small monthly investments (₹500-₹10,000) in RDs compound quarterly in most banks. Suitable for short-term goals (1-10 years).

9. ELSS (Equity Linked Savings Scheme) Tax-saving mutual funds with 3-year lock-in offering potential 12-15% returns with Section 80C benefits up to ₹1.5 lakh.

10. Real Estate and REITs Property appreciation and rental income create compound returns. REITs (Real Estate Investment Trusts) allow real estate investment starting from ₹10,000-₹15,000.

The Crorepati Formula: Putting It All Together for Indian Investors

Becoming a crorepati through compound interest isn’t mysterious. It’s mathematical.

Path 1: The Early Starter (Middle-Class Saver)

- Start at age 25

- Invest ₹5,000/month in equity mutual funds

- Earn 12% average annual return

- Result at age 55: ₹1,76,49,569 (₹1.76 crore)

Path 2: The Consistent Investor

- Start at age 30

- Invest ₹8,000/month in diversified portfolio

- Earn 12% average annual return

- Result at age 60: ₹2,67,30,359 (₹2.67 crore)

Path 3: The Aggressive Wealth Builder

- Start at age 25

- Invest ₹10,000/month increasing by 10% annually

- Earn 12% average annual return

- Result at age 55: ₹6,35,12,447 (₹6.35 crore)

Path 4: The Government Employee

- Start at age 25

- EPF contribution: ₹3,000/month (you + employer)

- PPF contribution: ₹5,000/month

- Average return: 8% on EPF, 7.5% on PPF

- Result at age 60: ₹2,24,67,893 (₹2.24 crore)

Notice that earlier starting ages require less monthly investment to achieve better results. This is compound interest at work.

Common Compound Interest Mistakes Indians Make

Mistake 1: Keeping Too Much in Savings Accounts

Savings accounts offer 2.75-3.5% interest, below inflation (4-6%). Your money loses real value. Move surplus beyond 6 months’ emergency fund to PPF, mutual funds, or FDs.

Mistake 2: Choosing Regular Plans Over Direct Plans

Regular mutual fund plans charge 1-1.5% more in expense ratio. On a ₹10 lakh investment over 20 years, this costs ₹8-10 lakh in lost compound returns. Always choose direct plans.

Mistake 3: Breaking Fixed Deposits and PPF Prematurely

Premature withdrawal attracts penalties and interrupts compounding. A ₹1 lakh PPF withdrawal at year 7 costs you ₹1,87,893 in lost growth by year 15.

Mistake 4: Not Increasing SIP with Income

Many Indians start ₹1,000 SIP and never increase it despite salary hikes. Increasing SIP by 10% annually dramatically multiplies final corpus.

Mistake 5: Investing in Insurance as Investment

ULIPs and endowment plans offer poor returns (4-6%) with high charges. Separate insurance (term plan) from investment (mutual funds/PPF) to maximize compound returns. Always keep a health insurance to avoid any future medical crisis.

Mistake 6: Ignoring Tax-Advantaged Instruments

Not utilizing Section 80C (₹1.5 lakh), 80CCD(1B) (₹50,000), and other deductions means paying unnecessary tax instead of letting that money compound.

Mistake 7: Gold and Cash Hoarding

Physical gold doesn’t compound (only appreciates). Sovereign Gold Bonds offer 2.5% interest plus price appreciation. Cash under mattress loses value to inflation daily.

Maximizing Your Compound Interest Strategy: Indian Context

Start with Small SIPs, Increase Gradually

Begin with ₹500-₹1,000 monthly SIP to develop the habit. Increase by ₹500-₹1,000 every 6 months or with each salary increment.

Maximize Tax-Saving Investments First

Fully utilize Section 80C (₹1.5 lakh) through ELSS, PPF, EPF, and NPS. The tax saving itself adds to your compound returns. Section 80CCD(1B) offers additional ₹50,000 deduction for NPS.

Use Step-Up SIPs

Most mutual fund platforms offer automatic SIP increase by 5-20% annually. This aligns your investments with income growth and accelerates wealth building.

Diversify Across Asset Classes

Don’t put everything in one instrument. Suggested allocation for young Indians:

- 60% equity mutual funds (growth)

- 20% PPF/EPF (safety + tax benefits)

- 10% gold (hedge)

- 10% liquid fund (emergency)

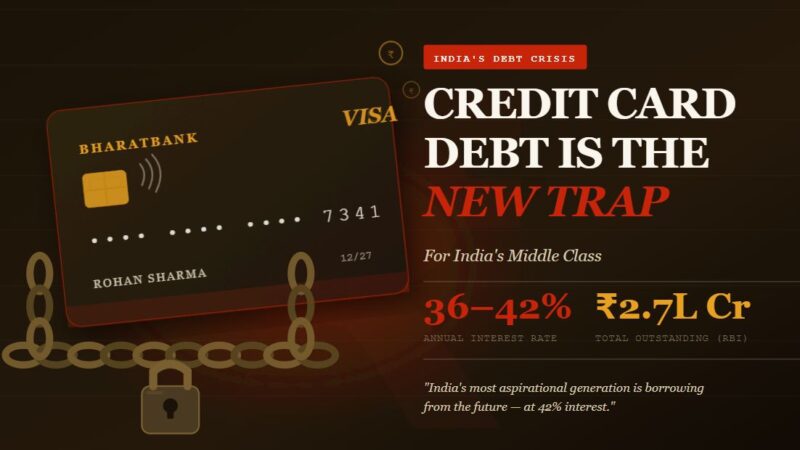

Eliminate High-Interest Debt Immediately

Pay off credit cards (36-42% interest) before investing in markets (12-15% returns). The net benefit is enormous. Use personal loans only for genuine emergencies.

Start Retirement Planning Early

With life expectancy at 70+ years and limited social security, compound interest through National Pension Scheme (NPS), PPF, and EPF is crucial. Starting at 25 versus 35 can mean ₹50 lakh-₹1 crore difference.

Teach Children About Compound Interest

Open Sukanya Samriddhi for daughters. Start mutual fund SIPs in children’s names. Financial literacy combined with early investing creates generational wealth.

Tax Implications on Compound Interest in India

Understanding taxation helps maximize post-tax compound returns:

Tax-Free Instruments:

- PPF: Completely tax-free (EEE)

- EPF: Tax-free if withdrawn after 5 years

- SSY: Completely tax-free

- NPS: Partially exempt

Taxable Instruments:

- FD interest: Added to income, taxed at slab rate (up to 30%)

- Debt mutual funds: LTCG taxed at slab rate

- Equity mutual funds: LTCG above ₹1.25 lakh taxed at 12.5%, STCG at 20%

Strategy: Prioritize tax-free instruments first, then use tax-efficient equity funds over FDs.

Compound Interest During Indian Economic Cycles

India’s GDP growth (6-8% annually) creates unique compounding opportunities:

Infrastructure Boom: Thematic funds in infrastructure sectors benefit from government spending.

Digital India: IT and fintech sector funds have compounded at 15-20% over past decades.

Consumption Growth: FMCG and consumer funds benefit from rising middle class.

Manufacturing Push: Make in India initiatives boost manufacturing sector returns.

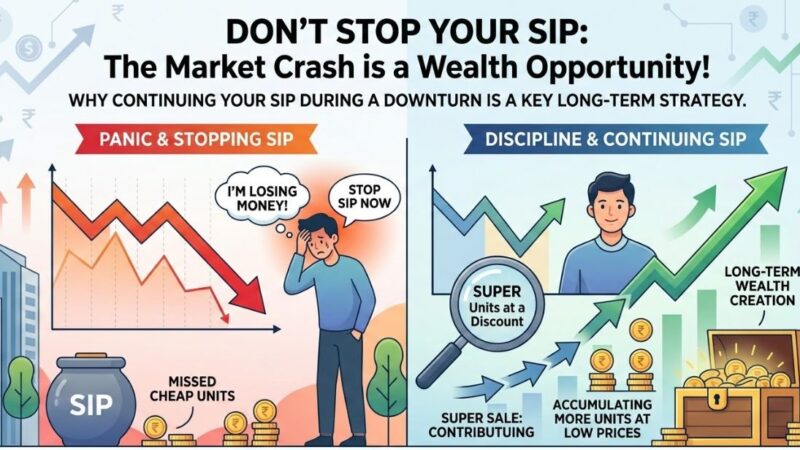

Stay invested through economic cycles. Indian markets have historically recovered from every crash and reached new highs.

Conclusion: Your Eighth Wonder Awaits

Einstein allegedly called compound interest the eighth wonder of the world because it’s a force that can work miracles in your financial life, but only if you understand and harness it. Those who don’t understand it will spend their lives paying interest to banks and credit card companies, watching their wealth slip away month after month.

For Indian investors, compound interest is even more powerful. With a young population, growing economy, and improving financial infrastructure, the next 20-30 years offer unprecedented wealth creation opportunities through systematic investing.

The choice is yours. Will you be the one who earns compound interest or the one who pays it?

The mathematics is simple. The strategy is straightforward. Investment options are available to everyone from ₹500 monthly. All that remains is your decision to start today.

Remember: the best time to start was yesterday. The second-best time is now. Your future self will thank you for every day you choose to harness the eighth wonder of the world.

As we say in India, “Boond boond se sagar banta hai” (Drop by drop, an ocean is formed). Start your SIP today, let compound interest work its magic, and watch your drops become an ocean of wealth.